We knew this would happen….right?

We knew it was inevitable, didn’t we?

Last week, mortgage rates rose some eighty basis points. Let’s start with the the woulda-coulda-shoulda and then move on to how this will affect the real estate market going forward…

I hate to say “I told you so.”

Except when I’m right.

Then, it’s awesome!

On March 5th, 2010, I wrote a blog post called “Get A Mortgage Pre Approval.” You can read that post here.

Okay, so I didn’t exactly predict that rates would go up (or that they’d go up this soon), but my point was that rates could go up, and that’s reason enough to get a mortgage pre-approval.

When I meet a new buyer-client, the first thing I ask is “Have you been pre-approved for a mortgage?”

Part of the reason I ask this question is to determine how far along in the process the buyer actually is as well as how committed they are, but it’s also to get that buyer locked in to an interest rate in case rates rise.

Some buyers balk at the idea of the pre-approval because it’s “a lot of work.” That’s a terrible excuse.

Spend two hours, fill out the online application, get your T4’s, NOA’s, and pay stubs together and make it happen.

I feel bad for all the people that didn’t get a pre-approval in January, February, or March who are now kicking themselves.

Last week, mortgage rates went up a whopping eighty basis points.

A typical five-year, fixed-rate morgtage went from 3.69% to 4.49%.

And the most interesting part about the rate hike was that it came with mixed reviews.

Some people are obviously upset with the rate hike, most notably those entering the housing market in the next few months who won’t benefit from all-time-low interest rates.

But others applaud the rate hikes, saying “enough is enough” to ridiculously low rates. Many people think that the rates have allowed buyers to enter the real estate market who have no business buying, and this has helped raise prices of entry-level condominiums downtown.

So what does the future hold?

Call me a salesman for life, but I’m not convinced that this rate hike is going to have a major impact on our real estate market.

All that has happened is that mortgage rates have gone from “ridiculously affordable” to “really affordable.”

Think about it.

We’re coming off some of the lowest interest rates in the history of our country.

The affordability factor is still incredible!

I don’t have an up-to-date graph (since StatsCan charges $3.00 to download a chart and they don’t even let you preview it…), but here is a great graph that shows rates from the 1950’s into this decade:

And we all know what has happened since this chart went out of date – rates went down even further.

When I locked in to a five-year, fixed-rate mortgage for my current residence back June of 2007, I was happy to get a 4.99% rate which at the time was phenomenal.

Rates went up shortly thereafter, and some of my clients received rates approaching 5.99%, but then rates came crashing back down to as low as 3.49% earlier this year.

So who cares if we’re back to 4.49%? Wait, okay, I know a lot of people care…

What I’m saying, is that how much does this really change things for a buyer?

Take the example of a $300,000 condo purchase with a 20% downpayment:

Monthly Mortgage Payment @ 3.69%: $1,014.35

Monthly Mortgage Payment @ 4.49%: $1,128.18

First of all, consider how ridiculously low that monthly payment still is. It’s a far cry from when interest rates were at 22.5% back in the 80’s, because then the monthly payment would be $4,304.97…

But who among us can’t afford another hundred bucks a month?

Note to all potential buyers: if $114 per month is going to make or break your ability to live without selling your body for crack, then maybe you shouldn’t be entering the housing market in the first place.

I know you have to draw a line in the sand somewhere, but I just don’t see a “large” difference between the monthlies for the new/old rates.

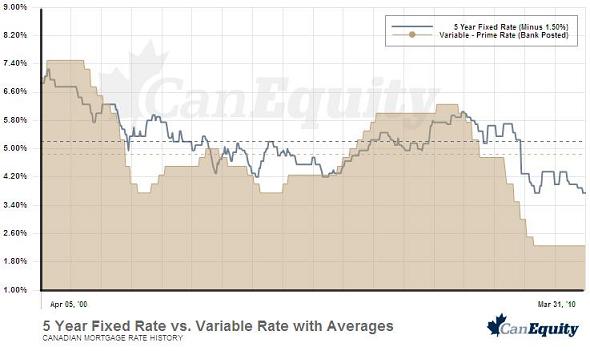

Take a look at this graphic below:

This graph is completely up-to-date and shows the five-year fixed mortgage rates during the last decade and the relationship between the variable and fixed rate.

It’s interesting to note that variable rates have hovered above that of fixed at several points during the last decade.

You can’t turn on the TV without seeing an ad for your friendly, neighbourhood bank in which they depict “you” as the complete moron who can’t tell the difference between variable and fixed rates, and thus you enlist the help of the 31-year-old high-school drop-out who works at one level above “teller” at your bank who is going to explain to you when, why, what, where, and how you should evaluate variable versus fixed.

But I digress…

I was a little frustrated last week when some people predicted Armageddon after the mortgage rates increased.

Rates are still incredibly low, and I’m just not convinced that the decrease in affordability is going to shake up our market.

When rates go beyond 6.0%, then I’ll come up for air.

But another glance at the graph shows that 6.0% isn’t that bad…..historically.

Are we going to see rates in double-digits once again?

Probably…..at some point….but when?

Take a look at the first chart again that began in 1951.

People talk about “seven-year real estate cycles” or “twelve-year market cycles,” but if I were an amateur chartist, I would conclude that there is a “sixty-year interest rate cycle” which has a huge peak in the middle! Rates were at about 5% in 1951, went as high as 22.5% in 1984, and then came back down to 5% in the last couple years.

Does this mean that rates will hit 22.5% again in the year 2043?

Who cares. And that comes without a question mark because it’s more of a statement…

All I know is that rates are at 4.49% and that is still incredibly affordable.

What the future holds, I don’t know.

But does anybody?

Meh

at 10:24 am

How about we run your example with some numbers that actually represent the common situation a buyer is in today instead of a 20% down on a cheapest-unit-in-the-city example you just did?

420,000 house, 5% down, 35 year mortgage.

399,000 mortgage -> 1,686.69 @ 3.69%

399,000 mortgage -> 1,875.61 @ 4.49%

Only 150$ more a month you say? Well this is the same buyer that couldn’t afford the 2,032.32 a month a regular 25 year @ 3.69% mortgage was. So it’s only 150$ more than previously, but it’s also only 150$ away from something they couldn’t afford.

David Fleming

at 10:38 am

My example was for $114, yours was for $150.

Meh.

Meh

at 10:46 am

Yes, but your example is unrealistic but for a tiny number of sales.

TC

at 11:03 am

Interesting analysis David However, I think it would be wise to consider the the direction of the coming trend in interest rates. Watch the bond markets, as those yeilds continue to rise so will mortgage rates. We have really solved nothing since the 2008-09 market crash and all that has happened since then is a big game of extend and pretend. If you honestly look for the true numbers and statistics and look at the whole picture you will see that this global financial crisis is only just starting. Double digit interest rates???…..I can assure you will be an acknowledged fact much sooner that anyone would dare think!!! Caveat Emptor………

Meh

at 11:13 am

Oh wait, are you saying that 114 is almost the same as 150?

Apparently you missed the point.

JG

at 11:27 am

“the 31-year-old high-school drop-out who works at one level above “teller” at your bank who is going to explain to you when, why, what, where, and how you should evaluate variable versus fixed.”

ouch!

David Fleming

at 6:55 pm

@ JG

I know, I know. You’re a banker!

I was speaking from experience – at my TD bank which is run by children, and a couple of burn outs who I remember from high school.

My statement was meant to me more funny than to blanket the entire industry.

JG

at 7:31 pm

@ Fleming –

Nothing to worry about – i thougt it was hilarious due to its accurate description of most. Banks are nothing but a retail clothing store. Ever notice you go in there to get a basic chequing account and they attempt to ‘sell’ you everything under the sun!! visa’s, lines of credit, loans, – all credit products. Ask them about an investment vehicle – you’ll get a blank stare!! Pathetic – just my opinion from an ex-business banker – now dealing solely with mortgages…..but i digress.

@ Meh-

I too agree examples you find in news articles are terribly inaccurate. I was reading an article over the weekend and they quote a $200,000 mortgage balance! Come on!! Who has a $200,000 mortgage. I like Fleming’s as its somewhat more accurate @ $300,000. In my experience this is a more real number to use.

But even these examples have little bearing in the real world. Right now the market is all about conversions!! I spent the last week dealing with them. Whether they should have or not is another story……but i am seeing people with 1.5% VRM rates converting into fixed rates at 3.70% – and people are still crying!! The lack of reality people have about mortgage rates is distiburbing. Since when did 3.70% become too high of a rate. I see people’s payments increasing $400/mth and their hurting. I see people who will stay with the VRM because they cannot handle the increase in payment. If they cannot handle a 2.20% increasing what is that saying about their affordability?

I dont really see the rates reaching double digits anytime in the near future. I can see them going back to their historical norms i.e. 5yr fixed being 5.50%. And as shocking that is, this will dampen the real estate market for a short while as people wont be able to jump in as quick. They will have to save a bit longer for their down payment.

Finance Minister has already incorporated news rules!! All rental purchases now must have 20% downpayment, and the client has to show $100k in liquid assests. What do you think this will do to the average joe who’s looking at buying a ‘rental’ unit? And good luck lying about owning a home, Equifax now reports it on your bureau. So as for pre-contructions, i think sales may slow down for this.

Existing home owners who want to refi? because the rate hike is killing them! You can only refi to a max of 90% Loan to value of the property?! I know, i know, who the heck takes it up to 95% ltv – but trust me, a lot of people. i am still seeing mortgages that were bought with 100% financing, and what kills me is the sense of entitlement people still have in this situation!!

Its almost as if a perfect little storm is brewing right now, and it will be very interesting to see what happens with the real estate market over this summer. April 20th is when the Bank of Canada reviews the Prime rate – its projected to go up! Which means, a lot more people wanting to get a fixed mortgage. They can expect at least a 3%-4% increase in rate – which is what a $600 -$700 in monthly payments.

ok, now i am just rambling –

thanks.

Chuck

at 10:38 pm

I think if rates hit double digits, it’s a race to the soup line for just about everybody.

Potato

at 3:57 am

It may “only” be $114, but that’s 10% of their mortgage payment!

Plus, that’s a single rate jump on a single day. There are more to come to get us back to where we were — as you say, just ~2 years ago rates were touching 6%. Now that kind of rate would be ~$350/mo more on your entry-level mortgage, or ~30%, and I can’t see how that won’t trickle through to housing prices.

After all, in your description of your Rezen condo you only had ~$300/mo of positive cash flow — rates returning to where they were a few years ago at renewal time would eat basically all of that, and it would be even worse for the sucker who bought after you, since they paid even more than you did!

@JG – People who can’t handle a rate increase are going variable?? Yikes.

George

at 11:58 pm

I agree with Chuck. I think there is a virtual ceiling on mortgage rates for the foreseeable future. Double digits would destroy the financial well-being of too many people/families. I think it is a reasonable assumption to budget for an average long-term prime rate to be 4.75%, meaning a variable mortgage rate just below 4%.

The Chijindu Law Firm

at 8:44 pm

Notwithstanding the rise, rates are historically very low. This is the time to come on board and buy.