This was quite possibly the best book I’ve ever read.

And even though I’ve read American Psycho as well as The A-Z Encyclopedia of Serial Killers, I still believe that “The Big Short” is likely the most disturbing book I’ve ever read.

People always say, “You’ve gotta read this book,” but rarely is that genuine advice taken. Rather then tell you all that you simply must read the book that details how America caused their own economy to implode beyond anything that capitalism has ever seen before, I’ll just outline my favourite quotes from the book and perhaps you can use this as a synopsis of sorts…

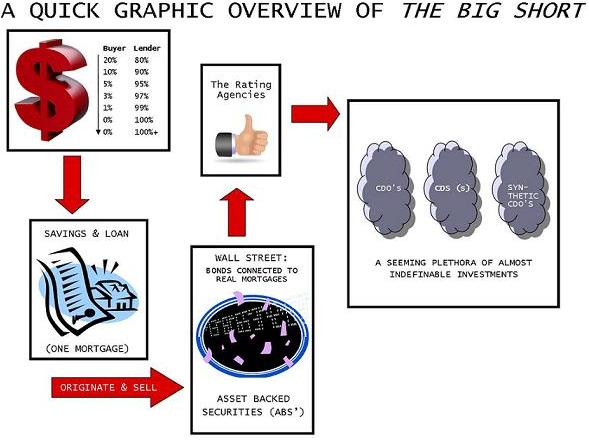

The above graphic tells the whole story.

First, lenders began giving money to people that had no business getting money. If you had an income of $14,000, you would qualify for a $724,000 loan.

Then, crappy mortgages were bundled and sold as asset-backed-securities.

Following this, the ratings agencies, notably Moody’s and Standard & Poor’s, were duped into rating these crummy B-level investments as AAA.

Finally, these instruments were packaged as CDO’s, CDS’s, and basically ABC’s and XYZ’s.

People defaulted on their mortgages, and the whole system imploded.

Here are my favourite quotes from the book…

Meredith Whitney’s comment on Wall Street brokerages that started the whole market collapse:

“You’re wrong. You’re still not facing up to how badly you have mismanaged your business. You’re still not acknowledging billions of dollars in losses on subprime mortgage bonds, The value of your securities is as illusory as the value of your people.”

Steve Eisman on the pressure to not rate companies with a “sell”:

“I put a sell rating on the thing because it was a piece of shit. I didn’t know that you weren’t supposed to put sell ratings on companies. I thought there were three boxes – buy, hold, sell – and you could pick the one you thought you should.”

Steve Eisman defending his “sell” rating on Lomas Financial Corporation after they claimed they were “hedged against market risk”:

“The Lomas Financial Corporation is a perfectly hedged financial institution: it loses money in every conceivable interest rate environment.”

Steve Eisman explaining a savings & loan’s theory on checking accounts:

“Someone asked him if he believed in the free checking model, and he said, ‘Turn off your tape recorders.’ And he explained that they avoided free checking because it was really a tax on poor people – in the form of fines for overdrawing their checking accounts. And that banks that used it were really just banking on being able to rip off poor people even more than they could if they charged them for their cheques.”

Eisman asked, “Are any regulators interested in this?”

“No,” said Sandler.

“That’s when I decided that the system really was, ‘fuck the poor.'”

Michael Lewis:

“Back in 1996, 65 percent of subprime loans had been fixed rate, meaning that typical subprime borrowers might be getting screwed, but at least they knew for sure how much they owed each month until they paid the loan off. By 2005, 75 percent of subprime loans were some form of floating-rate, usually fixed for the first two years.”

Michael Lewis on a BS instrument called “the interest-only negative-amortizing adjustable-rate subprime mortgage”:

“You, the home buyer, actually were given the option of paying NOTHING at all, and rolling whatever interest you owed the bank into a higher principal balance. It wasn’t hard to see what sort of person might like to have such a loan: one with no income.”

Mike Burry on Goldman Sachs’ mishandling of mortgage bonds:

“This was shocking to me, actually. They were all priced according to the lowest rating from one of the big three ratings agencies. It was as if you could buy flood insurance on the house in the valley for the same price as flood insurance on the house on the mountaintop.”

Steve Eisman on the tactics of subprime lenders:

“They were making loans to lower-income people at a teaser rate when they knew they couldn’t afford to pay the go-to rate. They were doing it so that when borrowers get to the end of the teaser rate period, they’d have to refinance, so the lenders can make more money off them.”

Steve Eisman on Gregg Lippmann – one of the pioneers of credit default swaps:

“Why are you asking me to bet against the bonds your own firm is creating, and arranging for the ratings agencies to mis-rate?”

Related to above:

“Having gathered 100 ground-floors from 100 different subprime mortgage buildings (triple-B-rated bonds), they persuaded the ratings agencies that these weren’t all exactly the same things. The ratings agencies, who were paid fat fees by Goldman Sachs and other Wall Street firms for each deal they rated, pronounced 80 per cent of the new tower of debt triple-A.”

Michael Lewis:

“In Bakersfield, California, a Mexican strawberry picker with an income of $14,000 and no English was lent every penny he needed to buy a house for $724,000.”

Steve Eisman:

“She was this lovely woman from Jamaica. She says she and her sister own SIX townhouses in Queen’s. It happened because after they bought the first one, at its value rose, the lenders came and suggested they refinance and take out $250,000 – which they used to buy another. Then the price of that one rose, too, and they repeated the experiment. By the time they were done, they owned five of them, the market was falling, and they couldn’t make any of the payments.”

Daniel Moses on the rating’s agencies’ decision to not downgrade bonds:

“She submitted a list of the bonds she wished to downgrade to her superiors and received back a list of what she was permitted to downgrade. She said she’d submit a list of a hundred bonds and get back a list with twenty-five bonds on it, with no explanation of why.”

Charlie Ledley on the concept of the CDO:

“The more we looked at what a CDO really was, the more we were like, ‘Holy shit, that’s just crazy. That’s fraud.’ Maybe you can’t prove it in a court of law, but that’s fraud!”

Charlie Ledley and Ben Hockett:

“Wall Street was propping up the price of these CDOs so that they might either dump losses on unsuspecting customers or make a last few billion dollars from a corrupt market.”

Daniel Moses on invalid, unfair, and misleading media coverage:

“It became very frustrating that they weren’t in touch with reality anymore. If something negative happened, they’d spin it positive. If something positive happened, they’d blow it out of proportion. It alters your mind. You can’t be clouded with shit like that.”

Steve Eisman on the bleak future of the American economy during the subprime crisis:

“We are in the midst of of one of the greatest social experiments this country has ever seen. It’s just not going to be a fun experiment. You think this is ugly. You haven’t seen anything yet.”

Michael Lewis on the ridiculous cheating they called a ‘conflict of interest’:

“Of all the conflicts of interest inside a Wall Street bond trading firm, here was both the most pernicious and least discussed. When a firm makes bets on stocks and bonds for its own account at the same time that it brokers them to customers, it faces greater pressure to use its customers for the purposes of its own account.”

Michael Lewis:

“Between September 2006 and January 2007, the highest-status bond trader inside Morgan Stanley had, for all practical purposes, purchased $16 Billion in triple-A-rated CDO’s composed entirely of triple-B-rated subprime mortgage bonds.”

Michael Lewis:

“For more than twenty years, the bond market’s complexity had helped the Wall Street bond trader to deceive the Wall Street customer. It was now leading the bond trader to deceive himself.”

A classic Steve Eisman rant:

“The upper classes of this country raped this country. You fucked people. You built a castle to rip people off. Not once in all these years have I come across a person inside a big Wall Street firm who was having a crisis of conscience. Nobody ever said, ‘This is wrong.'”

In September of 2008:

“Merill Lynch, who had begun by saying they had $7 Billion in losses, now admitted the number was over $50 Billion. Citigroup appeared to have about $60 Billion. Morgan Stanley had it’s own $9-plus Billion hit, and who knew what was behind it.”

Steve Eisman sums it all up:

“The investment banking industry is fucked. These guys are only beginning to understand how fucked they are. It’s like being a scholastic prior to Newton. Newton comes along and you wake up, ‘Holy Shit, I’m wrong!'”

Michael Lewis continues from Eisman above:

“Lehman Brothers had vanished, Merrill had surrendered, and Goldman Sachs and Morgan Stanley were just a week away from ceasing to be investment banks.”

Michael Lewis on the injustice of it all:

“Howie Hubler lost more money than any single trader in the history of Wall Street ($16 Billion) and yet he was permitted to keep the tens of millions of dollars he had made (as salary and bonus).”

Michael Lewis on who lost in the end:

“By early 2009, the risks and losses associated with more than $1 Trillion worth of bad investments was transferred from big Wall Street firms to the U.S. taxpayer.”

Do yourself a favour – read this book.

Even if you can’t understand some of the lingo or can’t comprehend what’s going on, you’ll still get the gist of it.

Ten or twenty years from now, the subprime mortgage meltdown in the United States will be the subject of books, movies, and university courses. It will likely be examined as a cause-and-effect of many of the future problems in the U.S. and world economy.

It is very important to have at least a basic understanding of what went down.

LC

at 8:19 am

Self-imposed destruction. Totally decimated the credibility of the banking sector. A classic on human stupidity for decades to come.

George

at 6:46 pm

We are all inherently greedy, but some people express this greed in much more diabolical ways than others do.

The saddest part is who has to clean up the mess.

LM

at 8:33 pm

yes, but what most people don’t acknowledge is that the US government pressured banks to lend at ridiculously competitive/ lenient rate to encourage home ownership vs renting. Yes, Wall Street was greedy, but it, along with Freddie Mac and Fannie Mae, etc govt. agencies were “strongly” encouraged by the government to lend without asking too many awkward questions. So, as tempting as it might be to blame invesment bankers earning obscene salaries, in truth, they were only following orders, and then, as is human nature (come on, wouldn’t we all be driving Ferarris if we could?), they got greedy…

Frank

at 7:48 am

I would add the role of the Federal Reserve and one Alan Greenspan in particular. Sometime in the 90s Greenspan and his Republican cheer leaders became enamored with the notion that you could essentially abolish the business cycle if you just pushed interest rates low enough for long enough. Whenever the economy hit a slow patch, rather than allowing the economy to naturally work off the excesses of the previous growth cycle, Greenspan would hit the gas again. And the excesses just piled up until the inevitable implosion.

Matt

at 3:25 pm

LM (20:33:01) :

yes, but what most people don’t acknowledge is that the US government pressured banks to lend at ridiculously competitive/ lenient rate to encourage home ownership vs renting. Yes, Wall Street was greedy, but it, along with Freddie Mac and Fannie Mae, etc govt. agencies were “strongly” encouraged by the government to lend without asking too many awkward questions. So, as tempting as it might be to blame invesment bankers earning obscene salaries, in truth, they were only following orders, and then, as is human nature (come on, wouldn’t we all be driving Ferarris if we could?), they got greedy…

—

You oversimplify the situation with the US government here.

Collateralized debt obligations were packaged by the banks and sold to investors. The US government never forced banks to do this; it was CDOs that allowed the financial situation to balloon to epic proportions and spread across the planet’s entire financial system.

At the heart of this crisis are the rating agencies. Now we all know how the game truly works; even large reputable agencies like Moody’s and Fitch were turning a blind eye, probably for cash.