Fifteen offers, wow!

Who says the market is slow, right?

In actual fact, and this is a topic for another day, the market has come back hard over the last three weeks. Agents are seeing it and talking about it, buyers are feeling it, and some sellers are making moves where as they wouldn’t have six weeks ago.

Today’s blog will highlight an example of how and why the market looks to have made a comeback, specifically, sale price that even the buyer and the buyer agent admitted made little sense.

But it’s the experience of the listing, the sale process, and the interaction with buyer agents that is actually the topic of today’s blog.

Fair warning: when I write these posts, some readers don’t like it! They feel I’m being mean, or that I’m being unfair, or they agree with what I’m saying but feel as though I’m complaining whereas I should be happy that the incompetence of other agents allows me to elevate my own game.

The actual point of today’s blog is to help buyers.

Because every one of the agents that I’m going to describe in today’s post is representing a buyer in the (potential) purchase of a home.

The truth is: these buyers have no idea that their agents are making mistakes. The agents themselves can learn from this too, as I know I made at least one new friend who is a new reader, and who will read about herself in today’s blog.

I was raised with tough love both in my childhood as well as when I cut my teeth in the real estate industry nineteen years ago.

I have a lot of sayings and adages that I hold near and dear:

“Never make the same mistake twice.”

“Learn from your mistakes.”

“The best way to learn is by doing.”

“Failure provides a learning experience that success never will.”

Where one might see negativity, I see positivity. I see an opportunity to learn.

So based on my experience with the fifteen agents who submitted offers

Let me set the scene:

The property was listed for $899,900 and it was, by most accounts “worth” somewhere around $1,000,000.

But what’s it really worth?

And has the market changed?

My clients own a lot of real estate and they trust me emphatically. They said that they were flying to Florida at 7:15pm and that all they needed was for me to send them a DocuSign by the time they were “wheels up.” They didn’t need or want to be involved in the process; just tell them where and when to sign.

I held offers at 6:00pm.

I work quickly.

And I’m not one of those agents that loves the feeling and the power, and keeps the process going for hours on end.

I emailed all the agents that showed the property with VERY specific instructions, outlining that offers would be reviewed at 6:00pm sharp and that agents were to register their offer by no later than 5:00pm, “To ensure all agents presenting an offer at 6:00pm were informed as to the number of competing offers.”

By 5:00pm, only three offers were registered.

Go figure.

But that was merely a sign of things to come this evening, so let me tell the stories in a way that provides for learning.

Here are the lessons that I believe could have been learned last night…

–

1) Introduce yourself.

While this might not be a “face-to-face” business anymore, it’s still a business where people interact and transact.

Some may long for a time when sales are automated, but for now, listing agents and buyer agents are still human beings with faces and names.

Since 10% of the agents do 90% of the business, more often than not, I already know the listing agent. But whether I do or don’t, if I have an interested buyer, I’ll give the listing agent a call.

On the day of offers, at 8:35am as I was picking up my morning offer, an agent called me.

“My name is Desiree,” she said, “And I’m just calling you so you remember my name.”

“Desiree,” she said again. “I’m going to be submitting an offer on your property tonight, and I know you’re going to have a lot of calls. Please save your number in my phone. It’s Desiree.”

Well, geez, Desiree, you had me at “hello.”

I did save Desiree’s number in my phone, and while Desiree didn’t have the winning bid that night, or anything close to it, I recognized her name when she submitted her offer, I recognized her name when she called for an update, and had she been in the running, I surely would have worked with her.

–

2) Introduce yourself at the least, but above all, don’t be anonymous.

Further to our first point, some people not only fail to introduce themselves, but they fail to communicate who they are at all.

By 6:30pm, I had received about thirteen offers.

An email came into my inbox from a sender named, “Hotmail Account.”

I hate that. Not just in real estate but in general. Some people will put their name as “T” or “T S” instead of “Tony Smith,” and it’s their prerogative, but I find it odd.

In any event, “Hotmail Account” sent me an email with an attachment. The attachment was called “Scan108494184.pdf.”

Why not rename that file, “123 Jones Street – Offer 2023.2.20?”

Nah, that’s too logical.

I opened the file and sure enough, it was an offer.

But I had no clue who sent me this offer. I had to scroll to the very bottom in the “Confirmation of Cooperation” to find the person’s name.

I then looked up their name and found they did not register an offer.

Go figure.

It’s 6:30pm. Offers were due at 6:00pm. Offer registration was 5:00pm. And now I’m in receipt of an offer from a person who I had never spoken to, who didn’t register, who had no name in their email, no name in their email signature, and I actually had to Google this person to find a phone number, which I was not able to.

Is this real life, or is this just fantasy?

–

3) Know your market.

I’m genuinely asking here, without sarcasm: if an agent calls me and says, “I don’t work in Toronto, so I was hoping you could help me price this property,” would you expect me to do so?

Some of you want to think the world is a good place, so you’re hoping I would help this agent.

Some of you will say, “David, you have a fiduciary duty to your client, so helping this agent to price the property is helping your client.”

Except that maybe it’s not.

Maybe this agent was going to value the property way higher than it’s worth, so my “helping them” might cost my seller money.

Maybe this agent was going to value the property way lower than it’s worth, so my truthful assessment of value might cause them to back off and not submit at all.

Speculate all you want, but there’s a difference between calling the listing agent and saying, “Hey, I know you probably can’t answer this, but do you think this is headed north of $1,000,000?” and that of what I received last week.

One agent called me and said, “I’m going to send you my evaluation to look over.”

I asked, “Huh?”

He said, “I’m from Niagara Falls and I don’t know this market at all. I put together an evaluation but I need you to look at it and tell me if I’m on the right track or not.”

Folks, I would be absolutely mortified if I did this. There’s just no way to explain this.

But I had agents from Niagara Falls, Hamilton, Barrie, Huntsville, and even one from Sarnia all calling me and saying, “I don’t know this market, can you help?”

One agent took a photo of his computer, which was showing his “comparable” properties, and emailed it to me asking if these were houses I would compare the subject property to.

Caught in a landslide, no escape from reality.

–

4) Understand who is in control; the buyer or the seller.

This will be a tough one for those buyers who say, “I’m gonna do what I’m gonna do, and nobody is going to tell me otherwise.”

It’s a free country. But if you expect to be successful in a 15-offer process, you’re going to have to play ball with the sell-side.

Every agent who called me to ask, “How are you going to handle this process tonight?” was told that offers were at 6:00pm, a decision would be made by 6:30pm, and an offer would be accepted by 7:00pm. But they were also told, “Bring your absolute best offer.”

Bring your absolute best offer.

That’s different from: bring the list price and expect to be given a dozen opportunities to improve, incrementally, all night, as you see fit.

Right?

Look, I get it, I get it! Some people don’t like the process. Some people won’t be strong-armed. Some people are going to do what’s “best for them.”

But every real estate scenario is different!

Case in point:

Scenario A: The subject property has been on the market for 87 days without an offer.

Scenario B: The subject property is under-listed with an “offer night” and there are fifteen offers.

An agent called me midday to talk shop and said, “I’m just letting you know that my clients are going to present a starting offer and then work upwards from there.”

I said to the agent, “I’m expecting eight or ten offers tonight, so we’re going to encourage buyers to bring their best and we’ll make a decision right then and there.”

She said, “Yeah, but I’m telling you that we’re not going to work like that. My buyers are going to start small and slow and work away.”

I replied, “You and the buyers can do as you please. But I’m telling you that the seller is on a timeline, they are seasoned sellers, and they don’t want to drag this out. They will accept the highest offer presented, and you will not be given an opportunity to improve.”

She sighed and said, “You’re not listening. I’m trying to explain to you how this is going to work. My buyers are going to make a STARTING OFFER.”

I wasn’t rude.

I didn’t tell her, “You’re not listening,” or “I’m explaining to you how this is going to work because it’s my listing.”

I simply said “Okay,” and let her crawl into a hole, pull dirt down, and bury herself.

I had several agents take this approach. It was mind-numbing.

As an agent, you have to understand who has the leverage in every situation: the buyer or the seller.

If I have a listing that’s been sitting on the market for thirty days, I expect to make concessions. I expect to be submissive. I expect to roll out the red carpet.

But If I’m presenting an offer in competition, I can’t fathom calling the listing agent and saying, “Here’s what we are doing tonight, so eat it!”

That’s the path that three or four agents took, but in the end, they all wanted to improve their offers once they knew that they had lost…

–

6) Put your best foot forward. Especially when you’re told to put your best foot forward.

Here’s a rhetorical question: if you made an offer on a property and you knew that you had the highest offer, would you want the seller to accept your offer, or would you want the seller to allow the six people behind you to improve their offers and leapfrog you?

It’s not a trick. It’s rhetorical. Everybody would want the seller to accept their offer.

But if you had the third-highest offer or the fourth-highest offer, would you want a chance to improve?

There’s an assumption from every buyer agent who ever made an offer that goes, “If I’m the highest offer, I want you to accept it. If I’m not the highest offer, I want a chance to improve.”

When I decided to proceed with the highest two offers, I started emailing the agents who were at the bottom and telling them that we were working with another offer.

Every time I clicked “submit” on an email, ten seconds later, my phone would ring, and it was that agent, calling to find out why he or she didn’t “win.”

The agents didn’t win because they were all low by $100,000, $150,000, or $180,000.

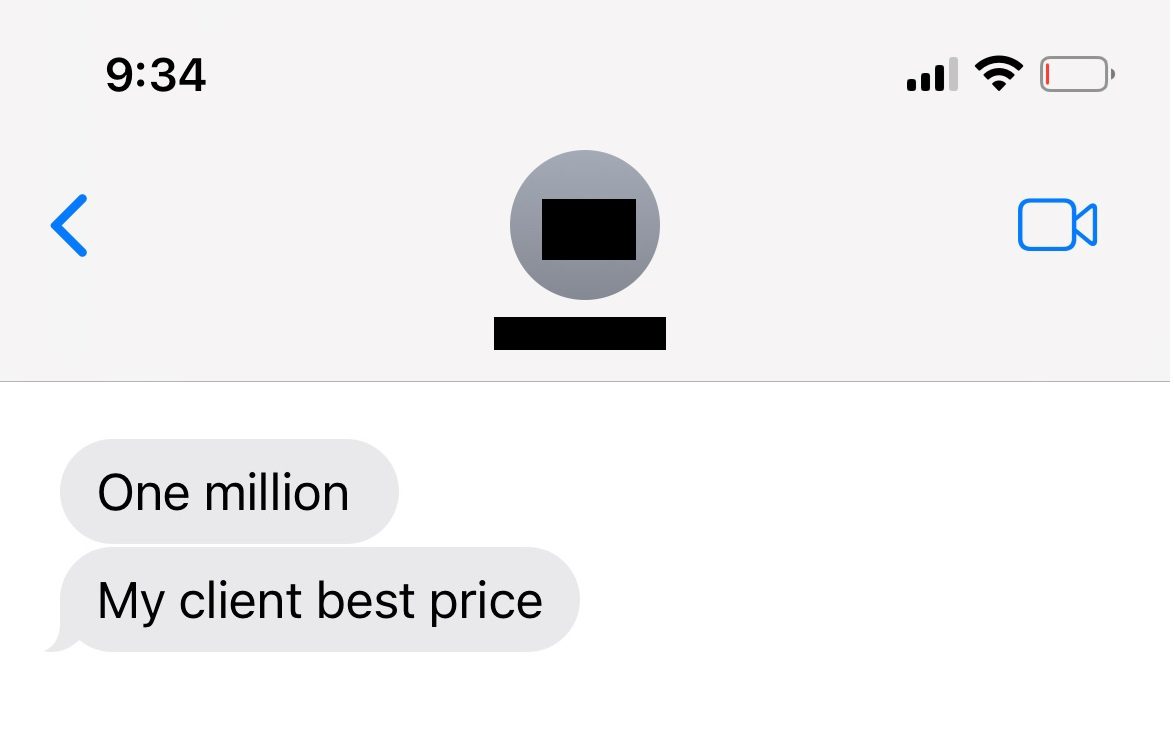

But then they would follow up with text messages, like this one:

First of all, this was an agent who offered $950,000.

If you wanted to bid $1,000,000, then 6:00pm was probably the time to do it.

But more importantly, this doesn’t constitute a legal offer.

You can’t just text message numbers. It doesn’t work that way.

Here’s another:

This agent offered $970,000.

Oh, I suppose I should mention: the property sold for $1,108,000. That’s important at this juncture…

–

7) Don’t shoot yourself in the foot and then attempt a marathon.

Once again, for the umpteenth time, “You do you, bro.”

If you want to offer $100,000 under the list price when there are sixty-six offers, go for it.

But you can’t have any expectation of success, can you?

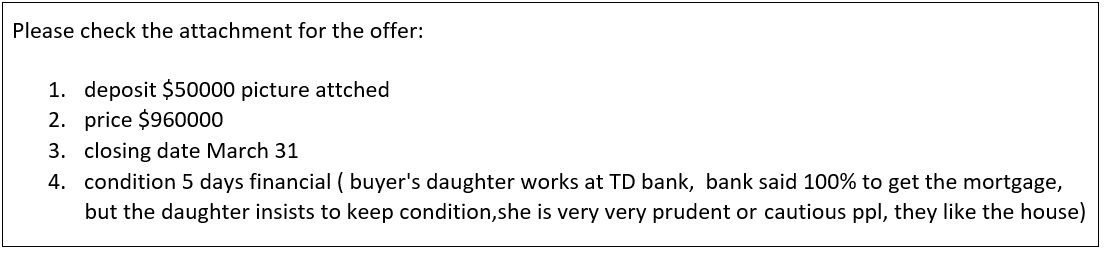

I wanted to call this point, “You can’t have it both ways,” because the following picture explains why:

This makes no sense.

There are fifteen offers on the property.

It’s competitive.

You have, apparently, 100% certainty of obtaining a mortgage and yet you’ve included a condition on financing which is going to ensure you have no chance on offer ngiht.

It’s like this one:

We included a Carson Dunlop pre-inspection, as we always do.

This agent says, “We don’t see any problems” and that the client is “financially sound” but included two conditions, one on inspection and the other on financing, “for ease of mind of buyers.”

As I said, you do you, but you can’t shoot yourself before you’ve even got into the starter’s blocks.

–

8) Have your clients prepared.

Offers were due at 6:00pm and I started reviewing offers by 5:30pm when the first one was submitted.

One offer came in that was very high and I figured that if it wasn’t the best, it would be in the top two. So I called that agent and said, “Do you have the deposit cheque with you, or do your clients have it?” He said that his clients had it, and I told him, “You might want to have that in your possession. Your offer looks good.”

But more importantly, I told him that there were two mistakes in the offer that needed to be corrected and that if we decided to work with his clients’ offer, we would need that offer resubmitted with the mistakes corrected.

That was at 6:15pm. I know this because I log all my communications in these situations.

There was another offer that was close, but I was inclined to work with the first one as it was better in all respects. I just needed that agent to resubmit.

Time kept ticking and I knew I had a 7:00pm deadline.

I was shocked that this agent hadn’t resubmitted. When making an offer in competition, you should literally be sitting in front of your computer. Sure, life happens, but if you’re the agent that wants to go curling from 6-7pm when offers are being reviewed, you have only yourself to blame if you’re passed over.

In this case, it was one of the buyers who went missing. Again, life happens, but it’s the buyer agent’s job to prepare the client for the process, and I told every single agent that I was going to review at 6:00pm, have a decision by 6:30pm, and have a signature by 7:00pm, so absolutely nobody could claim they were caught off guard.

By 6:45pm, I called the agent and again he said, “I’m still trying to get ahold of my client.”

So I then called the agent with the second highest offer and said, “You’re my backup plan.”

She said, “What do you need?”

I told her, “This has to be fair so I’m not gift-wrapping this to you, but if you can improve your offer past the one I have in my hands, it’s yours.”

And she did exactly that.

She improved her offer and beat the first offer by $13,000, but moved her closing date up by six weeks so that my clients could now close in a month. The other offer had a ninety-day closing, and that agent said it was because her clients had a 1-bedroom condo to sell.

At 7:00pm, the agent with the first offer still hadn’t resubmitted, nor communicated anything of any sort to me.

We accepted the second offer at 7:15pm as my clients were “number two for takeoff,” sitting on the runway at Pearson. For what it’s worth, they had WiFi on the plane just in case, but they made it clear that was a disaster plan and that they wanted this property sold by the time they took off.

I sent an executed copy to the agent who provided this wonderfully-revised offer, and the property was sold.

Then I called the first agent and told him we had accepted another offer.

He was livid.

I explained that I was very up front with the process and that I told him from the very beginning, “We will have this property sold by 7:00pm. I even waited an extra fifteen minutes.”

He hung up on me.

–

9) Reside on planet earth.

I was home at 7:55pm when I got an email.

It was an offer.

It was from somebody who did, to their credit, register an offer.

But it was 7:55pm.

Offers were due at 6:00pm.

And the offer was quite poor, in case you hadn’t guessed.

I emailed back right away and said, “Thank you for your offer, however, offers were reviewed at 6:00pm as per the instructions sent this morning through BrokerBay and the property was sold at 7:15pm.”

I never heard anything back.

Oh, the poor buyer clients…

–

Well, folks, tell me you like my tough love or tell me you love my tough love!

But don’t tell me any of the above was unfair.

Or, do. Even though you’d be wrong. 🙂

Whether the market is up, down, or sideways, it’s no easy task to sell real estate in Toronto.

Buyer agents would be wise to accept the tough love and learn lessons as a result.

I wonder if any of them will?

Peter

at 8:33 am

I love the subtle Queen reference this morning.

Marina

at 10:54 am

Part of the problem is that everyone is an “expert” in real estate these days. Their dad got a great deal on a house 30 year ago, so he’s totally going to walk them through the process and score them a great deal. Or they know everyone says one thing but mean another. And you can never convince them otherwise.

The thing is, some buyers are not actually ready to buy. They are not willing to put in an unconditional offer, or offer over asking, or get into a bidding war. So they are just not there yet, and that’s fine. But a lady at work has put in over twenty offers in the last six months, and still has not bought a house, and I’ll let you guess why. She thinks the market is nuts. Some other colleagues think she’s not very smart. I just think she doesn’t really want to buy. She’s not ready, so she keeps giving herself an out.

Back when we bought our house everyone was telling us we were nuts. Prices were going to fall. We would regret buying an older semi and should just rent a condo. On and on. Meanwhile our house has more than doubled and is almost paid off. But I’m sure those same people would love to tell me how I could have gotten a better deal, while they still rent.

Nobody

at 4:08 pm

David, the biggest reason buyers don’t trust sellers’ agents is because they lie all the time about the process, final and absolute best offers, number of offers, etc etc etc.

There are just very, very few situations, even from an agent like you, where the process is really that constrained. Even then you did work with the top 2, rather than just being a fully final sealed bid auction of one round.

Very hard for even a sophisticated agent to realize that the process would actually happen like you claimed. In the current market and in the last 15 years, the agents who expected multiple rounds and treated this sale like all the others have been proven right 99.99% of the time.

Ace Goodheart

at 11:36 am

RE:

“This makes no sense.

There are fifteen offers on the property.

It’s competitive.

You have, apparently, 100% certainty of obtaining a mortgage and yet you’ve included a condition on financing which is going to ensure you have no chance on offer night”

I always wondered about this, because I refused to do it myself when purchasing.

I understand the process of pre approval and that you get a letter from a bank saying you have a certain number you can go up to, for purchasing. I also understand that this letter does not obligate a bank to actually advance you these funds, and that you require, following an accepted offer to purchase, an appraisal and also a firm commitment from your bank (if you want to use mortgage financing, which apparently every one does).

So any seller who is accepting these firm offers, is aware (or should be) that the buyer does NOT have firm approval from their bank, that they might NOT be able to close, and that the process for dealing with a failure to close involves a court case, lawyers and a whole truck load of money paid out in legal fees, with full recovery being years away (if it happens at all, often the failed purchaser will declare bankruptcy or find another way to disappear and not pay the bills).

Would a seller not want firm financing before they sign off on an accepted offer?

For me, as I had said in previous comments, I actually did have the money, in a number of direct investing accounts, in securities holdings. The process for obtaining said money is of course complicated and involves finding a buyer for your securities at market price, and then waiting about three days for the transaction hold back period, and then moving a large sum of money from one account to another.

If a person does not want to actually sell their holdings (because they are making 6% on the securities, and they can get a mortgage for 1.2% so it is free money) then you put a “conditional on financing” clause into the offer, to save yourself the trouble should the bank bail out or the appraisal come up short.

And you are refused. Beat out by people who I refer to as “cream puffs” because they are bidding money they do not have, and relying on financing that they have not actually received a firm approval for.

These bidders are going to do one of two things, upon acceptance of their offer:

1. Figure out a way to borrow the money or…

2. If they cannot, then try to convince the seller to accept a lower price (we see this now happening a lot with deals inked in February of 2022 that close in 2023).

So the seller is really just accepting “cream puff bids only”. Unless they are actually verifying that the purchaser has the money (or can borrow it).

I was asking my agent “do you want me to just email you a black lined version (identifying information removed) statement of my investments? So the seller can see that I am not a cream puff buyer. I have the cash, I just would prefer to finance as I get a lower interest rate than I currently earn on my portfolio”.

I got no takers. I ended up buying a house that no one wanted (for the usual Toronto reasons, basement moisture reading was too high – because it has a stone foundation, no weeping bed and is 143 years old, so what do you expect?) and it looked like crap (but wasn’t, actually a very good house).

I don’t understand the process of basically preferring cream puff style bids over people who are more responsible with financial matters.

Bryan

at 12:58 pm

I am asking this out of a genuine curiosity rather than to be obtuse, but what interest do you think your investments are to a seller if you are not prepared to cash them to buy their property?

I would assume that the reason you are making an offer conditional on financing is because, one, there exists a chance you will not secure financing (bad appraisal or whatever) and two, if you did not secure financing you would not want to purchase the property. In essence then, regardless of investments, the condition passes the risk of you not securing financing on to the seller.

The other thing I would ask is how might a seller distinguish between someone who is paying cash (or perhaps someone looking for financing but would pay cash if it fell through… or someone who has a bunch of other properties they would leverage to obtain financing) and a “cream puff” style bid? Conversely, how do they know that you aren’t someone who is making an offer conditional on financing because you only make $35k a year and don’t think the bank will approve you?

The number of instances where a “cream puff” fails to close is very very small (I believe David did a blog about it a little while ago?) and the number of offers conditional on financing that never turn into real deals is much much higher. Individual risk tolerance plays a critical role (big downside for the seller in the <1% of the time the cream puff doesn't close), but the expected value of going with the non-conditional offer is almost certainly higher than going with the conditional one.

Ace Goodheart

at 1:41 pm

My issue was timing.

At the time of purchase, banks were running “credit cues” which were quite long. When you put in a request for funding, it could be weeks before you heard back.

Offers have closing dates, and they cannot be extended without consent of both parties.

So I was quite clear that I wished to buy the property, could do so in cash, however I was putting the financing condition in, so that I could obtain the financing I wanted. I was also clear that I intended to purchase anyway, even if I could not get financing that I liked, however in that case I may be a bit long on my closing date, as I had to dig into financing more and try to get the loan I wanted to get. I made my expectations and means crystal clear to all involved. However, sellers would not accept offers conditional on financing.

During the two and a half year process that it took to find and get an accepted offer on a house, more than one of those sellers had their Agent contact me to advise that the top bidder had flaked out, and they were wondering if I wanted to revive my offer. Surprisingly enough, they STILL wanted me to do it unconditional on financing.

I would disagree that offers conditional on financing fall through more regularly than firm offers.

My concern has always been, that the offering process not only allows, but actually ENCOURAGES “cream puff” bidding. I would think that a buyer would need to have firm financing in place, before making an offer. But this is not the case. You can offer on a property with no financing in place at all, and provided you have a small deposit available, you can be the high bidder.

Ed

at 4:14 pm

Ace Goodheart

February 23, 2023 at 1:41 pm

My issue was timing.

At the time of purchase, banks were running “credit cues” which were quite long. When you put in a request for funding, it could be weeks before you heard back.

////////////////

Guess you never heard of a mortgage broker.

Different David

at 7:44 am

I have to be honest – if I were a seller, I don’t care what your investment accounts are. If you have a condition that forces me to relist my property and show weakness, I’m going for a 100% sold offer that I can work with later on (if it comes to that).

Your desire to squeeze out a few extra basis points of profit is not high on my list of concerns.

As David has written on many times, an unconditional offer will always trump one with conditions in a multiple offer scenario. Go cream puffs!

Ace Goodheart

at 7:59 am

True…until the buyer can’t close.

Then you want to talk to the more financially responsible people who put conditions in their offers…

Nobody

at 3:53 pm

If you’re going to close anyway regardless of financing, why do you need a condition?

Thw only reason is because you would want to amend the offer and want to be in a position where the seller is more likely to accept a gaircut rather than go through the process.

You either accept where the matket is and transact or you don’t. Not wanting to engage is a fine decision – FTX seemed insane to me but some 28 year old in a tshirt was worth 10 Billion 4 years agter starting his company. Now he’s on bail, just got more bank fraud charges, and is VERY LIKELY to do 30+ years in federal prison with his ex girlfriend co-operating with the US government against him. It’s also very likely that his brother and his parents go to prison too.

Lots of people told me I was an idiot for not getting in on bitcoin and blockchain and I was a bootlicker for caring about things like money laundering, wire fraud and securities law.

Don’t try to engage in an irrationality exuberant market and get angry that you won’t get treated like you’re in a buyer’s market. A hotel with 95% vacancy rate will give you an amazing discount if you talk to a manager. When there’s 98% occupancy in every hotel within 80k. Of Union Station and the Hilton wants $1200 for a standard one king don’t try to get the manager to give you a room for 99 bucks.

Bryan

at 4:29 pm

Why didn’t you just make the closing date conditional then? I have not personally seen it done, but it is definitely legally possible to put in a clause that says “closing is 30 days conditional on the buyer getting financing in the next 7 days. If not the fail to get financing, closing is 60 days”. To make the whole deal contingent on financing makes a buyer think you simply want to eliminate all the other offers from the conversation and then, when your financing “falls through”, change your mind on the price without the hypothetical legal repercussions that a firm “cream puff” would have while putting the seller in a situation where they need to either re-list, or take whatever you decide to offer them. If I am a seller and all I have is your word that your financing condition is you being “responsible on financial matters”, rather than setting me up for a haircut, I wouldn’t trust you…. because I have no reason to. Now if it was just the closing date that was conditional, that is another matter.

The conditional vs non conditional “offer falling through rate” would be an interesting thing to look at. I wonder if David has that categorized in one of his spreadsheets (my guess is yes). My guess on what the actual rates are would be ~10% for offers conditional on financing and <1% on firm offers over the last few years. Perhaps the more recent market has that <1% number a bit higher.

Ace Goodheart

at 10:02 pm

Again, I would have to disagree with you.

I have sold houses as well as bought them. I deliberately underpriced houses to create bidding wars.

But on offer night, I would not necessarily take the highest bid. Or the bid with “no conditions”.

I took the bid that I thought could close.

In one case, the high bid was a young couple who had put together financing which included loans from family. I refused to sell to them. They seemed shaky financially. I took a bid 20k under what they offered, because the bidder was a divorced lawyer, I knew her firm, I checked and confirmed she was a partner and I knew she had money. She actually sent the deposit cheque two days after I accepted her offer (the other folks had a certified cheque with them).

I used to drive my Agent nuts doing this but I just did not want to sell to a cream puff.

I also avoided people I thought might sue me if it turned out there was something wrong with the house. I was literally doing face book back ground checks on bidders while my agent was scratching his head like “what are you doing?”

I was like “read this face book post, these people are assholes, I’m not selling to them no matter what they bid”

So, yeah, been there, done that.

Most important thing for me was always “can they close?”

Ethan

at 12:19 pm

I too am somewhat confused by your assertion. You want to buy a property, you prefer to finance it, but you have 100% certainty you have liquid assets to pay in cash if your financing doesn’t come through?

You are the epitome of a buyer who should be making offers *without* a financing condition. By your own admission, there is zero risk in your ability to go through with the deal; so why add a condition?

Ace Goodheart

at 1:37 pm

I didn’t feel like selling a bunch of stocks that I kind of liked.

It is also very difficult to liquidate a large securities portfolio. There are a lot of brokerage fees involved and you have to find buyers for securities at prices you are willing to sell at.

I just didn’t want to get pushed into that situation.

I also saw it as a financial hit on my side of things. If I had to give up, say a few 100K of securities, to pay out the difference on a house that I bid up to $2 mil and that the bank appraised at 1.8 mil, then I have 200K that I have lost 6% interest or more on, and also I did not get that 200K at a 1.2% rate.

It represented a financial hit for me.

I know most people don’t see it that way, but that might be because most people didn’t have the money anyway and were just going to borrow it. When it is your money, you are much more careful than when it is just money being borrowed from a bank.

I saw the whole situation as an unreasonable risk for me having to take a financial hit that I did not want to take, so that I could win a bidding war against folks I referred to as “cream puffs” who had very little money and were just running on a dream and a prayer, hoping a bank would actually advance them the funds. I saw it as very careless.

When I have worked in big business and been part of the purchasing process for large expensive assets, I know that we never made any sort of firm offer (unless you are Elon Musk, I guess, and buying twitter – his lawyers must hate him) without financing in place. You made your offer conditional and then firmed it up as the financing process took place.

At any rate, we all saw what happened in March-onwards of 2022, talk to any real estate lawyer (I know a bunch of them) and they will tell you that their “problem files” exploded in volume after the end of February 2022.

Geoff

at 9:55 pm

Ok wait, it’s not that buyers won’t accept an offer that’s conditional on financing. If you’re the only offer, they may well do that. But given a choice of offers, it would be hard to select that offer. Especially if one is selling to buy another, and they need the funds from the sale (cough, cough) selling conditionally can introduce a level of uncertainty that no seller wants to experience.

Steve

at 12:28 pm

Let’s face it the reason so many people don’t do their best offer on the first round even when explicitly told to is that there are plenty of selling agents who will say that and then send them back to improve anyway.

I mean even here in the end didn’t you do exactly that with what became the winning offer?

Jennifer

at 1:19 pm

Exactly. Basically it’s a “come in at your second best but close to your best” offer. Even if the first offer is over $100,000 they still come back to the top 2-3 to improve and squeeze more out of the top bidder. How often is it a one shot process?

JF007

at 12:55 pm

When we decided to move out of our North York Condo to the burbs we were working with a “part-time” realtor friend of ours looking for his first sale..we absolutely loved a 42×135 detached with great backyard potential, we were unsuccessful but then the house came back on the market as the sale fell through but then our friend did the worst thing possible instead of submitting an offer kept conversing with seller agent on what they expected out of it, and the seller agent turned around and sold it to his own buyer just a 1000 over the list price …we were so livid..the friend did redeem himself though by getting us our current house about a month or so later that too almost 30K below what we were ready to pay using the same tactics..difference this time was that one the property had sat on the mkt for 3 months through 3 relists and reductions and this time we had submitted an actual offer 😀 . Even though there was another offer in play we gave a 30 day closing per seller request and resigned right away post some negotiations.

f00kie

at 9:26 pm

I wonder what kind of people need to get rid of a $1M investment specifically on this particular day and by this particular time.

QuietBard

at 10:54 am

Could be lots of reasons. Keep in mind they probably bought the property years ago

1)They have another business opportunity they want to take advantage of

2)They may realize the value of the property is at its peak.

3)Reducing real estate exposure/ don’t want to deal with this specific property anymore

4)Want to have fun spending their wealth

5) Their kids are in a bind and need a few hundred thousand to close…..

Nobody

at 4:03 pm

I didn’t see that they “had” to get it done, just that they wanted to. They didn’t want to delay their flight, didn’t want to deal with it after midnight or the next morning – just as the buyers wouldn’t want that – and didn’t want to move their offer night.

Think of it like how much you care about the sale of 1000 shares in BCE vs selling the family convenience store/restaurant/medical device manufacturer. An investor with many properties in their portfolio selling one of them is not going to care as much about the process/want to be involved as much/ir try to price to absolute perfection. When you’re selling your family house or a cottage you’ve owned for 4+ decades you’ve going to be deeply involved and want (and probably need) to get every possible dollar.

Vancouver Keith

at 3:54 pm

It’s amazing that after the interest rate increases we saw last year, that the market is as strong as you have communicated. It’s proof that there’s still a lot of demand out there. The fact that you can dictate the buying process in this way in order to get the best result for your client would suggest that we are still a long way from any kind of crash scenario. Your tough love is a reflection of the market realities, sadly with the extreme Pareto principle at work in the real estate business you will always be dealing with people who have limited experience.

Is it possible for buying agents to work with a local agent from the same real estate company in order to get advice on comps and valuation, or does collaboration fall apart at the prospect of fair compensation for that advice.

Sirgruper

at 12:11 am

Always like the tales from the trenches stories. David, Just wondering, if an offer came in clean at $960,000 with a $200,000 deposit and a quick closing, what would have you advised your clients to do?

David Fleming

at 6:12 pm

@ Sigruper

Sorry, I think I must have confused the readers here.

The offers we had in hand over $1,100,000 were both unconditional. One had a May closing the other had a March closing, and because the first offer dragged their heels, we went with the March-people who came up in price.

But to answer the other readers at the same time – there were so many offers between $940,000 – $970,000 that they were all moot. Sure, somebody texted, “My buyer will go to $1M” but they were still $120K short. My point was that these folks should have come in at their $1M price. Yes, agents always ask buyers to improve, but no, that doesn’t mean they should leave anything on the table. Nobody ever wins in these situations by presenting a “starting offer” and then working upwards. Ever. It’s always the ones hot out of the gate, and in this case, I had two.

Sirgruper

at 6:56 pm

Thanks. My bad (I thought they were conditional) and good to know to lead strong.

Alex

at 12:50 pm

That’s how it should be, up front, firm and professional. I would have loved to seen the agent who “explained” to you how it’s going to work when they found out they couldn’t improve their offer! Well done sir.