The word “relax” is defined as follows:

verb: make or become less tense or anxious

So be honest, folks, how many of you were truly “relaxed” this holiday season?

While there are many reasons why we may be less tense and anxious, including, but not limited to, being away from our places of work, there are countless reasons why we may be more tense and anxious!

How many of you hosted a large family gathering?

How many of you had family stay with you at your home for several days and nights?

Do either of these things provide for less anxiety?

Did you cook your very first turkey this year? What was your stress level like during those six hours?

Were you tense when your child or significant other opened that present that you hoped and prayed they would love?

How many of you attended seasonal events, ie. the Christmas Market in the Distillery, the Nutcracker, the ROM, and the like? Did the driving, parking, long lines, and large crowds put you in a calmer state than when you’re sitting at your desk on a Tuesday afternoon?

The last two weeks were a whirlwind for me, and truly and honestly, I find anything outside of my day-to-day routine to be stressful. This is quite ironic, since I work in a fast-paced, high-stress world, but I take it in stride. The stress manifests itself inside of me, but I don’t really feel stressed. Give me two weeks around Christmas-time, and I feel it. I feel it in every ounce of my being.

My brother and his family came to stay with us for three nights, beginning on the 19th, and they returned on the 27th for another two nights. It was nothing short of magical, and seeing my daughter play with her two cousins for hours and hours on end just melted my heart.

We hosted one family dinner, attended three others, and in between, visited the Polar Express Train in Uxbridge, Casa Loma, Christmas GLOW, and the Dr. Seuss Experience, which was more than merely an “experience.” It was a realization, specifically, that people are unique.

Netflix changed the way we absorb television and movies, and in essence, the way we entertain ourselves. But if you really want entertainment, simply attend a public event, and people-watch.

The Dr. Seuss Experience was utterly bizarre.

What started with the person at the door telling us two rules, continued with the person checking tickets telling us three more rules, and morphed into an exhibit of employees walking around and policing children and adults alike. There was one guy who had a megaphone and was shouting incessantly at nobody in particular. Another Seussian who guarded the balloon maze was talking into a smaller mic that emitted sound from a small speaker, located, of all places, on his belt. I felt that talking at face-level would have made more sense, but what do I know. The “rules” were explained to us at the threshold of every, single room, without fail. My two young nieces joked about it for the rest of the week.

The lady working the “Horton Hears A Who” room was incredibly concerned with the well-being of the fuzzy clovers, and repeatedly cautioned children to “be kind” to the clovers. When the room emptied, I swear on my life, she began combing the clovers with a brush, stroking them, ever-so-gently, and then talking to them. It was bizarre.

My daughter just about got lost in that room:

Every room had something different, but it was the people that made this exhibit so interesting, to me.

I thought I would blend in, but apparently not.

I was kindly asked by management not to “hog” the Bofa on the Sofa.

I had no idea what they were talking about.

But it seems that the one place I found to sit in the whole building was actually a top “selfie-spot,” and on this day, it was in high demand…

Yes, that’s how I dress when I go to events like this.

I believe I’m dressing “like a guy who is out with his kid on a Saturday,” but my wife feels differently, as do my brother and his wife, who took this creepy shot while I was reflecting on a conditional sale that was going to fall through. I’ll tell you that story next week…

The Circus McGurkus was confusing. Imagine an indoor carousel where your feet were 2-inches off the ground, that moved at a speed so slow that your 3-year-old daughter was walking by your side, and lapping you! Yes, I rode this particular carousel, simply for the amusement of the three children, none of whom rode with me. Again, I couldn’t help but feel like I was in a mad-house. Nothing made sense. Not the exhibits, nor the wacko employees, and especially not the people attending.

But the most amazing part of the “experience” was seeing a line of people, and simply conforming without thinking. We joined this line, not sure of what we would see on the other side of the door, and after explaining to the Seussian employee that we would not divide our group of seven people because six was the limit, we went inside to find….

…..well, I still don’t know.

Sneetches, apparently.

A small room, in which we crammed, surrounded by plexiglass, with Sneetches. Nothing really to do per se, but after fifteen seconds, the door opened, and we were told our “turn” was over. The adults were laughing so hard that the children soon followed.

The whole experience was just weird.

Whether it was the staff that worked there (don’t get me started on the World Record for body odour that Thing 1 & Thing 2 possessed…), or the people, it was just weird. I mean, we saw a young couple in their 20’s, dressed like they were going to a nightclub, in attendance without any children. What’s that about? Half the people there looked like meth-heads. It’s true. My niece still asks me about “Meth-Wendy,” which is a name I bestowed upon the lady policing children in the Lorax room…

Maybe in the end, it’s me that’s insane. But people-watching through Dr. Seuss, GLOW, Casa Loma, and a train ride in Uxbridge gave me so much at which to shake my head, that I almost developed a cramp.

I actually did throw my back out on Christmas morning, and couldn’t walk upright for four days, but that’s another story…

So here we are, back to our routines, and I’m simply asking for an honest show of hands – how many of you felt truly relaxed over the holidays?

As we turn the page to another year in the Toronto real estate market, we all seem to be entering the fray at different speeds, and even different times.

I’m currently writing this on December 30th, as I sit alone in my office at 290 Merton Street. There is one staff at front desk, and I’m the only other person in the building. All of our other offices are closed.

When does the year start anew? Is it January 2nd? Or “back at it” on January 6th?

For all intents and purposes, let’s say we’re back on the 6th, because I don’t see much happening during the preceding half-week.

And then what should we expect? When do new listings start coming out?

Well, I’ve got a condo listing coming out this week, as well as two properties for lease. But beyond that, we’re sort of pushing toward the end of the month, and even beyond.

I have a client who will be re-listing a property that wasn’t sold last year (with another agent), and I told them, “If you can wait until the spring, do it.” They’ll spend money to carry the property, but it’s worth waiting for better weather, just based on the type of property.

Then I have another home-seller who wants to be the “first, great house on the market in 2020.” From a strategy standpoint, it makes sense. Strike while the rest of the market is sleeping.

I expect the start of January to be very slow, and many agents that I know are taking extended vacations until the end of this week, returning on Monday in what is almost “mid-month.”

So without much in the way of market activity to discuss, I figured we’d take a look today and on Wednesday at the top discussion points of the year ahead. This is not going to be a “predictions” post as it has been in years past, simply because my predictions are just as likely to be correct or incorrect as yours, and also because within every discussion point, you can surely expect some opinion and prognostication.

I’m also not going to count down in reverse order, since I think we should start with the most important.

–

Discussion Point #1: What is going to happen with home prices?

Interesting!

Or boring, if you feel we’ve covered this far too often.

But any discussion about the real estate market surely touches on prices, if not directly focuses on them.

I’ll give you my prediction right now, since it’s simple: I predict that Toronto home prices are going up. Tell me I’m being a salesperson, and once again, I’ll tell you that we purchased our forever-home in 2018, so I did put my money where my mouth is.

I think that both 416 condo prices and 416 freehold prices will finish the year higher (and by that I mean November 2019 vs. November 2020, since I don’t recommend using December), and if you want to use the average sale price for all months during the year, I will predict that figure rises too.

As for the rest of the GTA, it’s anybody’s guess.

We all know that the “outskirts” have been weak over the past two years, and anecdotally, I think we’d suggest that ‘some areas’ are down 20-30% from the peak in April of 2017.

But it wasn’t until I sat down and charted all the data that I really got a picture to understand where things were, where they went, and perhaps shed a light on where they’re going.

TREB divides the Greater Toronto Area into seven districts: Toronto, York Region, Durham Region, Halton Region, Peel Region, Dufferin County, and Simcoe County.

Since we really don’t care what’s happening in Barrie, we focus on the first five areas in the context of “Greater Toronto.”

It’s been my contention that the 416, or Toronto-proper as most people think of it, has been the least affected area since the “drop” in April of 2017, and I’ve shown in the past two years that prices are actually much higher in certain areas of market segments.

But what of the rest of the GTA?

Here is the average sale price for each of the five areas over the past three years:

My immediate observations are as follows:

1) The area with the most volatility is Toronto.

2) The area with the least volatility is Durham, where prices don’t seem to have moved much at all since the fall of 2017.

3) It’s quite hard to ignore that bright, yellow cliff in mid-2017.

Beyond that, this looks like any other chart.

But in case your eyes aren’t doing the math for you, let’s look at how November of 2019 sale prices compared to the “peak” in April of 2017:

Halton:

April, 2017: $981,544

November, 2017: $892,034

Peel:

April, 2017: $790,298

November, 2017: $769,434

Toronto-416:

April, 2017: $943,947

November, 2017: $910,419

York:

April, 2017: $1,198,229

November, 2017: $974,771

Durham:

April, 2017: $702,768

November, 2017: $611,872

This provides us with respective price changes of:

Halton: -9.1%

Peel: -2.6%

Toronto: -3.6%

York: -18.6%

Durham: -12.9%

And while the “peak” occurred in April of 2017 for Peel, Toronto, York, and Durham, if we used the true “peak” for Halton in February of 2017, the decline would be -12.2%.

I would also add that October was higher than November for Toronto and Durham, but not Halton, Peel, and York, but this is moot.

What this data concludes is that with 2.6% and 3.6% declines respectively in both Peel and Toronto, the average home price hasn’t changed that much since the peak of 2017. Prices in Toronto have been volatile, as you can see from the chart, but this is seasonality, and I believe that Toronto is more affected by seasonality than any other area. Why? Well, look no further than the “days on market,” as houses and condos in the 416 sell very quickly, but houses in, say, York Region, often take months to sell. There is no real “prime season” for sales outside the core.

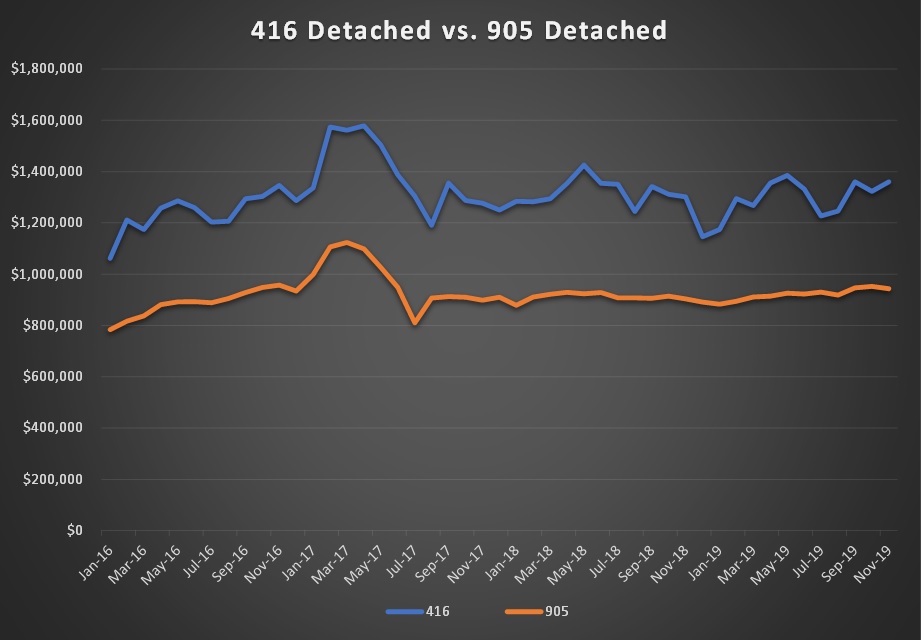

Now if we wanted to further compare between the 416 and 905 just to see what prices have done, I would recommend looking at the “holy grail” of property types, which is the detached freehold.

And we should go back another year – to the start of 2016, just to see how prices looked as we approached 2017:

Again, my initial observation would be the lack of volatility in the 905. Look how flat that orange line is from the summer of 2017 onward!

Seasonal volatility is nowhere more prevalent than with 416 freehold detached homes, and this chart proves it.

Now what have these two property types done since the peak?

416:

April, 2019: $1,578,542

November, 2019: $1,360,246

905:

April, 2019: $1,098,827

November, 2019: $943,494

416: -13.8%

905: -14.1%

Who among you saw that coming?

Having shown you this data, I would truly challenge you to find a detached home in central Toronto that’s worth less today than it was in April of 2017, and I will say that of all the data we could pull from MLS, the one figure I understand less than the rest combined is this one.

Anecdotally once again, I would suggest that there was no area with more rampant speculation in early-2017 than York Region, where sub-divisions with acres upon acres of vacant land behind them were “selling out” routinely. The run-up in prices was not a function of supply and demand, as it has been here in the central core for some time.

With a nearly 20% decline in average home prices in York Region since April of 2017, should residents be pleased to hear that prices rose 9.9% from November of 2018 to November of 2019? Or is it simply a game of waiting until prices return?

That’s the tough question for these home-owners. I met with several owners in York Region last year, all of whom referred to 2017 prices, over and over. While I remain convinced that it’s only a matter of months before Toronto recaptures those few percentage points of value that’s missing from three years prior, I have zero faith that York Region will do the same.

There’s tremendous strength in some pockets of Halton, ie. Lorne Park, Clarkson, Park Royal, and family neighbourhoods tht are close to the GO Train and QEW, and yet Halton prices remain down 9-12% on paper, depending on which month you use.

The story continues to be: depending on the specific neighbourhood, you could see strength or weakness, and prices both above or below the 2017 peak, let alone last year.

If you’re a home-owner, then my advice is to know your market! Know your specific market. Ignore catch-alls like the GTA average home price, which may or may not tell the story of what’s going on in your area.

It will be very interesting to see where prices finish by the end of 2020…

Discussion Point #2: Will anything happen with interest rates?

Ah, yes, another boring conversation about yet another topic covered ad nauseam.

But I promise, once Mom and Dad have their serious talk, then the kids can play, which is to suggest that perhaps Monday and Friday’s blog will be more entertaining if you’re not moved by stats, graphs, and percentage signs…

Let’s face it: interest rates have the single-greatest impact on the housing market of any potential influencer out there. Consumer tastes and preferences and even supply-and-demand don’t hold a candle to the impact that rates have.

So where are rates?

Where are they going?

And what impact is this going to have?

As noted in my year-end blog in 2019, rates remain low! Of course, “low” is a relative term.

When I bought my house in 2018, I took a variable rate mortgage because I’d never had one before, and because it was low. I was at 2.5%, and it was like free money! As rates increased later in 2019, I found myself on a variable rate mortgage that was above 3%. Meanwhile, my clients securing fixed rates were getting rates 20, 30, or 40 basis points lower!

I had no mortgage on my condo for the last five or six years that I was there, so all of this meandering about rates was a flashback to days prior, and suddenly I found myself thinking about things I had previously left behind.

Eventually, I decided to take a 5-year, fixed rate, and after a lot of back-and-forth with my lender, some epic bluffs, and some string-pulling, I locked into a 2.59% rate which will run until late-2024.

And in the end, I wonder, does any of this really matter?

I mean, of course! It’s money!

But does 2.59% versus 2.69% versus 2.79% really mean anything?

And so what if I was paying 3.14%. Does that impact my life?

I’m of the mindset that if you can afford to live in your home with a 2.59% rate, but can’t with a 3.14% rate, then maybe you should give home-ownership a second thought.

I know that will force both the market bulls and market bears to crack smiles, for completely different reasons, but I’m just putting this into context.

I received an email late last year from a would-be buyer who doesn’t have a penny to his name, but who wants to use the first-time home-buyer incentive to purchase a property, simply because the government is offering it. As I said in my year-end post in December, it’s not the government’s job to bring people into the housing market who can’t afford to do so on their own, although that statement opens the door to debate about CMHC and the like, so I’ll leave that for now. But I do believe that mortgage rate sensitivity has to be taken into consideration by any would-be buyer, and few even consider it. Thank goodness for the stress test. Right? Riiiiight?

We’re not going to see mortgage rates increase in 2020. That’s almost for certain.

But what if they did? How would that impact buyers?

The buyer of a $525,000, entry-level, 1-bedroom condo, with 10% down, on a 2.69%, 30-year amortization, is paying $1,950.92 per month.

That same buyer, at 3.19%, is going to pay $2,076.09.

Here we have a “game-changing” 50-basis-point difference, as some would argue, and yet the monthly payment changes only by the cost of cell phone bill. Tell me if I’m out of touch, but are people really living this close to their breaking points?

So much is made of interest rates in our market, and while I argue that there is no greater impact on the market than that which rates can make, I also think, at times, interest rate fear is overblown.

There was a terrific article in the Globe & Mail, ironically published on Christmas, about how a cut is “unlikely.”

“High Household Debt Has Bank Of Canada Hemmed In, Making Rate Cut Unlikely In 2020”

The author argues that the biggest barrier to a rate cut in the year ahead is the country’s heavy consumer debt load.

Oh, how comical!

We can’t inject life into the economy by way of a rate cut, thereby increasing economic output and enjoyment for all, because we don’t trust people to spend responsibly.

What a riot.

From the article:

There’s no question that the country’s heavy consumer debt load poses a major barrier to the central bank cutting its key rate from the current level of 1.75 per cent. The bank has said so, loudly and clearly, since late October. That’s when its governing council debated – and rejected – making a cut as “insurance” against the then-mounting risks of an escalating U.S.-China trade war and a global economic downturn.

The risks of compounding Canada’s already substantial debt problem by making borrowing even cheaper, it concluded, outweighed the benefits of giving the economy a shot of adrenaline with a cut.

The Bank of Canada has been warning for years about the potential threat of high household debts to Canada’s economic and financial stability. And it’s keenly aware that a decade of historically low interest rates has been a key catalyst in this worrisome debt buildup. As Bank of Canada deputy governor Timothy Lane cautioned in a speech in early December, in explaining the bank’s decision to hold its rate steady while most of the world’s major central banks have been cutting, “lowering rates further could make those [household] vulnerabilities worse.”

So interest rates aren’t going up in 2020, but if they did, say, a modest 25-basis-point increase, I would still argue that this means close to nothing in the context of the Toronto market.

Happy ending?

(TO BE CONTINUED…)

Marina

at 10:15 am

Happy new year!

I just had a conversation around the 2020 market with another mom yesterday, and she was sure the market will “crash” in 2020. It was “due”. She was very adamant that it would be a crash, not a correction.

I also believe I’ve had this conversation with some hopeful soul every Christmas season for the last 15 years.

Reality is, we had a correction. In 2017. Maybe we will have another. But on a 10 year horizon, I don’t see prices going down in Toronto proper. Not with the current state of infrastructure and population increase.

Mike

at 11:51 am

She is “sure” based on what fundamentals? Or is this just the same gut feeling that has kept her renting for the last decade?

Izzy Bedibida

at 1:15 pm

Or maybe she heard about some recent marriage break ups where mortgage payments ate up all their income and made Tim Horton’s the monthly date night spot.

Happened to 2 different couples friends of ex-wife.

This might be happening more often in the future. This might be a consequence of the current housing affordability crises, but not a sign of impending crash.

Appraiser

at 2:30 pm

20 / 20 Foresight:

No recession. Minimal interest rate movement – up or down. Low inventory. Higher prices.

balwinder bal

at 5:48 pm

why would you say interest rates will go up…I am thinking they are going to go down..no?

Professional Shanker

at 3:58 pm

Toronto detached is down as much as the 905, the numbers do not lie they merely point out people’s biases.

Look at Etobicoke, North York, -10% to -30% drops. I am sure examples can be found in more “Toronto proper” neighborhoods, with slightly less price declines.

Out of curiosity what % of total sales is Toronto proper, less than 5% of the market? If the market collapses, Toronto proper will as well.

condodweller

at 5:23 pm

I think what you are seeing here is that as people become more selective, desirability of a home becomes more important and the gap between the outliers widens while the average doesn’t change much. Remember that for an average price if there is a sale 30% below the mean there will be another with 30% above. During 2017 people were paying indiscriminately for any location/quality.

Professional Shanker

at 7:51 pm

Interesting theory you have, I don’t disagree anecdotally.

Professional Shanker

at 4:05 pm

My prediction is condo price gains will lag/be on par with other segments. Airbnb reg’s combined with reduced speculation in the segment will finally relent.

Rental vacancy will increase, rentals are starting to sit on the market which would have never happened over the past 3 years, are prices too high, not sure. David, what is your perspective on this?

Christopher

at 5:45 pm

I’ve noticed the same thing about rentals in the 905. It’s taking months for some places to rent unless they drop the price back down to 2018 levels.

Professional Shanker

at 7:54 pm

I know of 2 in prime 416 within an albeit a tiny sample of investor friends, this was not the case years back. Is the market changing or have they become too greedy on price, I suspect the latter but we shall see.

David Fleming

at 9:30 am

@ Professional Shanker

I noticed weakness in the rental market last fall. I had a client who’s 1-bed, 1-bath sat for a month at $2,400, and he ended up selling it. Maybe we were $100 too high, but what’s the price sensitivity here in relation to booked showings?

I had another rental listing in a 1-bed, 1-bath walk-up that didn’t get a lot of love either.

I think it might have been the time of year, however. I don’t find a lot of people want to look in December and move for January 1st, despite what people believe to the contrary. I find that people discuss life plans, New Year’s resolutions, and get pressure and questions from friends/family over the holidays, and then we see a lot of people start their searches in January.

I brought out three rental listings this week so it will be interesting to see what the activity level is like.

crazyegg

at 12:18 pm

Hi All,

Yes. I agree that the DOM for rentals is on the uptick.

One strategy I employed is using the “discounted rent” method to mitigate vacancies while also ensuring fair market rent down the road

I discounted the rent by $200 for the first 5 months to attracted interest in signing the one year lease. By the sixth month, the rental rate goes back to the normal rate (which is market rent)

Having a rental unit sit vacant for several months looking for that “elusive” tenant who is willing to pay $2200 for a studio is illogical.

Regards,

ed…

condodweller

at 12:39 pm

That is interesting David and it highlights the unrealistic expectations investors have. If the investment is not viable at record high rents at $2,200/month and the person is expecting even higher prices at $2,400 they clearly haven’t thought through the investment.

This concerns me WRT condo prices because if this person is not alone and investors start offloading units because they can’t get ever increasing rents it will put a damper on prices.

I think the psychology of rents is similar to house prices in that there is a limit what people can and are willing to pay.

Jimbo

at 8:17 pm

Most are counting on appreciation of asset to supplement the cash flow loss.

With the growth in population and that populations ability to come up with insane DP I don’t know that running to the exits upsets the condo market. Seems illogical to me but that is how it has been working the last 5 years.

condodweller

at 5:18 pm

Happy New Year!

I agree on prices that they will go up….barring the unexpected. That’s the crux of it isn’t? Prices go up until they don’t. If and when and the magnitude is anyone’s guess. Are the numbers correct for the average price graph? Shouldn’t Toronto be the highest $$? What I find interesting is that Halton seems to have peaked first.

Also, Toronto’s off the cliff shape looks an awefull lot like the yellow one except it is slowly recovering. Halton, not so much.

Re interest rates:

“Thank goodness for the stress test. Right? Riiiiight?”

I’m not one to pat myself on the back but this is kind of what I have been saying while many are calling for eliminating the stress test. I still say if anything, it should be increased to build in protection against a sudden spike that might take us backup to the 5-7% range which while historically is not high at all, it might be unimaginable to many who only remember sub 3% rates. Imagine what a 2-3% increase might do to a mortgage payment on a $500,000+ mortgage!

I do remember days with Greenspan when there was a .5% jump followed by many .25% increases for many months. Just because millenials haven’t seen it in their lifetime doesn’t mean it can’t happen again in the future.

I don’t think it will happen this year, however, it will hurt even if it happens in 10 years as the outstanding mortgage will still be high in 10 years.

balwinder bal

at 5:46 pm

what are you saying? Not right time to buy

Izzy Bedibida

at 6:06 pm

It’s always a “good time to buy”. The important thing is that the property meets your needs for the foreseeable future, the mortgage obligations can easily be met without having every penny of income spent on mortgage and housing cost to the detriment of everything else.

balwinder bal

at 8:31 pm

yep I hear you but even small townhouses are selling close to 700,000….lol….so there is no way to buy house without having every penny of income spent on mortgage…furthermore…..renting a place is also painful as rent is so high….may be time to discover another planet….lol

condodweller

at 12:51 pm

What I’m saying is that if you are borrowing your max to buy today you better be ready to handle 5-7% rates in the future. When I bought my first place my rate was around 7% IIRC and it had just come down from 12% a few years prior. If/when rates start going up prices will come down and if you can’t make your payments and are forced to sell you may find yourself owning the bank a few hundred thousand after your loss + commission.

Appraiser

at 7:08 am

December 2019 TREB data just released. Year over year results are as follows:

Sales up +17.4%

Average Price up +11.9%

HPI Benchmark up +7.3%

Active Listings down a whopping -35.2%!

Bal

at 8:07 am

Not surprised….we all knew it is coming because of interest rates…..if interest rates were about to go up….then headlines would be different….now all sellers think prices will go up…they are holding on to inventory….simple game

Chris

at 9:11 am

Remains a pretty odd market overall.

Detached prices have stayed relatively consistent since mid-2017. SALR holding steady around 30-40%.

https://torontorealestatecharts.com/toronto-detached/

Meanwhile, condos continue to do well, with prices barely pausing in the recent downturn, and while SALR is down from a high of 80% in the heady days of Spring 2017 it is still elevated at ~65%.

Chris

at 10:25 am

“Toronto housing market: lots of excitement. Resales in Dec were up 17% vs a year ago. But, last year was very weak. This Dec was unexceptional on a seas-adj’d basis – actually a bit lower than prior months (my prelim SA estimate – CREA data should be available on the 15th).

On a population-adjusted basis, sales this Dec were 17% below the long-term (2001-present) average. Sales reduction is partly due to a collapse of supply: both new listings and active listings have plunged (again, these are my prelim. estimates of seasonal adjustment).

Favourable fundamentals (strong employment situation over the past three years, most rapid population growth in a generation, and low interest rates) should be resulting in a population-adjusted sales rate that is above average, not below average. What’s the problem?”

– Will Dunning, Jan. 7, 2020

https://twitter.com/LooseCannonEcon/status/1214538779454779392

Appraiser

at 11:57 am

Problem is obvious – low inventory. More good listings = more sales transactions.

Chris

at 12:01 pm

Mr. Dunning acknowledges that as a contributory cause:

“Sales reduction is partly due to a collapse of supply”

Seems he doesn’t believe it to be the only cause.

Appraiser

at 1:27 pm

Stress test is also a contributing factor. It’s still pushing some buyers to the sidelines.

Chris

at 1:52 pm

Most likely, yes. Mr. Dunning also discusses this quite often.

Libertarian

at 9:40 am

David, congrats on the re-finance!

I tried to do the same, but of course, I wasn’t offered anything close to 2.59%. I didn’t have strings to pull as you did.

I am very envious.

Appraiser

at 9:53 am

REAL ESTATE NEWS: Toronto Star, Jan. 7, 2020.

“Toronto home prices likely to be hot again in 2020 after 4 per cent increase last year”

https://www.thestar.com/business/real_estate/2020/01/07/toronto-home-prices-up-4-in-2019-and-signs-point-to-a-hotter-market-ahead.html

Chris

at 10:08 am

Prediction courtesy of TREB.

Their 2019 prediction turned out to be quite accurate: “This demand/supply relationship points to price growth in the mid single digits, with the average selling price reaching $820,000” – average selling price for 2019 came in at $819,319.

Their 2018 prediction was less so: “The forecast range for the overall average selling price is between $800,000 and $850,000.” – average selling price for 2018 was $787,300.

Appraiser

at 12:00 pm

Always behind the curve.

Chris

at 12:02 pm

In 2018, yes, agreed, TREB definitely were. In 2019, they did better. We’ll see how their 2020 call turns out!

condodweller

at 12:57 pm

I think he was referring to you 🙂 What a way to start off the new year.

Chris

at 1:01 pm

Oh I know, I just chose to give him the benefit of the doubt. Thus I responded while working under the assumption that he was conducting himself as a decent person, rather than trolling yet again.

Appraiser

at 10:16 am

Attention name change effective immediately: The Toronto Real Estate Board is now the

The Toronto Regional Real Estate Board.

(or TRREB ) ?

Chris

at 10:22 am

Old news.

https://twitter.com/areacode416/status/1205654212459282433

Appraiser

at 12:00 pm

Too funny.

Former905er

at 12:25 pm

“There’s tremendous strength in some pockets of Halton, ie. Lorne Park, Clarkson, Park Royal”

Those areas are all actually in Mississauga/Peel 🙂

Mr. Anon

at 12:02 pm

https://www.osc.gov.on.ca/en/Proceedings_soa_20150813_mortgage-company.htm

https://www.realtor.ca/real-estate/21441696/3-bedroom-single-family-house-2423-bridge-rd-oakville-bronte-west

RECO won’t do a thing about it either.

Bailti FR

at 4:04 am

Nice, Si vous êtes un étudiant à la recherche de la location ou de la colocation idéale, sachez que vous vous trouvez au bon endroit. Vous pourrez être mis en relation avec des personnes ayant les mêmes affinités que vous pour que la collocation se passe comme sur des roulettes. Ouvrez-vous à une multitude de possibilités et dénichez aisément votre futur logement grâce à cette solution aussi simple qu’efficace. “https://www.bailti.fr/”

Landmark Property Buyers

at 4:26 am

Wow. Our mission is to relieve people from the burden of property ownership. If you’re looking for fast cash in exchange for your unwanted real estate, submit your property information to us today! “https://www.landmarkbuyers.com/”

uspercargo

at 9:32 am

Buying internet media, as an example impressions, emails distributed, sponsorships, and so on. Internet marketing is more affordable than printedads.