Sometimes I have absolutely nothing to write about on TRB. I still find a way, but there are times when my queue is simply empty.

Then other times, I have so much to say that my queue contains topics that need to be explored for fear of them growing stale!

In fact, most two-part blog stories start with the intention being one, but after you hit a certain length, that alarm bell goes off that says, “Hey, this feels like a ‘Part II’ is going to be needed.”

Then there are the times where we explore an important topic and merely touch on a secondary or related topic therein, but where that second topic necessitates a blog post of its own.

Last Thursday’s blog was exactly that.

On Thursday, we looked at the “Mortgage Renewal Cliff” and traced back the origin of the term, exactly why it came to exist, and got up to speed on whether or not it’s still relevant in March of 2025.

But at the very end of the post, I mentioned mortgage delinquencies.

This was an afterthought as far as the blog was concerned, but when I ran into a client on the weekend, she said, “I read your blog on Thursday; you’ve never talked about mortgage delinquencies before, it was cool. But what is a delinquency?”

Good question.

Up until now, we’ve merely assumed that everybody knows!

My client continued to ask, “Is a delinquency the same thing as a default? And what’s it called when the bank actually takes your house and sells it?”

All good questions, but then came the kicker:

“At what point does a delinquincy rate signal a problem?”

I touched on this during Thursday’s blog, but I think that every reader, economist, lender, and banker are going to have their own answer to this question.

This is also where my favourite saying comes into play: you can make numbers say anything you want.

We’ve played this game many times before on TRB, but let me ask a hypothetical question:

If you heard that a local baseball team increased their attendance by 1000%, how would you describe that figure?

Would you describe this as “a lot”?

Relatively, yes. But relative to what?

Alright, here’s what I’m really asking: if you heard that a local baseball team increased their attendance by 1000%, would you simply assume this means many people attend the games?

Because if the team was averaging one fan per game, and another ten joined on average thereafter, then there’s your 1000% increase.

In the end, eleven fans isn’t a lot.

I talk quite a bit about relative versus absolute when I analyze statistics here on TRB, and when it comes to mortgage delinquencies, I’ve felt this really hits home.

First, a couple of definitions.

A “delinquent” mortgage is one where the borrowers are more than three months, or ninety days, overdue for payment. This is referred to as “a mortgage delinquency” as well as “mortgage in arrears.”

You’ll hear these terms used interchangeably but “delinquent” is the same as “in arrears.”

Now what is a mortgage “in default?”

That’s trickier, especially because the media will often use the terms interchangeably.

Here’s an example:

The headline says “defaults” but the article uses the word “delinquent.”

Again, you can ask ten people in the mortgage industry to differentiate between the terms, and you’ll get ten slightly different answers.

Simply put, “delinquent” means overdue. To be in “default” means to break the loan covenant, but we all know that missing a payment is exactly that. So to be “delinquent” essentially means to be in “default,” but it’s widely understood that to be in default means to continuously miss payments to the point where the lender is, or has taken action to recover the money owed, including foreclosure.

The verbiage will differ depending on the geography, and just as Americans will refer to a deposit “in escrow” and we say the funds are “in trust,” we see these terms and their definitions vary consistently.

In Canada, we use the term “mortgage delinquincy” and we define this as a mortgage where payments are overdue by 90 days.

Defaults, foreclosures, power of sales, bank sales – this is a whole other conversation. Not every delinquent borrower has their house foreclosed on by the lender and sold against their will.

Now, back to this idea that “you can make numbers say anything you want.”

Let’s look at some of the recent headlines about mortgage delinquincies.

Here’s a banger:

“Ontario’s Mortgage Delinquincy Rate Nearly Doubled In The Final Months Of 2024”

CTV News

February 25th, 2025

Hard to ignore the word “double,” right?

And there’s no fudging the numbers here. This is a 90.2% increase from Q4 of 2023 to Q4 of 2024.

But we’ll come back to this.

Three days later, we see this article in our news feeds:

But when we click on the link, it takes us to this article:

“Ontario Mortgage Delinquincy Rate Jumps 50% Amid Growing Signs Of High-Rate Renewal Shock”

Toronto Star

February 28th, 2025

The first link said, “since 2019.”

But maybe that’s not sexy enough?

The second headline simply says “jumps 50%” and then adds “shock.”

Newspapers re-write headlines all the time, just as they update articles that have already been released. This felt like a case of trying to make the situation sound a lot more dire!

Not only that, the sub-headline reads:

“Credit agency Equifax reports more than 11,000 mortgages in the province missing at least a payment in the fourth quarter of 2024, nearly three times the number seen in 2022.”

So now we’re talking about missing one payment instead of being delinquent, which is missing three payments, and we’re also “three times,” or 300%, over 2022.

Got it.

So through two articles with three headlines, we’re looking at mortgage delinquencies:

-in Ontario

-in Canada

-year-over-year

-since 2019

-since 2022

-in Q4

-one month in arrears

-three months in arrears

Did I miss anything?

There are so many ways to make an argument when you’re armed with data.

…

Right, because this is in Ontario, but the first headline referred to delinquincy rates in Canada.

And then sometimes, we’re not given any statistic or takeaway in the headline. We’re just given this:

“Lower Interest Rates, Higher Defaults: What’s Going On?”

CBC News

March 5th, 2025

They’re not wrong.

Interest rates are dropping and mortgage delinquencies are increasing.

But mortgage delinquencies have always been viewed as a “lagging indicator” since the problem began at least three months ago.

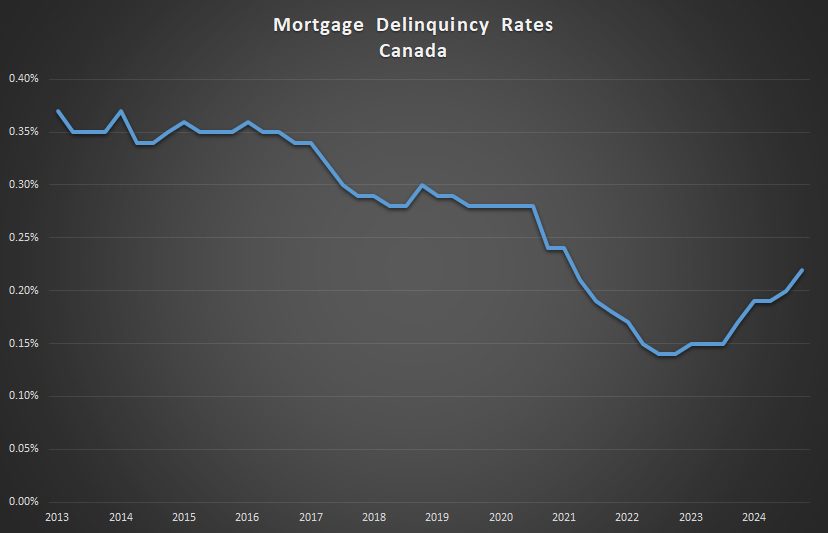

On Thursday, I provided you with the following chart for discussion purposes:

If you’re interested in the data, the CMHC publishes it HERE.

As we noted last week, the delinquency rate in Canada hit a low of 0.14% in Q3 and Q4 of 2023.

To see the same rate increase to 0.22% by Q4 of 2024 is to say that it “increased by 57.1%.”

That’s a big increase!

And while the newspapers are choosing their own statistics, whether Canada-wide, Ontario-wide, or comparing a particular quarter, month, or year to any one period in the past, I’m simply looking at the obvious data in front of me.

The mortgage delinquency rate was at a low of 0.14% in 2023.

The fact that it’s risen to 0.22% as of Q4 last year doesn’t move the needle for me at all.

What would move the needle?

Well, if that figure increases to 0.35% or thereabouts, I would conclude that the increase is troubling.

However, with the delinquency rate sitting consistently around 0.35% from 2013 through 2016, I also wonder whether this actually would be anything to write home about.

After all, do you remember the alarm bells going off in 2013, 2014, 2015, and/or 2016 when delinquency rates were at 0.35%?

No.

Of course not.

Nothing was made of this at the time since a delinquency rate of 0.35% is still ridiculously low.

As I noted at the onset, there’s “relative” and there’s “absolute” when you look at data, but if you change what that data is relative to, you can change your entire perspective.

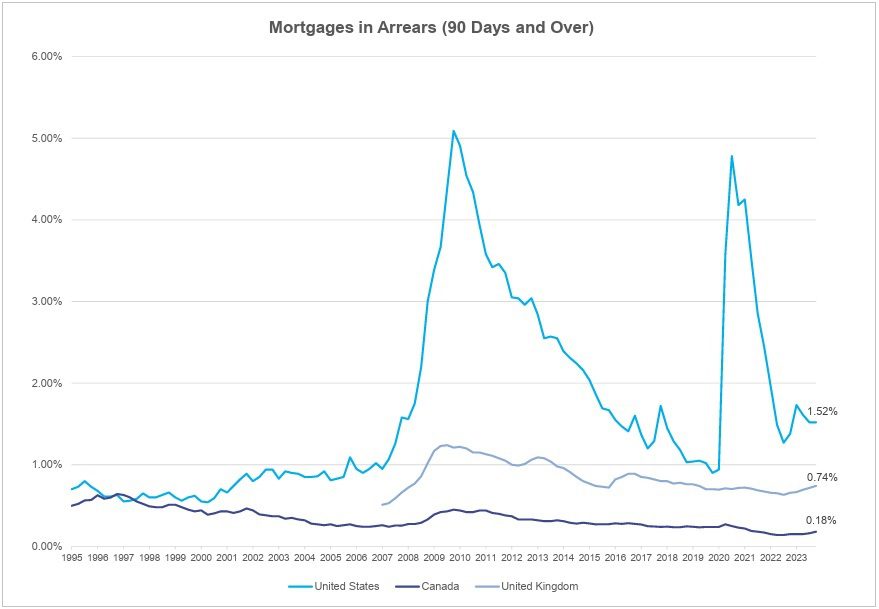

Case in point: how does Canada’s delinquency rate look relative to the United Stats or the UK?

Here’s a great read, and very current!

“Read The Latest Statistics On Mortgages In Arrears In Canada”

Canadian Bankers Association

March 28th, 2025

If a picture paints a thousand words for you, then try this one on for size:

“Gather round, youngsters. Let me tell you about 2008…”

I think we all know that Canada escaped the financial crisis seventeen years ago essentially unharmed, but just look at the amount of mortgage delinquencies during the pandemic in the United Stats versus Canada.

Is there any conclusion to draw here other than the fact that Canada has among the lowest mortgage delinquency rates in the world?

The data I have for mortgage delinquencies only goes back to 2013 as that’s all that the CMHC makes publicly available (and I suppose easily accessible, so please email me if you have another source!).

But the Canadian Bankers Association article has data going bak to the 1990’s.

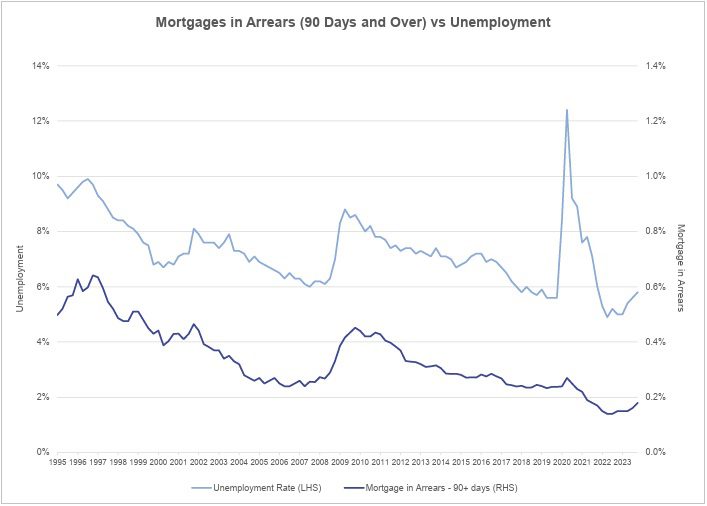

And while the following chart from the article is intended to plot unemployment against mortgage arrears, I want to draw your attention to the expanded data on mortgages in arrears:

In my chart above, I showed you 2013 to 2025, and the conclusion you’re supposed to draw is, “Yes, the rate has increased, but it’s still low compared to 2013 – 2016.”

Showing you this chart now, your conclusion should be, “Mortgage in arrears have really never been lower than the past five years.”

It’s all relative.

It’s all perspective.

And if I could conclude with an annoying catch phrase that hit its peak of overuse around 2003, “It’s all good.”

I expect to see more articles about mortgage delinquencies, mortgages in arrears, and mortgage defaults in the coming months, but I’m going to conclude that it’s much ado about nothing.

Disagree if you choose, but there’s no denying the data above.

Appraiser

at 8:37 am

Soundest banking system in the world – Canada.

Most stringent underwriting in the world – Canada.

Serge

at 8:39 am

I agree it is a nothingburger, like mortgage cliff. And it is because of the political will of the government, unlike in the US. Just today in CBC an UBC professor explains it:

Kershaw says Canada has made a “political bargain” for the last 25 years that has eroded financial security for young people, in order to protect housing wealth windfalls for older generations. “Politicians generally are going to say we need to protect the nest eggs of an older demographic. But the people providing the protection are actually younger people who, quietly and without any fanfare, pay higher rent and delay getting into home ownership, if not cancelling that dream entirely,” Kershaw said. “They’re reducing their standard of living to provide protection. They’re like shields against what might otherwise cause risks to the wealth that has been accumulated in housing by people my age and older.”

So, no cliff, no delinquencies.

RPG

at 10:55 am

Dr. Paul Kershaw.

He’s essentially declared war on seniors.

David wrote about him a few times last year.

Serge

at 2:11 pm

Thesis that reduction of standards of living by youngsters somehow protects oldsters, seems not explained. Unless, the solution is crashing RE prices and allowing youngsters to buy RE from oldsters for peanuts and in this way to increase standars of living. If that is what he meant. But, definitely, the gov does not want it, and protects homeowners (including young homeowners).

Marina

at 9:16 am

Mortgage delinquencies at the moment mean nothing. From a bank perspective, the bank cares in one of two cases:

1. Increased risk which becomes high enough to affect its business – things like it has to tighten is lending rules for new borrowers, or keep more cash on hand or whatever. Currently delinquencies are so low that it really doesn’t matter.

2. Danger of having to foreclose. Contrary to popular lore, the bank does NOT want to own your house. Ever. It’s a massive increase in liability – taxes, insurance, maintenance, etc. But the market is still strong, so there is no danger of this. Either the client will sell the house, or the bank will. But it will NOT be staying on the balance sheet for long. So it really doesn’t matter.

As long as the house can easily be converted to cash, it’s not an issue. It may be an indicator of things to come, but a pretty far off indicatior.

Now if the real estate market finally “crashes”, then it’s a whole new ball game.

Finally, quick public service announcement. If you are in danger of not being able to make your mortgage payment, call your damn provider! They WILL work with you. You’d be surprised how many options a lender has to make sure they don’t end up owning your house.

Derek

at 10:05 am

Regardless of whether the current delinquency number is “significant”, there must be some utility in the measure for our economic masters, no? The first chart shows a somewhat rapid decline, 2020 to late 2022 and then, kind of a flat “bottom”, and then a pretty sharp reversal. Why the decline, why the bottom, why the reversal? Who cares? Nothing to see here?

Serge

at 2:27 pm

By Thursday, new March numbers should trickle in, so, may be David would explain them to us….

Derek

at 4:22 pm

What’s to explain? Good listings are moving fast and over asking, but there are very few quality listings out there. Not only that, prices are not even falling like the real estate haters want. Until next month then… 🙂

T

at 7:58 am

mortgage renewal cliff – overexaggerated. mortgage deliquencies – nothing burger.

how about people unable to close on new build condos? and then getting sued?

“This condo investor is being sued for $860,000 for failing to close. He’s one of dozens facing lawsuits as default rates soar” today (apr 1) on the star. April Fools or a legit danger?

Derek

at 11:09 am

April fool’s. It’s not a real variable to be considered in assessing the state of the market because people like that are bad people and stupid . Those people deserve what they’re getting so you can’t really include those pre-con price drops as part of the whole, when taking the temperature of where real estate was, is now, or will be for the foreseeable future. Nothingburger.

David Fleming

at 8:54 am

@ Derek

😲

Ace Goodheart

at 7:25 pm

In Ontario, it is rare to see a lender foreclosing on a mortgage. This happens mostly with private mortgages.

Large institutional lenders generally use the power of sale provision in the mortgage contract.

Gord McCormick

at 10:13 am

With mortgage delinquencies so low….why does CHMC (and others) still have to charge 2.8-4.5% “insurance” ( or is it a “tax”) on most first time buyer high ratio mortgages?

Broker Gord

Ottawa