I hate writing this post, every September, as it marks the official end of summer.

Then all the “remember when’s” start flooding back, like, “Remember when it was June, and we were so excited for summer?”

It’s like on the last day of vacation, when you think back to the first day you arrived, and how you had the whole trip ahead…

Well, summer is over, folks. So let’s talk about the 2016 fall real estate market, and discuss what lays ahead.

Every summer, when NFL camps open, and I start to get excited about the upcoming season, I come to the exact same realization: in order for football to start, the summer has to end.

It’s so unfair.

It almost makes you want to become a CFL football fan. Almost…

It’s a classic case of “you can’t have one without the other.”

Football can’t start, until the summer ends.

One of your favourite things can not coincide with one of your other favourite things.

Of course, I’m negative by nature. Try as I might to see everything in life as “glass half full,” I’m still learning.

So I suppose an optimist would say, “The gifts just keep coming! After the best season of the year, we get another present in the form of football!”

Yeah. I can’t quite see it that way.

The “first day back” after Labour Day just feels different.

You just know it’s not summer anymore.

It’s as though every person in the city is 5% less happy. Smiles aren’t quite as wide, hugs don’t last quite as long, laughter tails off where it once continued…

Remember what it was like, back in Grade 7, getting on your bike at 8:35am to head to school for the first day back? It was noticeably colder, there was dew on the lawns on your street, and you were just a little more tired than usual.

It was tough getting back into the rhythm.

Your teacher was prepared, however. It was as though she had been drinking coffee and taking speed since 4:30am. She was operating at a whole other level, and you were staring out the window, watching that first leaf fall off a tree branch.

You’d stare outside, hoping to see a squirrel, or a car drive by – anything to take your attention away from French verbs.

Je, tou, il/elle, nous, vous, ils/elles. Holy crap, how did this happen? Where did the summer go?

And the worst part was: you knew the school calendar would never be longer than it was at this very moment. This was the first day of a ten-month school calendar. Where the HELL did the summer go?

For a lot of people, it’s like that in real estate.

I’m in the office, alone, writing this on Friday, September 2nd. It’s a ghost town around here.

And it was “slow” in the summer, as many people – agents, buyers, sellers, inspectors, mortgage brokers – all figured they could make themselves scarce in the “slow summer months.”

From my perspective, the real estate calendar lasts 365 days. There are slow(er) periods, but you can’t ever truly take your eye off the ball.

A new listing came out today on Rushbrooke Avenue in Leslieville. Yes, a new listing, the day before a long weekend.

How many agents and buyers missed that one?

In any event, by the time you read this on Tuesday, the market will be back in full swing, and it’s going to get crazy.

It’s going to get absolutely wild.

A lot of what I think is going to transpire this fall season, ie. my “predictions,” are things we’ve talked about over the last few months.

But whether this is a refresher, or whether it’s

1) Prices Will Continue To Rise

This should come as no surprise. To any of you. At all. Period.

Every once in a while, and it’s happening far less frequently, I have a client or a random emailer say something like, “We’ve decided to put our search on hold until prices drop.”

I’ve been hearing that since I got into the business twelve years ago, but it rarely happens anymore.

I had one client, who owns a $2,000,000 investment property, and lives in a $350,000 condo, tell me he wanted to “wait until prices dropped” to purchase his family home, since what he wants is $2,500,000, but he only wants to spend $1,700,000.

Of course, if the market dropped, and that $2,500,000 house was available at $1,700,000, the multiplex and the condo would drop too.

But this just illustrates the ideas people come up with when they’re trying desperately to convince themselves that what they want to happen, can happen.

Sorry, folks, but prices aren’t dropping this fall, or any time soon.

Call me a snake oil salesman if you want.

You wouldn’t be the first person, after all.

Last week I got this message on Facebook:

Wow!

What a mouthfull!

I don’t really monitor the comments on Facebook, but a colleague showed me this, then told me the person who posted this message has a profile picture of the Twin Towers burning on 9/11……with smiley-faces. Yeah. Right. Soooooo…….

In any event, this snake oil salesmen is here to say that the average price of a Toronto home will not be dropping, any time soon.

It’s what people don’t want to hear, but it’s what most people are ready to acknowledge, which is different than in years’ past when the denial was a lot greater.

–

2) The Fall Will Be Hotter Than The Spring

Anybody can “predict” that prices will continue to increase, in a market where the average home price has increased every year for two decades.

But I’m here to predict that the fall will be hotter than the spring, and by that, I’m referring to the average home price in the fall actually topping that of the high point in the spring.

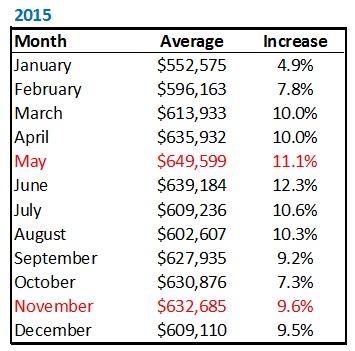

Take a look at this chart from 2015:

Here we’re looking at the average sale price of a home in each month of 2015, as well as the average increase of the price of a home, year-over-year, in that month.

Two things to note here:

- The “high point” of the spring market, in May, was $649,599, which was more than the high point in the fall, of $632,685 in November, even though November fell a half-year later.

- The average appreciation was higher (ie. mainly double-digit, 11.1%, 12.3%, etc) in the spring than in the fall (ie. single-digit from September to December).

Assuming that house prices are going up 1% per month, as the above chart shows, I find it fascinating that the November average sale price was unable to top that of May!

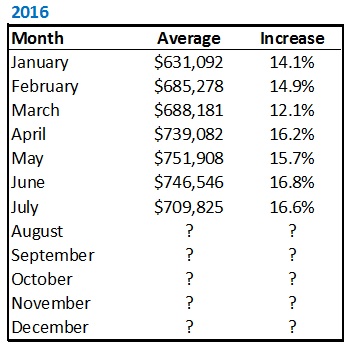

Let’s take a look at 2016 so far:

The first thing you’ll notice here is the insane appreciation!

The average house price in April,l May, June, and July was up over $100,000, year over year.

Now my prediction, as I alluded to above, is that “the fall market will be hotter than the spring market.”

What I mean by that, is that in last year’s market, we saw the average house price in the spring top the average house price in the fall.

That ain’t going to happen this year.

It’s common, it happens just about every year.

But in the fall of 2016, I expect the average house price in October and November to be in excess of $755,000.

If that happens, it means that the October average house price will be up 19.8%, year-over-year, and the November average house price will be up 19.3%.

That’s insane.

But so too is our market…

–

3) Inventory Will Be In Low Supply

In case you missed August’s blog called, “Toronto’s Real Estate Problem: Simple Supply & Demand,” I suggest you have a read!

That was one of the better blogs I’ve put together this year, in terms of offering insight no one else is providing, but also in terms of the spirited debate in the comments section, which is always full of informative viewpoints.

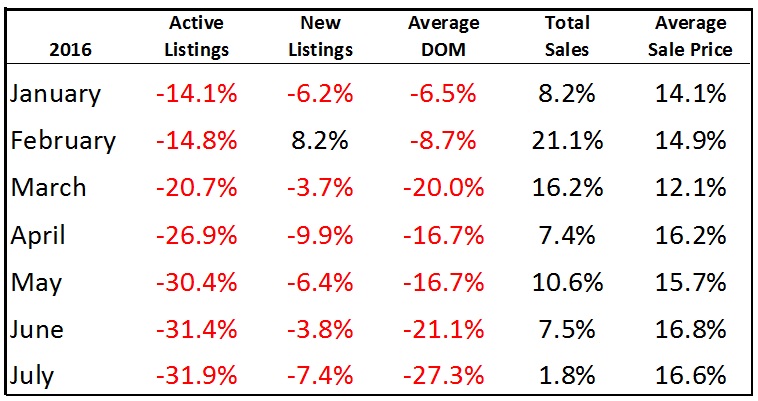

The most haunting graphic of that blog post is this:

The inventory levels are lower than they’ve been since TREB re-drew the MLS districts in 2008. Otherwise, I wonder how far back we could go…

I don’t believe that this trend – the decrease in active listings from 14.1% in January all the way to 31.9% in July, is going to continue.

I can’t fathom seeing -35% in August, and -39% in September.

But I can definitely see the overall trend continue, as levels should be at least 25% lower than they were last fall.

All this is going to do, of course, is give buyers fewer options, and make them push harder to get what is available.

And thus my #1 prediction will be helped along…

–

4) Pre-Construction Prices Will Rise To Levels That Make Less (No?) Sense

There was an interesting article in the Toronto Star last week titled, “If You Think Condo Prices Are High Now, Fasten Your Seatbelts”

I find it ironic, because as much as our government – whether it’s municipal, provincial, or federal, wants to “help the middle class” and provide “affordable housing” to everybody, in every city, they sure as hell aren’t going to give up their cut of the pie in order to do so!

The City of Toronto charges a hell of a lot of fees to condo developers, and those developers, of course, pass it along to the consumer.

Development charges run amok.

Green levy, park levy, transportation levy, education levy – all kinds of levies, for all kinds of money, charged to the developer for each and every unit.

At no point is a developer going to say, “Well this is simply unaffordable to the consumer, so I think I’ll absorb this cost.”

Not a chance.

Read through the standard builder’s forms and you’ll see that they charge everything back to you. They charge you the amount that Toronto Hydro charges them to install a meter! They charge you the fees that they pay to the Law Society of Upper Canada!

So with the city of Toronto charging developers more, it only means that the prices of pre-construction will go up, which is crazy, since the prices already make no sense.

It’s crazy looking at some of these developments charging $800 or $900 per square foot in pre-construction, when you can buy a resale property next door for less, take possession sooner, and not take on the associated risks, and closing costs.

So with pre-construction condos set to rise $50 per square foot, will we see a drop off in sales?

Probably not.

I know, it makes no sense. But buying pre-construction never did.

–

5) CMHC Will Talk About Policy Changes

It’s about time for the Finance Minister to say he’s “closely monitoring the Canadian market,” and perhaps add that he “might intervene.”

This happens twice a year, every year.

And the Finance Minister and CMHC have both been quiet since they introduced a higher down-payment requirement back in February.

That seemingly had zero effect on the market here in Toronto, and it has to feel like every policy change the CMHC makes to try and cool the market, doesn’t, and sooner or later, they’re going to overreact.

Not quite “Vancouver 15% tax” overreact, but still…

Over the last few years, we’ve seen a lot of policy changes introduced in attempts to cool the market.

40% amortizations are gone, so too are 35%, and 30% unless you meet certain requirements.

Cash-back and 0% mortgages seem like a century ago, having been replaced with the minimum 5% down years back.

20% down on investment properties or second properties was a doozie.

20% down over $1,000,000 simply made ever $700,000 house worth $800,000 overnight. Bravo!

Increased insurance premiums on CMHC-insured mortgages was sneaky.

And increased down payment requirements from 5% to 10% between $500,000 – $999,999 was something long-rumoured, finally-implemented.

So what’s next?

If it’s not this fall, it’ll be next spring.

Something is going to come from CMHC, or perhaps it’s time for non-CMHC-insured mortgages to get their fair look. We talked about this back in July in a blog post you can read HERE.

So if the top story on the evening news, twice a week, from September through November, is the average price of a home in Toronto, you can guarantee that Mr. William Francis “Bill” Moreanu will be brainstorming ways to shake up the lending market.

–

6) Multiple Offers Will Be The Norm, Everywhere

My blog from two weeks ago didn’t get a lot of love: “Prediction For the Fall Market: Offer Dates For Condos Will Run Rampant.”

But it’s worth reading, because it’s going to be a new reality of this market.

If you’re a would-be condo buyer this fall, you have to read that blog post.

We will start seeing condos hit the market with offer dates, and we might even see the old “under-listing” strategy with condos, as we see with houses.

I admitted in that blog post – I don’t like it, but I have to do it. The market demands it, and so too do the clients.

If you see a new listing for a condo you like, and it doesn’t have an offer date, then get out and see it that afternoon, or be prepared to kiss it goodbye.

–

7) We Haven’t Heard The Last Out Of Vancouver

I know, I know.

You’re tired of this.

I am too.

It didn’t stop me from posting a massive rant last Wednesday on this very subject, however. Well, wait, that’s not entirely fair – the blog was about how what happened in Vancouver won’t happen here in Toronto.

But the word “Vancouver” in my circles immediately makes people think “fifteen percent tax” these days.

I saw a friend this weekend – also in real estate, who I haven’t seen in a few months, and after the salutations were exchanged, the first thing he said was “Wow, Vancouver, eh?”

That’s the most impactful, most significant thing that’s happened since we saw each other last, and one sight of me – a real estate agent, and that’s what he thought of.

I don’t think “Canucks” or “Whistler” when I hear the word “Vancouver.”

Maybe I’m obsessed with real estate, or maybe this is just such an insane idea – the 15% tax, aka the “ban on foreign buyers,” that I can’t think about Vancouver in any other way.

In any event, we’re going to hear more out of Vancouver this fall.

Once we see the impact of the tax, ie. the sales numbers from September, October, and November, we’ll really get a sense of where things stand.

Then comes the election next spring, and I wonder if the Conservatives will tout this as a victory.

–

So that’s all I’ve got, folks!

2,500 words on the first day back. Brevity was never my strong suit.

I have a wicked story to tell you in Thursday’s blog, that might keep you in the city over the next long weekend. Stay tuned for that one.

For those of you in the market right now, get ready, and although it’s cheezy, hold on to your hats!

The market is going to absolutely explode this week, and it’ll be chaos for three months.

Welcome to 2016 fall real estate market!

H. Marshall

at 10:35 am

That prices in the newer condos are heading upwards, is not that surprising.

I am sure that it this is largely caused by investors looking to be landlords or to rent furnished units short-term on Airbnb or on other websites. This is a growing market for condo units in the tourist/convention areas.

What concerns me is how high the prices have risen this year for the older neglected condos that are in terrible financial and physical shape. Those buyers are going to get badly hurt.

Kyle

at 4:30 pm

Way to Kevin, for correcting their asses with maths and fax. Where would we be without you?

Kyle

at 5:10 pm

Ha! Looks like my ass needs correcting too. Should say, “Way to go Kevin”. Unfortunately i threw out my fax machine in the early 2000’s but i’ll gladly accept the maths via email.

Call the exorcist

at 6:18 pm

Way to go Kevin, blame the real estate agent… Reminds me of the “Millenial Revolution” lady being furious at her boomer parents for forcing the horrible dream of home ownership on her… You poor, poor souls… Damn these evil forces forcing our hands… Damn them straight to hell.

Kyle

at 1:25 pm

I know it’s totally off topic, but i 100% agree. The Millenial Revolution story is a total sham. Great for them for saving up a million, but the whole spin is so disingenuous. They basically scrimped and saved their way to a million for over a decade in a constant state of being “Portfolio Poor”. It certainly wasn’t the renting/investing strategy that got them to where they are. Meanwhile anyone in their home city of Vancouver who bought a house ten years ago became a multi-millionaire by simply owning and living in it. They claim their portfolio has allowed them to retire and travel the world, but i think the reality is they need to travel to other parts of the world, because a $1M portfolio doesn’t generate enough to live off of in Vancouver. What i find most hilarious though is how the Garth Turners and Rob Carricks hold these guys up like they’re heroes. The truth is they didn’t become millionaires because of the strategy, they became millionaires in spite of it. And the reason they are getting so much media attention because finding a millionaire renter is like finding a unicorn. While millionaire home owners are a dime a dozen.

Kramer

at 5:10 pm

Yes, good for them for putting $1MM together by 31, an amazing feat no matter how you get there…

I have tried giving them the benefit of the doubt… I have assumed their personal story (which is as undesirable as it is possible for most Canadians) is not a road map for people to follow but rather a way to say “there are other alternatives to home ownership for living and accumulating wealth”… i.e. more straight-up cash saving and other forms of investing.

However… their delivery of this is absolutely TERRIBLE and it shows just how entitled and spoiled these two little shits really are.

Pissing on boomers and making some kind of generalization that every boomer tells their kids that if they don’t own real estate they are a “loser”… If this is how they are trying to group everyone into what they’re selling, HUGE miss and this might be why some couples would actually punch these two in the face if they came across them. Many see boomers as a hard working generation that was extremely family oriented (maybe that’s why one of their primary goals was home ownership). I think if they are looking to connect with the masses, they should come up with some new kind of “why”… pissing on everyone’s parents isn’t the right hook.

There are so many holes in all their bullshit. Who are they really addressing here? Is this young couples with great educations and high paying jobs and no kids who are willing to live like paupers for 7 years during their precious 20’s? Thin market. Or are they addressing everyone and saying that everyone can get to $1MM and live off 4% if they try but it might take some people longer if they have children to support or lower paying jobs? I just don’t get it – who are you talking to? What is the goal? Yes, I understand these two have built in some plan so they can have kids one day, etc, but does that mean people who already have kids can’t participate or that it sets them back more years from financial freedom? What’s the goddamned goal here? It’s so convoluted, even if you assume they are not prescribing their exact path because, again, it is as undesirable as it is impossible for most Canadians.

Honestly, this whole thing stinks of these two people leading a unique path, which is commendable, but then trying to back into some kind of “revolution” or “cause” for it so that it can be publicized. There are a lot of people who have done much more interesting things than these two clowns, and/or who have made a lot more money than these two clowns, who are not making a website and publishing their salaries and financials. An aside, when asked if they could name one stock in their portfolio to perhaps share something useful with the public they say “I’m not allowed to give that information” – yah, the BNN guys thought you were a real #### too if it wasn’t obvious over Skype from Kyoto.

If they were listening, I would tell them this… that they are the two most off-putting people I have seen on TV in a while (and I watch Narcos)… you make people feel bad about themselves and their current situations by discussing YOUR financial situation (which is why in a more classy time there was an unwritten rule that you didn’t talk about your salary or financial situation), and you make people want to punch you in the face for talking shit about their parents and a generation that had more grit and dedication to family than their successors.

You might want to hire a marketing agency to work on all that for you, but shit, I think they MIGHT blow your budget.

Frances

at 10:31 pm

David, what “lies” ahead, not “lays”.

Dennis Rud

at 11:52 am

This is an election year and we have seen major issues in the markets during and after election years. What is a major issue this election year and what will be its affects on the economy & hosing market????????