Here’s one I’ve never heard before in almost twenty years of writing this blog:

“David, you talk about real estate on your blog, but you never really talk about real estate.”

Go on…

I met somebody last week who explained that she is a long-time reader of my blog, and yet she remains disappointed that I don’t talk about specific houses or condos on the blog.

“It’s sort of like how, back in school, you’d learn all the theory, but you never really saw how it was applied in the real world.”

Continue…

She said, “I would love it if you talked about this house, that condo, and, like, talked about houses and condos that were for sale. Kind of like BlogTO and the other sites.”

Ah, see that’s where she lost me.

First of all, real estate agents aren’t really allowed to talk about properties for sale.

This sounds crazy, especially considering what you see on social media these days, but two serious RECO rules would be broken:

1) Unauthorized advertising. What constitutes “advertising” is a grey area, but posting the address and photos of a competitor’s listing under contract is breaking a major rule.

2) Disparaging a competitor’s listing. Licensed agents are not allowed to say anything deemed disparaging, which means they couldn’t have an honest, open conversation about a property for sale, unless the feedback was one-hundred percent glowing.

Now, if you throw TRREB into the mix, there’s a third rule that agents break all the time:

3) Posting sold data. We won’t get into the history here, but TRREB does not allow Realtors to post “sold prices” publicly. And yet we all know a thousand agents who do this on social media daily…

Now, back to the comment from my long-time blog reader.

She lost me at the mere mention of “BlogTO,” which is a publication written for broke and angry Gen-Z’ers, which is why food critics and travel bloggers are constantly writing about the impending doom in the Toronto real estate market.

But her point is taken.

I don’t update readers with real-time articles about new property listings.

I don’t post sexy photos of hot new lofts or renovated mansions.

I don’t shovel real estate porn on the daily.

I think that’s a different target market, and to be quite honest, you wouldn’t be reading this mass of text if all you really wanted was to scroll through photos of kitchens with bottles of San Pellegrino and bowls with green apples on the counter….

Having said that, there’s been a lot of discussion about “affordability” in the market of late, and I figured it was time to address the topic.

But addressing and discussing only go so far.

Examples are needed for illustration!

On Saturday, I typed “Toronto Real Estate” into Google, and here were the results:

“Less than $300,000.”

“Think you can’t afford Toronto?”

“Prices are dropping.”

“Price slashed $600,000.”

Every headline is about the market having declined, or affordability, or both.

So today, rather than simply discuss the concept of affordability, I want to show you some examples of what’s out there in the market, and provide data to further contrast and compare various levels of affordability.

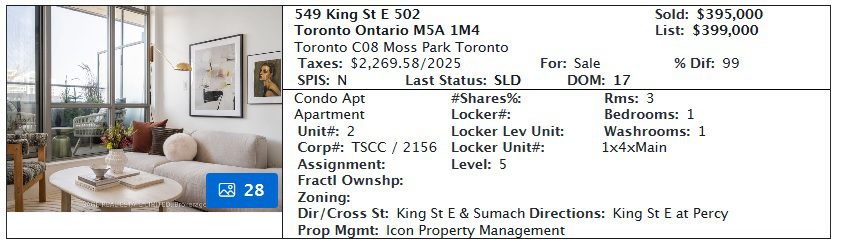

Let me pick a property that I really liked for my example.

This one here:

Whoever bought this condo is a genius.

549 King Street East is one of four buildings (along with 510 King Street, 569 King Street, & 52 Sumach Street) that form the “Corktown District Lofts.”

This building is low-rise, only seven storeys and 134 units, and was built in 2011.

It’s a soft-loft style building where the units have 10-foot ceilings, polished concrete floors, floor-to-ceiling windows, and generous outdoor spaces.

Corktown is a stone’s throw from a variety of other fantastic areas: St. Lawrence Market, Distillery, & Canary District, just to name a few.

This condo is a 503-square-foot, 1-bedroom, 1-bathroom unit, with an open concept layout.

It sold for $395,000 in January.

Let’s say that you’re a first-time buyer and you’re considering getting into the market.

I’m not going to pretend like everybody has a 20% down payment, just to make my numbers sound better, so let’s assume somebody buys this with 10% down.

Here are the parameters:

-$39,500 down payment

-30 year amortization, 3.74%

-$1,669.17 monthly mortgage payment

-$503.46 monthly maintenance fees (those are high!)

-$189.13 per month property taxes

-$50 per month for hydro (water and gas are included)

All told, the buyer of this condo would be on the hook for about $2,411.76 per month.

This unit would likely lease for $2,200 per month, so why would anybody buy this rather than leasing it?

First of all, you have to consider that about $548 per month of that $1,669.17 mortgage payment comes back to the buyer in the form of principal repayment.

So factoring that into the equation, the net cost to the buyer here is $1,863.76 per month.

That’s a lot less than the $2,200 per month lease cost, right?

Second of all, and here’s where I’m going to lose the perma-bears, but the real estate market is going to come back. It always has. It always will. Maybe not this year, or next year, but if you think that the real estate market will stay at this level or decline in perpetuity, then you belong on YouTube and TikTok and not here on TRB…

With a 10% down payment, this means the investment is leveraged ten times over.

When the buyer of this condo goes to sell it down the line, he or she is making a tenfold return on investment.

The counter-argument is, “But David, if the condo is worth less in five years, then that person’s loss is magnified tenfold!”

Fine. Come back here in 2031, and we’ll talk.

In any event, I don’t want this blog post to be about market predictions, so even if we took appreciation out of the equation, we still have a buyer who is paying less for the unit each month than it costs to rent.

But does that make the unit “affordable?”

I suppose we would have to define “affordable” first, wouldn’t we?

As we search for a definition, perhaps the low-hanging fruit here would be to look at affordability on a relative basis. That is to say, how does affordability today compare with affordability yesterday?

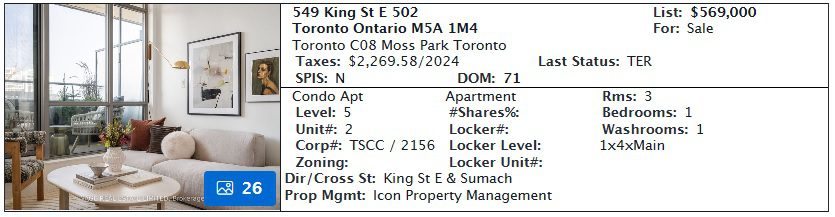

What would the unit above have cost several years ago?

Well, we need to simply look at the MLS archives to see what it might have or could have been worth:

Ah, okay! Now we’re on to something!

At one point, not too long ago, this was a $569K unit, or thereabouts.

So let’s re-run our example above, assuming a $565,000 purchase price.

-$56,500 down payment

-30 year amortization, 3.74%

-$2,387.55 per month mortgage payment

-$503.46 monthly maintenance fees

-$189.13 per month property taxes

-$50 per month for hydro

In this scenario, the buyer is paying $3,130.14 per month for the unit, compared to $2,411.76 today.

On a relative basis, this means the unit is “more affordable,” doesn’t it?

But wait!

We’re using today’s interest rate when we’re calculating numbers from yesteryear.

The Bank of Canada has cut the key lending rate from 5.00% all the way down to 2.25%.

So let’s re-run the above scenario with a mortgage rate of 5.74% instead of 3.74%.

This time around, the monthly mortgage payment is $2,986.28.

Add in maintenance fees, taxes, and hydro, and the monthly cost increases to $3,728.87.

So that’s $3,728.87 three or four years ago versus $2,411.76 today.

There’s no way to deny that this meets the definition of “more affordable,” since the “more” part of that term can be measured mathematically.

But can we now conclude that this is “affordable” in 2026?

What constitutes real estate being “affordable”? How do we define it?

One definition of the word reads: reasonably priced.

Another definition reads: inexpensive.

To me, those are very, very different definitions!

Shall we ask our federal government for help on this?

Here’s a link for you:

“Affordable Housing In Canada”

And here’s a graphic from the website that I think warrants a discussion:

Wow, they really went right for the jugular here, eh?

They started with homelessness as a type of housing, and named six types of housing before they arrived at “market housing.” Clearly a discussion for another day…

In any event, this is the definition that the government provides for affordable housing:

In Canada, housing is considered “affordable” if it costs less than 30% of a household’s before-tax income. Many people think the term “affordable housing” refers only to rental housing that is subsidized by the government. In reality, it’s a very broad term that can include housing provided by the private, public and non-profit sectors. It also includes all forms of housing tenure : rental, ownership and co-operative ownership, as well as temporary and permanent housing.

Less than 30% of a household’s before-tax income, you say?

In our case above, where the carrying cost for that condo is $2,411.76 per month, that would mean this individual would need to make $96,470.40 per year in salary to meet the definition of “affordable.”

Of course, I’m saying “individual” and not “household,” as I’m speaking to the notion of a young, enterprising, risk-taking individual who buys a condo for $395,000 in 2026 that was apparently worth $565,000 several years ago. If we were to make this a young couple and look at their combined income as a true “household” income, then we’re not even having a conversation about affordability.

It’s worth keeping in mind as well that we’re also talking about the salary for an individual working and living downtown, which I would assume is a higher salary than most other areas of the city.

In any event, I think the following question is now warranted:

Should we expect an individual home-buyer in 2026 to be able to purchase a property and pay 30% of their gross income, in order to meet the government defintion of “affordable?”

I’m not trying to move the goal posts here, but rather I’m suggesting we consider expectations.

The chart above notes that “affordable housing” is one step below “market housing.”

Would anybody expect a world-class city like Toronto to have housing that’s “affordable,” and thus below the definition of “market housing,” across the board?

Let’s take a step back for a moment and revisit this 30% threshold.

That’s for the government’s definition of “affordable housing.”

Historically, we would use a “Gross Debt Service” ratio, or GDS.

The universally accepted GDS ratio (mortgage, taxes, utilities, maintenance) is 39%.

For the person buying the condo above, with a $2,411.76 per month commitment, that 39% ratio would mean the individual needs to make $74,208 in salary.

Now, if we’re talking about an individual buying a home in the downtown core of a major world-class city, can’t we assume that this individual makes $74,208 or more in salary in 2026?

Maybe. Maybe not. Maybe some. Maybe most.

But for the rest, they can rent the same condo for $2,200 per month, remember? With a 39% GDS ratio, that’s a salary of $67,692.

For individuals who do not have a salary of $67,697, at the risk of sounding insensitive, dare I say that maybe, just maybe, living alone in a condo downtown isn’t an inherent right?

How that factors into the definition of “affordable,” I don’t know. Google’s AI probably isn’t going to work my opinions into their definitions, but I think my point is fair.

Again, I need to go back to the concept of expectations.

I’ve used this example many times, but consider a young person who works at Bay & Bloor, who complains that housing is “unaffordable.”

Where does that person live?

Bay & Bloor.

If that person makes $67,000 per year and is having trouble making ends meet while renting a condo for $2,400 per month at Bay & Bloor, then what’s stopping that person from renting at Warden & Danforth for $1,700 per month? Heck, what’s stopping that person from splitting a two-bedroom with a roommate, moving to Pickering, and spending a mere $900 per month on rent while using the savings for a GO Train pass?

Did I just run off topic?

No. I’m proving a point about “affordability.”

It’s simply impossible to define, since we have to take expectations, personalities, and societal norms into account.

We can’t just use a definition that’s handed to us, because as we’ve just seen, it’s trying to squeeze a round peg into a square hole.

Housing is “unaffordable” to Jimmy because his rental at Bay & Bloor costs him 43% of his gross salary. But this ignores the fact that Jimmy chose to rent for $2,400 per month at Bay & Bloor rather than look for alternatives.

My point is this:

Not only is that $2,400 per month today, down from $2,700 per month two years ago, but our $395,000 condos with 3.74% interest rates are down from $565,000 with 5.74% interest rates.

Affordability has returned to the Toronto market. There is simply no question about this.

Whether or not our expectations, spending habits, wants vs. needs equation, and definition of true physiological needs are in line with economic reality is an entirely different story.

–

P.S. –

I’m publishing a podcast on Last Honest Realtor this week called “Why People Love To Hate Toronto Real Estate.”

I think it might play into this topic.

I’ll provide a link once it’s uploaded.

Here’s the link:

Francesca

at 10:08 am

For a first time buyer who doesn’t have a current property to sell this is the perfect time to get into the market into a starter condo as I don’t think these low prices will be here permanently. I know of two friends who’s kids have bought their first one bedroom condo in their mid to late 20s now and are thrilled to have gotten a “discount” compared to if they had bought a few years ago. One could argue that no Toronto is still not affordable compared to Ottawa or Peterborough but many young people aren’t willing to sacrifice location until they need more space for a growing family so they will pay the higher prices to stay central, close to their jobs. I also think this is now a great opportunity to upsize into a larger condo as those prices have dropped significantly too. Toronto will never be “affordable” but like David said you cannot expect it ever to be in relation to other places in Canada. I would say its less expensive now not necessarily more affordable because in my mind affordable implies within reach of anyone who wants to buy with todays average income

Serge

at 3:26 pm

I have read somewhere about 3 years ago that in B.C. developers get government loans to build “affordable rental housing” interest-free or something. They have to promise to charge no more than 30% of the gross median income in Vancouver. That happened to be about 2500 for one-bedroom (I do not recall exact numbers). Et voila, developers prosper! And the government is happy. Probably, the same thing in Toronto… it is all about the median.

Frances

at 8:58 am

Why didn’t you direct that lady to your Pick 5 videos, where you cover exactly those things?

Derek

at 10:21 am

David, are you really trying to make the argument that it is more affordable to pay a lower price, have a smaller mortgage, with a lower interest rate than it is to pay a higher price, have a bigger mortgage, with a higher interest rate? How did you come up with that crazy logic?

Derek

at 12:20 pm

On the other hand, according to realtor, Jon “pew pew” Flynn:

“Mortgage payments on the average Canadian home are still 36% higher than before the pandemic insanity. Don’t forget they were already inflated back then.

Jan 2020, $2,145/mo

Jan 2026, $2,926/mo”.

Vancouver Keith

at 2:22 pm

Great assets do not go down in price that often. But even Canadian bank stocks have a big correction about every ten years. Toronto condos are an opportunity right now, you are absolutely right. You may not buy at the bottom, but in a decade todays buyers will most likely be in a pretty good position.

David Fleming

at 2:45 pm

@ Vancouver Keith

As I argued in my latest podcast, the younger generation has to make a very difficult decision:

“Do I buy a condo now, with prices depressed, and balance the potential downside with the potential upside, or do I simply not act at all?”

There’s a massive opportunity out there right now, but this generation has to do something hard: they have to make a decision.

Here’s the link:

https://www.youtube.com/watch?v=h1LIOvsOuY0&feature=youtu.be

Different David

at 4:00 pm

Spot on. This generation refuses to make decisions. They want their lives handed to them with all decisions made.

They would rather live for the moment, spending thousands on event tickets, instagrammable vacations, and food experiences. Telling them that they have to commit to a mortgage and that 1/3 of their mortgage payment is coming back when they sell doesn’t make sense.

Derek

at 5:56 pm

It feels like we’re going back to the “have fun staying poor” mocking of the renters? So soon? I’d be more on board with it if we had told anyone not to get in, in late 2021-22 because we were calling a top and years of subsequent decline. Or, if we had told anyone, year after year for the past 5 years that the decline was still declining and would continue to decline. Or, if we had told anyone that the rate cuts would not actually result in immediate rockets, or shortly thereafter rockets, or any time now trust me rockets.

cyber

at 9:08 pm

I don’t think the issue is a mortgage payment commitment, but the sacrifice or the duration of saving for the down-payment for those who are some combination of: not in top 10% of earners / not getting a substantial gift from parents / not married / not getting to stay with parents for free while saving

So many renters will complain how they “hate paying the landlord’s mortgage”, and how hard it is to save while also just living when not subsidized by parents.

Many just give up on ownership alltogether, and this should come as no surprise and is not some “moral flaw”. I, too, would get that avocado toast for brunch if I only had an “average” job, no working spouse, and looking at the prospect of 10 years of no fun whatsoever to scrimp for a down-payment on a 1 bed condo within 60 min of one way rush hour commute to the job.

addressbox

at 7:28 am

This article makes a great point that “affordability” in real estate is often relative rather than absolute. Even though prices and interest rates have improved compared to a few years ago, the real question is whether housing costs fall within a reasonable share of income. In Canada, housing is typically considered affordable when it costs less than 30% of a household’s income.

Discussions like this are valuable for real estate platforms such as Addressbox, which aim to help buyers understand how market trends, financing costs, and personal expectations all influence what truly counts as affordable housing.