I don’t believe I’ve cracked 3,000 blog posts yet, but I’m close.

In Major League Baseball, three thousand hits is what they call a “lock” for the Hall of Fame. I mean, unless you’re one of the steroid guys, like Rafael Palmeiro. And for those of you thinking Barry Bonds, he didn’t have 3,000 hits. I believe, off hand, he was just over 2,900. Leading MLB history in walks probably had something to do with that, but I digress.

3,000 is a number I’ve been looking forward to simply because of my obsession with sports statistics. All sports. Any sport. I always say, “I don’t watch tennis, but I follow it,” in that I have lists of all the Grand Slam winners in my homemade sports-stats book that I keep next to my bed for when I can’t sleep.

I also have been known, whether passing time waiting for a client, or trying to occupy my mind during extreme turbulence on an airplane, to jot down members of the NHL’s 500 goal club, or MLB’s 3,000 hit club, or the NFL’s 1,000 reception club.

There are countless lists, all-time leaders, and stats that I can memorize and recite.

But my favourite is the 3,000 hit-club. There’s something so pure and so special about 3,000 hits, and although there are more members of that club than the 500 home run club, it remains special for reasons I can’t delve into right now.

Ergo, I have been looking forward to penning my 3,000th blog post for quite some time. Probably since I passed the 2,000 mark.

The problem with having written nearly 3,000 blog posts over fifteen years is that every so often, I write a post that I’ve already written.

And that is what I experienced last week!

Are you familiar with the UBS Bubble Index?

I am. And I have been for some time.

So familiar, it seems, that after having written a fantastic introduction last week to a blog post about the 2022 UBS Bubble Index, it started to feel like deja-vu.

I searched my blog archives, and do you know what I found?

A similar blog post written one year ago.

Damn!

It was bound to happen, right?

Having said that, I don’t believe I can simply skip over the 2022 UBS Bubble Index as a blog story, but I also don’t think it’s worth 3,000 words, since we did that thirteen months ago.

So instead, let’s work it into some “Quick Hits” about a variety of subjects today, all of which are important but not enough to necessitate their own post…

Bubble Trouble…………..Again

There actually wasn’t as much coverage in the mainstream media as I expected, but the “UBS Global Real Estate Bubble Index 2022” was published last month, and my favourite article was this one:

Financial Post: “Drinking The Housing Bubble Tea: Report Labelling Toronto, Vancouver Market As Frothy Contradicts Itself”

Why, you’re wondering, did the report contradict itself?

Per the sub-headline: UBS report rings alarm bells over housing bubbles, but predicts housing prices and sales will resume their upward trajectory.

Monitoring the UBS Bubble Index has been a hobby of mine for the last decade. Not only because, as I’ve explained so many times on TRB, I believe the “historical indicators” that pundits use to assess the health of a market are out-dated and no longer relevant, but also because Toronto has been so prominently featured in this index.

Here is Toronto’s ranking over the previous five years:

2017: #1

2018: #3

2019: #2

2020: #3

2021: #2

And with the most recent edition, you can now add:

2022: #1

But hasn’t the average home price in Toronto risen 40% since the “bubble was set to burst” back in the fall of 2017? And just think: that was 71% this past February…

In case you’re wondering, the blog post I was referring to at the onset is this one:

October 18th, 2021: “The Gift That Keeps On Giving: UBS Bubble Index 2021”

I don’t often praise my own work, but damn was that a good read?

If you like sarcastic, cynical, snide viewpoints, then you’ll love that blog post. I even managed to work in references to CeCe Peniston, Garth Turner, and my GI Joe collection.

Market bears will point to the fact that the GTA market has declined 18%, on average, since February, as a sign that the UBS Bubble Index was right. But you can’t simply say, “The bubble is going to burst” every year for five years, while prices increase 71%, and then after an 18% drop, say, “I told you!”

I filed the PDF of this year’s “Bubble Index” away with my other reports, dating back to 2013. I can’t wait for next year’s edition to tell me more of the same…

“There Are No Mistakes – There Are Only Happy Accidents!”

Great quote, and if you can tell me who said that without Googling it, then you and I can be friends!

Over the last decade, there’s been a trend among Torontonians who are looking to expand their horizons – and home size, that end up selling their Toronto house or condo and move out of the city.

I’ve been moving folks out of the city for almost ten years now, including some very good friends.

But it wasn’t until the pandemic in early 2020 that we could say that people were moving out of the city “in droves.”

I had a lot of long-time clients sell their houses in 2020 and move out of Toronto, and we saw the media cover this topic every chance they got.

At the time, some people suggested that, at the very least a few of these folks would come to regret it. Many thought this might be a mistake.

Here’s an interesting read in last month’s Toronto Life:

“After Less Than A Year In PEC, WE Were Talking About Moving Back”: Why We Returned To Toronto

I said “interesting” and not “great” because the article has some, well, interesting bullet points.

They were looking for a house in Toronto, pre-pandemic, with a max budget of $850,000.

They bought in Picton in December of 2020 for $755,000.

They sold in Picton in November of 2021 for $1,150,000.

They bought in Toronto, in Davisville Village, in early 2022 for $1,916,000.

Does this math add up to you?

Sure, they made $395,000 gross on their house in Picton, but how much did they spend on land transfer tax, real estate fees, legal fees, and renovations?

How did they go from a budget of $850,000 to nearly $2,000,000 in a little over one year?

I’m not sure what the takeaway from this story is, or is supposed to be.

Are we to conclude that people shouldn’t have moved away from Toronto since this one couple moved back?

Is this article celebrating this family or making them out to be fools?

It’s a cute read but there’s something missing here.

On a related note, I’d be interested to hear if any of you have friends or family who have moved out of the city and now have moved back.

Place Your Wagers!

Raise your hand if you said, “The last interest rate hike will be in October, because there’s no way the Bank of Canada will increase the rate again in December.”

Let the record reflect: my hand is raised.

If a broken clock is right twice per day, then what does that say about me?

When the Bank of Canada announced a rate increase of 0.50% on October 26th, there were two ways of looking at it:

1) This is their sixth increase of the year and likely their last.

2) The rate was expected to be hiked by 0.75% and it was only raised by 0.50%, so the government must be holding back that 0.25% (or more) for December.

I was in the former camp.

I just figured that whatever the hike was, it would take us through to the end of the year.

But one friend of mine said that the BOC would raise 0.75% – 1.00% by year’s end, and whether that came in the form of one hike in October or two hikes combined in October/December, it would happen.

Well, it’s starting to sound like that’s accurate.

After the October 26th hike, the consensus was, “They’re done.”

But in the past two weeks, the feeling is that the BOC is going to give us at least another 0.25% in December.

Anybody care to wager?

Gentleman’s bet! Just for bragging rights.

I’ll wager +0.25%. I can’t see another 0.50% increase, but I also can’t see the government taking zero action.

Place Your Wagers V2.0…

This is a potentially less sexy topic but since we’re all addicted gamblers now, and even Wayne Gretzky says it’s cool, shall we wager on the red-hot, dinner-table-worthy, tell-your-children-at-bedtime topic of inflation?

I can’t believe we’re at the point where financial institutions are making forecasts, however, BMO is forecasting a 7.2% rate of inflation for October while RBC is forecasting 7.0%.

This is based on higher gas prices and higher grocery bills, according to most analysts.

Have we come a long way since that “peak” in June?

January: 5.1%

February: 5.7%

March 6.7%

April 6.8%

May: 7.7%

June: 8.1%

July: 7.6%

August: 7.0%

September: 6.9%

Not really.

That 0.1% decline in September wasn’t much to celebrate, but if the rate of inflation for October is higher, as many analysts expect, is there more reason for the Bank of Canada to increase interest rates in December?

The announcement will be made on Wednesday, which is why, among other reasons, we’re exploring this timely topic today.

So by the time you’re reading this, we might already know.

Anybody care to wager?

Also, anybody care?

Don’t Call It A Comeback!

A couple of my trusted allies in this industry have told me this week, independent of one another, that the market is “coming back.”

Just in the past two weeks, they both argue.

While the stats I provided last Monday show that the market has gained stability, I have yet to see or feel anything that shows strength.

But this was a sale that everybody was talking about today:

This property received fourteen offers on the scheduled offer night.

And while it “only” sold for 113% of the list price, that $1,905,000 was what you’d call “a February price.”

In February, however, this house would have probably been listed at $1,199,000 and there would have been 30 offers.

The pricing, strategy, and process might have changed, but in this case at least, the pricing didn’t.

Can one sale be enough to convince anybody? Because it seems to have done the trick on a lot of agents, in tandem, of course, with that “feeling” out there in the market.

But Seriously, What Month Is It?

Just when you think you have it all figured out, well, you don’t.

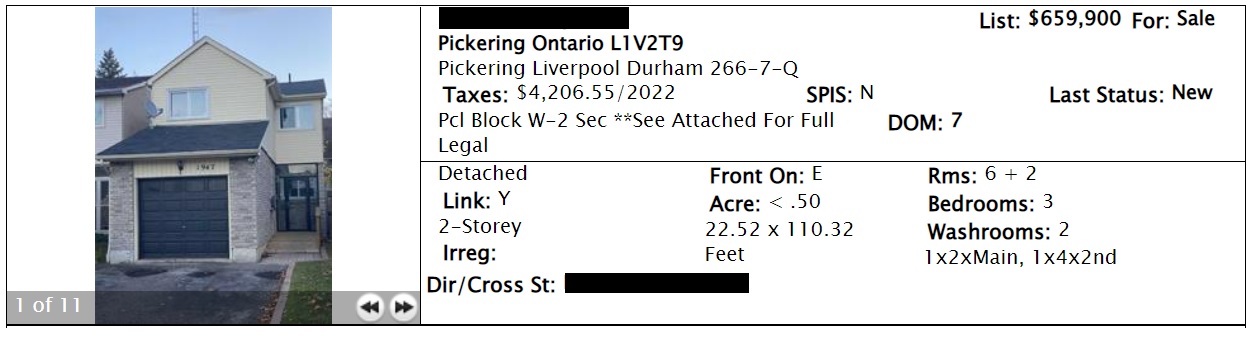

Case in point, this property:

This property was listed for $659,900, which seemed about right, based on the condition of the property and the comparable sales.

This property wasn’t just a “gut” waiting to happen. It was a disaster.

It needed everything.

Define everything? Well, there’s that saying, “….everything but the kitchen sink!”

How about everything including the kitchen sink, and, um, well……….floors?

No, seriously, the house has no floors.

It’s in that kind of shape everywhere.

Now, the comparable sale from the summer – what did it look like, and what did it sell for?

Well, it looked like this:

Oh, would you look at that! Floors!

This property was completely renovated inside and out.

And what did it sell for in the summer?

This:

Working backwards, the gut-reno version of this house is barely worth the list price of $659,000.

So weren’t we surprised when it was listed with an offer date?

Yessir.

Did it get an offer?

Nope.

It got ten offers.

And as of this moment, we don’t know what it sold for.

Anybody care to wager? 🙂

Appraiser

at 8:16 am

After indicating repeatedly that interest rates will continue to rise, it’s almost impossible to conceive that the BOC policy rate will not go up again on December 7.

I’m hoping for 25pbs but fear it will be 50.

As for inflation, I think it will come in lower than last time (will be released at 8:30am).

Those are my wagers.

P.S. I agree, the Prince Edward County story is full of holes.

Appraiser

at 8:49 am

Inflation Report:

Top line number is 6.9% same as last month.

Core inflation (excluding food and energy) is down 1bps from 5.4% to 5.3%.

Average hourly wages rose 5.6%.

https://www150.statcan.gc.ca/n1/daily-quotidien/221116/dq221116a-eng.htm

Francesca

at 8:18 am

We left the suburbs to move back to Toronto in February 2021 and are still here and have no desire to ever live in the suburbs again. Two other residents on our street sold during the pandemic too, one moved to Victoria BC the other to downtown Toronto. I think all the stories about people moving to the suburbs or exurbs was overblown and like the Toronto life article says I bet there are several who did the reverse move like us. We were in fact featured in a March 2021 Toronto life article about this! With people returning to the office in person many will no longer want to commute from the burbs.

I have noticed that a handful of houses that sold when ours did have now resold or are for sale. Is this due to rising interest rates and people who had FOMO then can no longer afford their variable rate mortgages? What’s interesting though is they are actually making a profit in just 1-2 years selling now. It seems like the suburbs may be recovering already in some pockets to maybe not February prices but definitely getting close. I thought the suburban market was dead now but doesn’t appear that way. Maybe lack of inventory is driving prices of few houses for sale up.

Appraiser

at 10:09 am

Think house prices are too high? The rental market is somehow even worse:

“According to data from rental accommodation website Rentals.ca, the average rent in October across Canada was $1,976. That’s an increase of 11.9 per cent, well ahead of Canada’s inflation rate of 6.9 per cent.”

https://www.cbc.ca/news/business/rent-inflation-november-1.6650777

Ace Goodheart

at 10:18 am

$1,905,000.00 for a fully reno’d 3bdrm semi in the Annex is not really a lot of money.

It is actually a pretty good deal. Looks like it had a parking spot too and a backyard, which puts the new owner in the 1% or less of property owners in that area who have those things.

I always thought the way affordability is portrayed in Toronto is wrong.

What folks in the media do, is take a house in a popular neighbourhood, that would fit quite nicely into an episode of “Cribs”, and then determine the affordability by “creating” a notional buyer who:

1. Has no down payment and must save the down payment before she/he can buy and

2. Will make the minimum down payment only and carry the house using a bank mortgage.

The media then says “this house is unaffordable to anyone!”

Well, not really. It is unaffordable to a person who has no down payment, no assets, and must borrow 80% of its value.

But that same house is not for first time buyers. It is a “move up” house. The people buying it likely have equity. They probably have a lot of it. They may go in with 50% down or more. They don’t have to save up 50% down, they already have it.

The media seems to conflate affordability for first time buyers, with affordability for move-up buyers. Sure, a first time buyer is going to buy a condo, and then build equity. When they have some cash, then they move up to a larger condo. Perhaps 10 years’ in, they can sell and buy an actual house. It is a process.

We then hear that “to lower house prices, we need a capital gains tax on principal residences”.

Which would mean that the person who wants to be a move up buyer, can’t do that, as they can’t sell their existing residence. It just locks people in. It is an “asset freeze”. No one can sell as they lose all their equity to taxes.

I watch the argument with so much frustration whenever it is made. Of course a first time buyer can’t afford a $1,905,000 semi in the Annex. That is a “move up” house. To buy that, you’d have to have been in the market already for quite some time. For some reason, the media refuses to see that.

Jennifer

at 1:10 pm

well said.

GinaTO

at 7:08 pm

Haha I was not surprised to see these stories in TL – after running articles on people moving out of the city for a year, now they’ll want to have the reverse. Most of those made me laugh – I mean, you have a downtown lifestyle, and you move to a plot of land far from the amenities you like but still want to see your friends, go to a coffee shop and do trendy things. What did these people expect?? We left TO for the Maritimes and are very happy. That said, we thought long and hard before making the move. These stories, in the end, are not about Toronto or whatever other place they moved to, they’re about lack of planning and misplaced expectations.