There’s a saying in sports: “Sometimes, the best trade is the one you never made.”

I often look back on an investment I almost made in the city of Waterloo, Ontario in 2005 and ask myself, “What if I had bought that property?”

Waterloo, Ontario is a beautiful place.

Kitchener, Ontario, is a hole.

Ask anybody from the area, “Where are you from?” And they’ll almost certainly say, “Waterloo.”

When I was attending McMaster University, my best friend was born and raised “in the area,” but instead of telling people that he was from Hamilton, he would always say, “I’m from Dundas.”

Nobody wanted to admit that they were from Hamilton, just like most people from Kitchener-Waterloo say they’re from Waterloo, or at the very least, “K-W.”

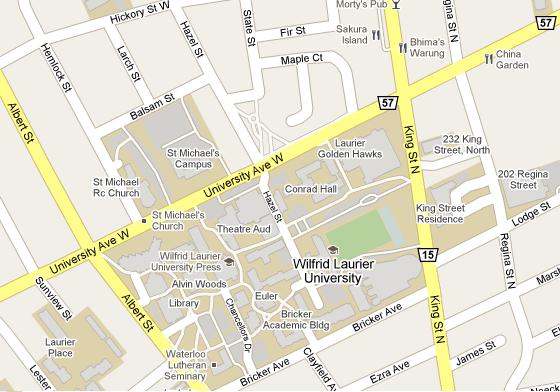

Although I went to McMaster University, I spent a lot of time up at Laurier since my girlfriend, my brother, and some of my close friends all attended the school.

I got to know the neighbourhoods that surround campus extremely well, and once I was finished school and working in real estate in Toronto, I realized how unique the area was.

Where I went to school at McMaster, it felt like the campus was a fortress and was protected on all sides. All the residences that students lived in were across a major road (Main Street) or down Sterling Avenue.

Wilfred Laurier, on the other hand, was incredibly small by comparison and you could literally jump from your house on Bricker Avenue right onto campus. Ezra, Albert, Clayfield – all the surrounding streets were less than a minute walk from campus and you could leave your house and be inside the classroom in three minutes.

Every one of these houses on streets like Ezra were home to students, and it formed a bit of a ghetto. But there were never any vacancies, and houses would be spoken for in May for the next term in September.

Back home in Toronto, I was looking for an investment property and trying evaluating six major criteria:

1) Capitalization rate

2) Number of units/size of property

3) Vacancy potential

4) Location

5) Demographic of tenants

6) Condition of property

It goes without saying that you want location to be A+. I don’t really care what the cap rate is when the property happens to be out by the airport; it’s just not a viable option. But these criteria all tie into eachother, and I wanted something that would have low vacancy and attract decent tenants because of the location.

The issue I had was that the cap rates in Toronto were far too low no matter where I looked.

I heard some investors refer to “good” cap rates when they were as low as 5%!

I understood that I wasn’t going to be cash flow positive, but I didn’t want to be running a massive deficit either.

The thinking behind most investment properties in Toronto, at the time, was that the market was going to go up forever. No, seriously – this was the thinking. You’d try and pay off most of your expenses (mortgage plus some of the operating costs) and assume that your property would continue to appreciate in value over time. Evidence shows that this thinking, in hindsight, was correct.

But I was more concerned with the cash flow of the property as I would rather have money in my pocket and a turnkey operation than make an assumption on the bull market.

So with that in mind, I turned my attention to the Wilfred Laurier campus, where the market was entirely different.

Every other weekend, I went to Waterloo to scope out properties with my younger brother who was in his fourth year of a five-year program at Laurier & Waterloo. The idea was that Neil would live in one of the rooms rent free, and he would look after the property and attract suitable tenants for the following year.

As I said before – the market was very different in Waterloo. Cap rates were DOUBLE what they were in Toronto, and these properties were cash flow positive.

There was a lot for sale up there, but most owners were priced about 20% over market value.

I only wanted to look at properties with an A++ location, and after seeing a lot of dilapidated houses, I decided that I also wanted a property in A+ shape.

We found a property on Hazel Street which was absolutely, positively, perfect.

The property was two, five-unit dwellings together on a single lot. There were a lot of very shady landlords up in Waterloo. My brother and his friends lived in a seven-person house that was legally zoned for four. I had no interest in running an illegal operation, and after speaking with the city inspector, I realized that eventually all of these landlords would get caught. They were just hoping they would make more money in rent than they would have to pay when they were fined.

The property was in excellent condition, with one of the units having been renovated three years ago, and the other unit essentially being brand new. The two units were separately metered, which meant I could charge the tenants for their hydro.

The location was A+++. Yes, I added another “plus.”

It was the second house in from University Avenue, on Hazel Street.

This was as close as you could possibly be to campus (on the north side), and it was steps from Pizza Pizza, ScotiaBank, and the plaza where kids would go for groceries.

But the rents were what sold me on the property.

There were ten bedrooms, and each kid was paying $500/month. Each kid was on a 12-month lease, and if the kid wasn’t living there during the summer, it was his or her responsibility to sublet the room, or eat the cost.

The price of the property: an even $500,000.

With $60,000 in rent, the cap rate was a tasty 12.0%. This would have been unimaginable in Toronto.

At the time, you were able to get 107% financing on residential properties, and you only needed 5% down with an investment property like this one.

With $25,000 as a modest downpayment, I would be making monthly mortgage payments (rates were at 5.29% for properties like this one) of about $2,500 even, including CMHC insurance.

Property taxes were only $4,200, or $350 per month.

Water and gas were huge expenses considering there were ten kids living there. They were almost $700 per month combined.

All in, I’d be looking $3,450 per month in mortgage and operating costs, and I’d be bringing in $5,000 minus the $500 for my brother to live there.

All told, I’d be putting $1,050 into my pocket each month.

That would translate to $12,600 per year and a 50.4% return on my $25,000 downpayment.

The numbers were phenomenal, and my mind was made up.

I put together an offer for an even $500,000 – every penny of the asking price. My offer was conditional on home inspection, otherwise, it was clean.

As luck would have it, there was another offer on this Hazel Street investment property, and the listing agent couldn’t believe it! I was dealing with a very hot Toronto market at the time, and multiple offers were common place. But in Waterloo, they were unheard of. The listing agent said he’d never experienced this in his entire career and he really didn’t know what to do with it.

I was willing to pay more than $500,000. What did I care? How would $505,000 make any difference in the return on my investment? I wasn’t chasing the capital appreciation like everybody in Toronto was. I wanted the monthly cash flow.

I improved my offer to $505,000, and both the seller and the listing agent thought they’d died and gone to Heaven.

But there was a snag, however: the other offer was unconditional, and there was no way in hell I was going to buy a half-million-dollar, ten-unit property without doing a ridiculously thorough home inspection.

I tried as hard as I could to convince the seller that my $5,000 premium was worth the “risk” of me pulling out of the deal, but they didn’t agree.

In the end, the property sold to another investor for $500,000.

Looking back on this, I’m so grateful that I didn’t end up with this property.

It’s been over five years, and I can’t imagine what my life would be like had I made this “mistake.”

First and foremost, the $25,000 downpayment I would have made at the time represented more than half of my net worth. I had a rather lean introductory eighteen months in the business, and the start-up costs associated with becoming a full-time real estate agent are substantial.

The stock market was not performing well at that time either (although I don’t have a single penny invested in ‘the market’ today, nor will I ever put a single penny into the market again, I did back in 2005), and the end result was that I was quite cash poor at the time.

However the major reason that I was thanking my lucky stars for “losing” the property came about a month later when I went to visit a couple of friends of my brother’s at their house on Ezra.

Brad and Dan were, to put it bluntly, complete morons.

They were obsessed with Jackass, and when we rolled up to the house on Ezra, Dan was sitting in a toboggan on the roof of the house and Brad was standing on the lawn with a video-camera.

Dan yelled, “Ready,” and then proceeded to slide down the roof on the sled and land in the bushes below. He jumped up and yelled, “Success!” and high-fived Brad.

The next day, they got bored (and really stoned) and decided to set fire to a pile of wood in the carport. The carport caught on fire – but this was probably okay with them, since it meant they could just light their joint from the burning flames.

Brad and Dan represented what every university student brought to the table: complete and utter risk.

I once talked to a real estate investor who told me, “I only buy buildings where old ladies live. Because they’re quiet, they never create any problems, and the only reason they’ll ever leave the building is if they die.”

There’s a reason that cap rates are/were 12% for student residences in Waterloo – there’s a TON of associated risk.

At the time, I was more than willing to accept this risk. I know what university students are like. They’re dirty, messy, loud, and they live in their own filth. They don’t respect other people or other people’s property.

But it wasn’t until I saw two morons light fire to a carport that this really hit home to me. I guess you could say it hit me like a ton of bricks, or perhaps like a toboggan sliding off a roof…

I’ve made five other significant real estate investments since I lost out on the house on Hazel Street, and all have been successful. I often wonder how much that property would have hampered my ability to buy into a variety of different investments, and I wonder how many headaches I would have had along the way.

My brother would only have been living there for one year, and then I would have had to either hire a professional property manager, or look after the property myself.

Sometimes the best investments are the ones you never made.

There are big losses, small losses, big gains, and small gains.

I’m convinced that so long as you eliminate the big losses, and all your investments take the form of the other three outcomes, you’ll win out in the long run…

MattO

at 10:19 am

haha I think I might have lived in that 7 person house! well at least, one of the many in the area. We got in trouble for it too, and my housemates that lived in the basement (there were 3 of them) had to move out halfway through the school term because the house failed fire safety inspection standards. Pretty brutal..

And as for being the landlord of a property rented out to university students, definitely good luck on your part to miss out on that house. I remember punched holes in walls, broken windows, broken appliances, etc etc etc…way too many headaches.

Jeremy

at 10:20 am

Hey! I grew up outside Kitchener and now live in Toronto and work in Waterloo, but I still say I’m from Kitchener. Sure it’s not as clean as Waterloo, but there’s no reason to be ashamed of it. There are places in Kitchener I’d live if I were to leave TO. And like you pointed out, large parts of Waterloo are trashy student housing.

Marina

at 2:29 pm

Contrast the names of Toronto condos:

Zen, Spire, Festival

to the names (admittedly – nicknames) of Waterloo student housing:

Scummydale, Cockroach Inn

Where would you rather invest? And, yes, I’m a proud former resident of both of these fine establisments 🙂

moonbeam!

at 4:16 pm

I guess landlords don’t or can’t ask students for a damage deposit?

WEB

at 6:35 pm

Great post as usual!

Cap rate is calculated using net operating income (before interest) divided by purchase price. Thus, you need to subtract your expenses to calculate the cap rate.

Potato

at 11:33 am

“although I don’t have a single penny invested in ‘the market’ today, nor will I ever put a single penny into the market again”

Hmm? All-or-nothing on real estate then? I’m pretty sure we’ve hashed it out before on that one, so I’ll leave it alone and get on to nit-picking:

“There were ten bedrooms, and each kid was paying $500/month. […] The price of the property: an even $500,000.

With $60,000 in rent, the cap rate was a tasty 12.0%. This would have been unimaginable in Toronto.”

I think you meant to say the gross rental yield is 12%. The cap rate looks to be closer to ~7%, which sounds more typical… though still better than what you could get in Toronto at the time (and it’s worse now: there’s a house around the corner from my parents that they’re trying to sell at less than a 2% cap rate! LOL).

Anyway, sometimes it’s good to miss out on deals for whatever reason. Another one here might be that the cap rate could have been temporarily inflated due to the timing — do you know if the rent/room has stayed that high as the double cohort worked its way through?

David Fleming

at 12:16 pm

@ WEB & Potato

I’m going be completely honest here – despite the fact that any definition you find online of “Cap Rate” clearly shows that you use net income over the purchase price, every single real estate listing I’ve seen has always used gross income. True -they are confusing gross/net, or the terms “cap rate” with “rental yield,” but in a strange way, I have come to accept this.

I’m not sure if this is just “the way it works” in real estate. Even my investor clients refer to the gross income over purchase price as “cap rate.” Even my mortgage broker….etc…

As for the “all or nothing” on the stock market and real estate market, well, I guess it’s a function of my knowledge and lack of time on my hands.

I don’t trust any “professionals” to invest my money. I think the fees in mutual funds are ridiculous.

I do have some money invested in index funds, but I don’t really consider that “investing in equities.” It’s like saying “Buy me THE MARKET” in general. The market goes up, the market goes down. But the days of individual stock picking or even individual mutual funds are long, long over for me…

WEB

at 11:35 pm

The fact that your investor clients and mortgate broker (in addition to MLS listings) use gross income to describe the cap rate tells me we must be closer to a market top than the market bottom in Canadian real estate.

It reminds me how during the dot.com boom, people would start to value companies based on revenue (or even future revenue) instead of profit. That is when you know things are getting dangerous. Very close to the top of the tech stock boom, I took a very quick look at Nortel. What was amazing is that this time, the company over the previous 10 years basically earned nothing (cumulatively.) Despite this, Nortel represented a huge portion of the entire TSX!

I understand you not trusting “professionals” to invest your money. Yes, it is true, there are as many dishonest and/or inept people in investments as there are bad real estate agents. But there are exceptions in both industries. For example, you are an honest and competent agent. In investments I recommend that you look at Chou Associates. I personally know the owner/manager, Francis Chou. He has a fantastic LONG-TERM record (20+ years) and he did not buy tech stocks during the mania. He is also honest- on three occassions or so, he returned fund management fees because he felt he did not do a good job that year and thus didn’t deserve to get paid (I’m not making this up!) Or how about Warren Buffett of Berkshire Hathaway? He is certainly a man that you can trust and is of the highest competence.

That being said, index funds are indeed a very good way of investing. Mutual fund fees are very high in general and most funds underperform low cost index funds. So that is indeed a great way to go. Warren Buffett has said this himself.

Here are a few articles on Francis Chou:

https://secure.globeadvisor.com/servlet/ArticleNews/story/gam/20090402/RCARRICK02

http://www.canadianbusiness.com/my_money/investing/mutual_funds/article.jsp?content=20060228_111027_964

Potato

at 5:52 pm

Yeah, index funds are a great way to get into equities, good to hear you do have some diversification 🙂 Though I’m mostly an active investor myself, I do index part of my holdings (indeed, most new savings go to the index side), and it’s what I recommend most people do.

WEB: you know Francis Chou? Cool…

apom

at 11:44 pm

haha your right about the whole Waterloo vs. Kitchener thing. It’s like Manhattan vs. the bronx. Based on appreciation I think you would have been in a good position today. Renting to students is risky tho. You need the right group. I have seen some horrendous things happen to rental properties in my day. I have personally seen upwards of $20,000 of damage in some houses but thats a small minority for sure.

Has any invested in Thunder Bay? I’m crunching the numbers and some cap rates are as high as 20%. I guess this is driven by the students. I don’t even care about appreciation at rates like those. Just get me my money back from the property after 6 years and I’m fine.