“How long is a piece of string?”

It’s a trick question, see. Because there isn’t really an answer.

A piece of string can be any length, from zero to infinity. But it can also be measured in millimetres, centimetres, inches, feet, meters, or anything you choose, right down to a furlong if you’d like.

Now, if you had a physical piece of string, and you knew that it was sixteen inches long, you could ask the following:

“Is this piece of string long?”

It’s another trick question, see. Because, again, there isn’t really an answer.

Is this piece of string long…..compared to what? Or to whom?

Is a sixteen-inch piece of string long compared to a two-inch piece of string?

Yes.

But if you were sinking into quicksand like we all feared while watching 1980’s cartoons, and you yelled, “Throw me a rope,” you’d be highly disappointed if somebody passed you a sixteen-inch piece of rope, right?

So what is my point?

This:

Any statistic, metric, or measurement is absolutely useless without being described in a relative context.

You understand, right?

If you said, “Jimmy is a great baseball player; he had nine home runs last year,” that sounds like a small amount if Jimmy were playing 162 games in the Major Leagues, but it sounds like a large amount if Jimmy were playing an 8-game high school baseball season.

So what then do we make of this:

Well, it sounds pretty bad!

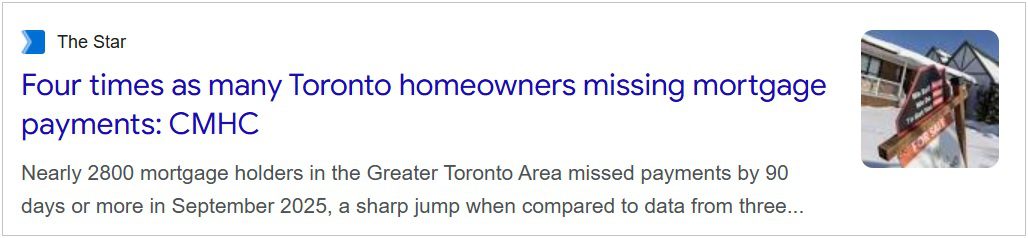

Quadrupled?

The number of people who are missing their mortgage payments has quadrupled?

This is a lot. There’s no denying it.

Then again, I’m reminded of a famous “Uncle Phil” quote when he was trying to prove a point to Carlton and Will: “Boys, what is one-hundred percent of nothing?”

One-hundred percent sounds like a lot, but when it’s applied to nothing, it’s relatively small. I remember this scene of “The Fresh Prince of Bel Air” vividly from my childhood, as Carlton & Will struggled to do the math in their heads, attempting to figure out what amount they would receive.

The point was made, however.

Everything is relative.

Earlier this month, there was a lot of media coverage about mortgage delinquencies in Canada.

Every major media outlet reported on the story from the CMHC, which you can read in full here:

“Mortgage Renewal Wave Strains Some Regions And Borrowers”

CMHC

February 5, 2026

Read the article if you have time.

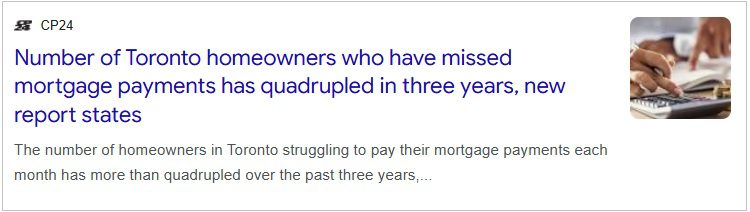

There’s a lot more in there than we would be led to believe when we were inundated last month with headlines like this:

This is the literal definition of “clickbait,” since you’re led to wonder which city they’re talking about, making you want to click the headline.

Spoiler alert: it’s Toronto.

From the article:

Mortgage delinquencies since 2022 have more than quadrupled in Toronto. Alongside higher payments, homeowners in the city are grappling with greater levels of household debt due to elevated real estate costs, while individual real estate investors face rising costs and falling rents. Falling home prices and slowing sales and a weak job market are also hampering people’s ability to cope with rising mortgage payments.

That sounds bad, right?

Mortgage delinquencies have more than quadrupled?

Damn, how is the world still spinning?

But I want to go to the CMHC report for a moment; the one which I linked above.

I want to quote directly from the report and we can see if the narrative (spin?) changes at all.

Check out this excerpt:

In Toronto’s struggling housing market, the mortgage arrears rate in the region has more than quadrupled from post-pandemic lows.

Does that look the same as the excerpt from the Financial Post article?

Nope!

Not even close!

The Financial Post article is missing four very, very important words: “….from post-pandemic lows.”

That’s incredibly important to the context of the story, and yet it’s being left out of virtually every article being written about mortgage delinquencies in Canada, from every major media outlet.

Now, let me flush out the above excerpt a little bit more:

In Toronto’s struggling housing market, the mortgage arrears rate in the region has more than quadrupled from post-pandemic lows. While arrears remain low, they’re projected to continue rising over the next year.

Again, we’re gaining more context!

The important words here are: “….while arrears remain low.”

They do remain low. They arelow. They’re projected to rise, but that would still make them low.

So then, what’s all this talk of quadrupling?

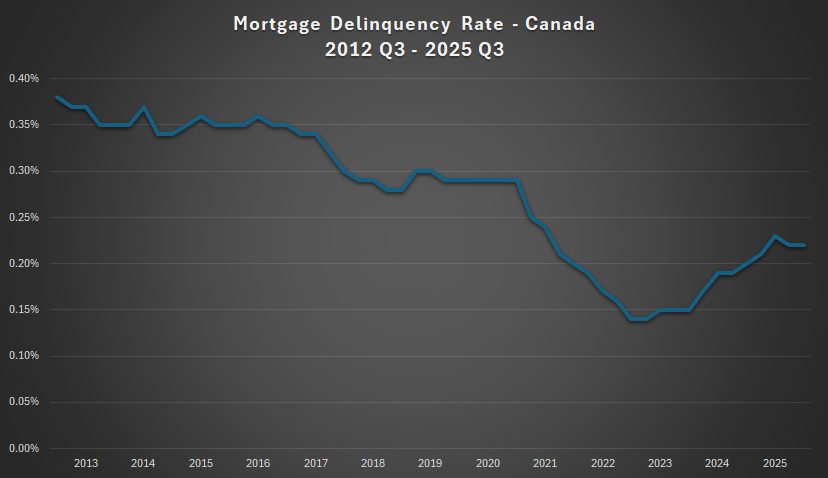

In September of 2022, we hit the lowest level of mortgage delinquencies at 0.06%.

In December of 2025, that number had risen to 0.28%.

There’s your “quadruple” right there.

But without proper context, and without measuring these numbers on a relative basis, you’re going to simply assume that this “quadrupling” signals the level of doom that the headlines want you to.

But what does history say?

Measuring a small piece of string against a smaller piece of string would render that first piece of string large.

But in the article above, we noted that we were measuring from “post-pandemic lows.”

Let me re-word that:

We were measuring from the all-time low point for mortgage delinquencies.

If the all-time low is your starting point, then surely you can’t be surprised when the figure increases, right?

So let’s go back further than “post-pandemic,” shall we?

Let’s measure today’s length of string against lengths of string from before the all-time low.

It would look something like this:

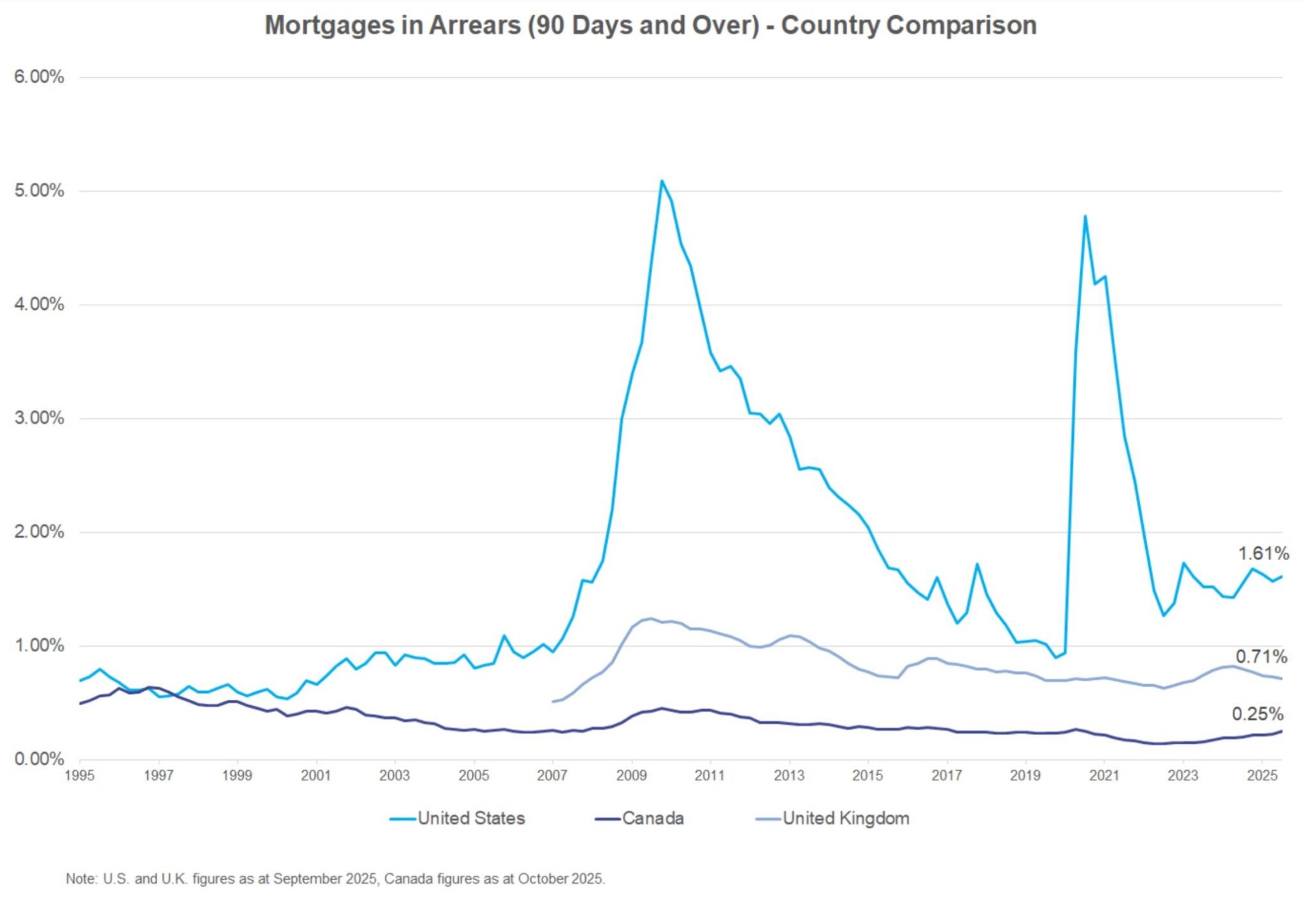

If memory serves me correctly, I wrote a blog post on this subject about one year ago. I distinctly remember making these charts with the data available through the CMHC.

Mortgage delinquencies did increase over the last year, and there’s no denying this.

But mortgage delinquencies are still well below anything outside of pandemic-affected levels, as the above chart shows.

What was also left out of the media coverage on this topic was the positivity in the CMHC report, but that comes as no surprise, as most of the headlines were click-bait in nature.

Here’s an excerpt from the CMHC report:

Mortgage arrears are rising but remain below historical levels

With financial pressure increasingly weighing on households in a very tangible way, mortgage arrears have been steadily increasing nationally since late 2023. This trend is evident across the many mortgage arrears indicators in Canada, each coming from different data sources. While this upward trend is clear, mortgage arrears levels remain low compared to earlier periods of economic difficulty. This reflects several underlying factors:

1. Mortgage borrowers continue to show strong resilience.

Canadian households have been playing financial Tetris very well, adjusting their budgets and even making some sacrifices to make ends meet. As long as income remains steady, most households are staying on track. Historically, however, rising mortgage arrears have been closely tied to increases in unemployment. Without stable income, even the most carefully structured budgets can be quickly disrupted.

2. Homeowners have prioritized short-term affordability over long-term debt exposure.

At renewal, most mortgage consumers chose to increase their amortization period to lower their monthly mortgage payments. This has kept payment increases smaller than expected, even though it means paying more interest and carrying their mortgage for a longer time. Choosing longer amortizations suggests that buyers are prioritizing either accessing homeownership or reducing immediate debt pressures over optimizing long-term financial health. As housing has become increasingly unaffordable, this trend highlights a growing reliance on short-term liquidity pressures at the expense of long-term wealth accumulation.

3. Income growth and labour market conditions have been generally solid…until recently.

While Canada’s labour market has softened, with unemployment rising, this increase has been concentrated among younger workers and recent immigrants—groups that are typically not yet homeowners.

4. Regulation has played an important role in limiting mortgage arrears growth.

Mortgage arrears could have increased more significantly and at a faster pace without regulation. Canada has gone through a wave of regulatory tightening since the global financial crisis (see Appendix 2). Even though Canadian homeowners felt the 2008 to 2009 recession less intensely than our southern neighbors, the federal government introduced a series of changes. The goal was to protect overall financial stability in Canada.

Notably, mandatory mortgage stress testing was introduced, in 2016 for insured mortgages and 2018 for uninsured mortgages. The stress test requires borrowers to qualify for their loans at higher potential interest rates. This means that when mortgage consumers qualified for their mortgage loans a few years ago, their ability to handle higher payments was assessed based on their income at the time. This measure helped ensure they could afford a rate increase.

Fast-forward almost a decade, and recent trends show that the stress test has served its purpose. Even with interest rate shocks, arrears have risen gradually rather than sharply. Without the safeguards of the stress test, the increase in arrears could have been much steeper. That said, it’s not bulletproof. As outlined earlier, risks are becoming more evident in certain regions, like Toronto and, to some extent, Vancouver.

“Mortgage borrowers continue to show strong resilience.”

This was not echoed in the media articles earlier this month, as headlines sought to scare people into believing that half the homeowners in the country were about to hand over their front door keys.

No, but rather, we were seeing headlines like this:

That’s sexy A-F, right?

A headline like that is going to get c-l-i-c-k-s, y’all!

Misery loves company, and as I explained in my Last Honest Realtor podcast on Monday, a lot of people in this city love to hate real estate. So why wouldn’t they click on that link?

Here’s another good one:

This is all about shock value, of course. That much is clear.

A trillion dollars is a lot of money. A number like that is going to get eyes.

Of course, there’s absolutely zero context here. It’s just a really long piece of string; the longest you’ve ever seen!

But what does this number actually mean?

I wonder how many people read the article, and how many simply concluded, “There’s way too much debt in Canada!”

But back to our piece of string, for a moment.

While Canada’s piece of string might be long(er) than it was before, if it’s measured against that of the Yanks and the Brits, it doesn’t look so bad, does it?

It’s also important to note, as we have done before in this space, that while the United States saw a massive surge in mortgage delinquencies during the 2008 Financial Crisis, our country did not.

In case you missed this from the CMHC report above, bullet point #4:

Canada has gone through a wave of regulatory tightening since the global financial crisis. Even though Canadian homeowners felt the 2008 to 2009 recession less intensely than our southern neighbors, the federal government introduced a series of changes. The goal was to protect overall financial stability in Canada.

I don’t credit the federal government very often, but they did an excellent job in 2008 and beyond in strengthening our banking system.

The result, in my opinion, is a country with exceptionally low mortgage delinquencies, despite what the media has been reporting throughout the month.

If you feel the preceding was a great example of, “Me thinks thou doth protest too much,” then I’m all ears!

Tell me I’m wrong. I promise, I’ll listen…

Serge

at 9:00 am

2008-2009! Were not those years with 0% downpayment and 40 years amortization?

The market needs them back.

David Fleming

at 11:33 am

@ Serge

In 2005, I sold a house for $1,070,000.

My client submitted a deposit of $50,000.

Upon closing, the lender advanced $1,070,000 to the seller, and then gave my client a cheque for $124,900.

That $124,900 represented the return of his $50,000 deposit as well as 107% financing for the home.

107% financing.

On a purchase of $1,070,000.

My client bought a house without putting any money into it AND received 7% of the value of the home as a loan.

That was a crazy time!

Serge

at 4:06 pm

Thanks, David!

Yeah, many people were sad that missed this opportunity.

Other people (including one famous anti-RE blogger who lost his ministerial position due to opposition to this decision of Harper, as he says) say that that was the origin of investor-fueled RE spiral, which came to the dead end now.

As to mortgage arrears I agree these numbers are nothingburger. Moreover, there is no breakdown if they are people with 15 years of mortgage, or recent investors / flippers who cannot sell their condos / houses.

Derek

at 9:29 am

The delinquency number must describe something about the broader market, no? Why so low when it bottomed? Why has the trend changed since bottoming? What does the trend say about the market? A rising delinquency rate means what? Absolutely nothing?

cyber

at 2:32 pm

TRREB reports 3,082 sales in the GTA for January 2026, versus 17,975 in active listings (roughly 6 months of inventory on average, obviously heavily over represented by “dog crate” condos no one wants).

CMHC report points to 2,797 mortgages in Toro to area being in arrears, ie over 90 days overdue

https://share.google/cILFa0bkapmYXU1uN

Assuming most mortgage holders who are behind on payments will try to sell, a significant chunk of properties that actually move/transact in the current market vs continue to sit unsold likely involve very “motivated” sellers

David Fleming

at 10:14 am

@ Cyber

Exactly.

The properties that ARE selling are the dog-crate condos, as you say, which are forced sales.

I know I sound like a broken record, “There’s no quality inventory out there,” and some of the readers have called me out on this, but an overwhelming amount of the inventory out there is garbage.

Serge

at 12:26 pm

Is not “one man’s treasure – another man’s garbage”?