A bit of a mortgage-theme here today on TRB, but I had two topics in mind and figured I’d group these together in one post.

First, we have significant competition among the Big-5 banks as they lower variable rates to try to gain more business.

Second, we have the odd listing coming out on MLS advertising vendor take-back mortgages.

This should give the market bears something to rest their hats on…

Who doesn’t love a good rate war, am I right?

My goodness, it’s been so long!

I went through my blog history just now, looking for a specific reference to rate war that I recall from the past, and I was surprised to see that it was actually over four years ago!

Here’s the blog: “Ready, Set, Rate War!”

That was back in March, 2014, when the 5-year, fixed-rate fell below 3.00%.

And within that post, I referenced a Globe & Mail article that couldn’t have possibly been more wrong: “Why Cut-Rate Mortgages Won’t Be Here For Long”

Who knew that rates would go even lower?

Many of you have benefitted from 5-year, fixed-rates as low as, what, 2.39%?

That’s just insane.

And both market bears, and/or the ‘older’ folk, will regale us with stories from yesteryear, when rates were sky-high.

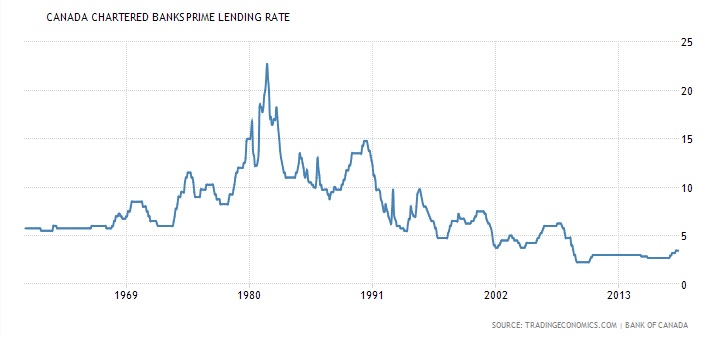

Just to put the interest rate environment into context, let’s take a look at the Prime Rate history from 1960 to today:

Yes, we’ve been in a low interest rate environment for quite some time now. I don’t think that’s in dispute.

And the question that many of you are asking is – how high would rates have to go to really have an effect on the market?

Those 2.29% 5-year rates are long gone!

Rates were up over 3.5% last time I checked. But alas, it seems the banks have other plans!

Cue the 2018 rate war:

From Tuesday’s Financial Post:

TORONTO — TD Bank is joining a rival bank in offering a highly discounted variable mortgage rate as competition among Canada’s biggest lenders heats up.

The Toronto-based bank said Tuesday it’s lowering its five-year variable closed rate to 2.45 per cent, or 1.15 per cent lower than its TD Mortgage Prime rate, until May 31.

TD’s special rate follows last week’s move by the Bank of Montreal, which discounted its variable mortgage rate to 2.45 per cent until the end of May.

Canada’s lenders often offer special spring mortgage rates as home buying activity picks up, but Robert McLister — founder of rate comparison website RateSpy.com — said last week that BMO’s special discounted variable rate was the biggest widely advertised discount ever by a Big Six Canadian bank.

TD’s discounted rate on Tuesday brings its variable mortgage rate offer in line with BMO’s.

1.15% lower than the Prime rate.

Until May 31st, yes. But what if this promotion “works?”

Real estate sales are down across the country, and the GTA is no different, where we’re off 30-something percent so far this year. Banks are in the business of making loans, and suffice it to say, if they can’t make loans, they can’t make money.

Some will argue that sales are down because rates are up.

Others will argue that sales are down because prices are up.

Then, others will suggest that it’s more to do with new mortgage rules, and affordability.

Any which way, the banks need to make more loans, and thus lowering their rates and providing promotions is one way to do that.

This promotion runs until May 31st, but if the banks see their loan numbers increase, this could become a permanent promotion.

It’s not unlike car dealerships, who advertise a different promotion every month, which is essentially the same offering, just packaged under the “New Year” tag one month, the “Valentine’s Day” tag the next month, followed by the “Spring into Spring,” the following month, and so on.

Of course it’s no surprise that once one bank started offering the discount, the others followed.

Who doesn’t love an oligopoly, right?

Now ironically, as this “rate war” is happening with the 5-year closed variable, rates on the 5-year, fixed are increasing!

I’m thinking Robert Frost here…

“Two roads diverged in a narrow wood,” and so on.

From last Wednesday’s National Post:

TORONTO — Canada’s Big Six banks have all increased their benchmark fixed-rate mortgage rate, a move analysts say could trigger a rise in the Bank of Canada’s qualifying mortgage rate as early as Wednesday, making it more difficult for some to take on home loans.

The Bank of Nova Scotia on Tuesday became the last of Canada’s biggest lenders to raise its posted rate for a five-year fixed-rate mortgage — from 5.14 per cent to 5.34 per cent. They also increased the posted rates for other fixed-rate term lengths.

Such rates are different from the actual mortgage rates offered by banks to borrowers, which are not seeing the same increases. But the Bank of Canada uses the posted five-year fixed mortgage rates at Canada’s biggest banks to calculate the rate used in stress tests to determine whether borrowers can qualify for both uninsured and insured mortgages.

And with a rate announcement coming from the Bank of Canada on May 30th, your guess is as good as mine as to where the lending sphere ends up.

Some rates are being slashed, others are being increased.

And all the while, I hear from mortgage brokers that the banks are dying to loan money! They hate the new mortgage rules, they don’t like the restrictions, and that more “promotions” like the 5-year variable closed could be on the horizon.

It would be nice if the Bank of Canada and the Big Five banks worked in tandem, but as we know, they have different agendas.

Now switching gears, when was the last time you heard of a seller offering, or a buyer asking for, a vendor take-back mortgage?

It’s certainly been a while.

As many of the wiser folks know, these used to be common place! Think back to the 80’s – transactions hinged upon what terms the seller was offering!

Here’s a sample listing I dug up from the MLS archives:

That’s from a listing in 1989, where the vendor was offering a $300,000 mortgage at 11.5%, for 1-year, when banks were looking for 13.5%.

It sure made sense if you were a seller.

That property was listed at $739,000.

Let’s say the buyer took the seller up on that $300,000 VTB at 11.5%.

$300,000 at 11.5% is a $4,377.10 per month mortgage payment.

$300,000 at 13.5% is a $4,995.96 per month mortgage payment.

Are the margins for the buyers that thin?

Does that $618.86 per month make or break the transaction for the buyer?

If it does, then the seller is smart to offer this vendor take-back mortgage. The vendor’s opportunity cost is 2% of $300,000, or $6,000. But what if this helps the vendor sell the $739,000 house, versus not sell it at all? Perhaps the vendor can obtain $735,000 for the house, from this buyer, but only $700,000 from a buyer using cash, or bank financing?

Fun times, for those of you who lived through this market.

I’ve never worked in that environment, but I was very interested when I saw this listing the other day:

0% Financing.

A nice way of saying “Free Vendor Take-Back Mortgage!”

Keep in mind, this is the first time I have seen this offered this year, or ever, really. At least in recent memory.

So what are the implications here? Both short-term, and medium-term for those of you who want to draw inferences?

I suppose an optimist would just say, “The seller is offering a discounted rate on part of the financing – which is undetermined, as an incentive, much like throwing in the flat-screen TV in the offer.”

A pessimist would say, “The builder can’t offload the house! The market is weak! He’s offering to finance the house for FREE to get out from under it!”

Given this is the first I’ve seen of this, I would probably lean toward the former.

At the very least, it falls a little bit left of centre.

Plus, as I said, we don’t know anything about the terms and conditions.

How much is the seller offering?

How long is the term?

What qualifications are needed?

Let’s say this is a $3,000,000 house, and the seller is willing to offer a $500,000, 1-year loan at 0%. How much of an incentive is this really?

With variable rates around 2.45%, we’re talking a paltry $12,250 in savings! On a $3 Million house!

But what if it’s a 3-year, fixed rate loan for the balance? What if the buyer could provide the minimum down (20% of the first $1M, and 50% of the balance, for a $1,200,000 down payment), and the seller would finance the rest?

A $1,800,000 loan at 0%, for 3-years.

Say we’re looking at a 3.2% comparable 3-year rate, that’s a $172,800 savings, or more if we’re compounding semi-annually.

All of a sudden, we’re talking meaningful numbers here. $180,000 is nothing to sneeze at, even in the context of a $3M house.

More to the point, what if the buyer wasn’t able to secure bank financing for the balance of $1,800,000, with the $1.2 Million down?

Now not only is the buyer getting a sweet deal in the form of a $180,000 interest savings, but he also gets to buy the house in the first place!

Some of you might be thinking, “Oh great, here we go. A guy who can’t get a bank loan is getting an interest-free loan from the seller, to buy a house he would otherwise not be able to afford? What could go wrong here?”

That’s fair.

But if the buyer and seller want to make a deal, what’s stopping them?

And to be completely honest, I have a hard time believing a buyer with $1.2M down can’t secure financing for a $3M house. Unless that $1.2M is a gift from Mom & Dad, or a drug dealer’s money in cash, these people are probably gainfully employed at salaries that represent their down payments.

Until I see this sort of “promotion” offered in an active MLS listing again, I’m going to consider it a one-off.

But if any of you out there see something to this effect advertised, please email me!

For now, let me open the floodgates to the inevitable interest rate, debt, and risk conversation…

XYZABC

at 9:14 am

Meh on the rate war….this is a, belated and not big enough still, response from these folks to the market.

Rates of prime minus 1.24% have been available from the non-big-bank lenders for some time now. These are not rates from some small monoline lenders either, but the bigger non-bank lenders. And come with 20/20 prepayment privileges, and to top it if you have to break the mortgage for any reason, the penalty is going to be lower when compared to the big banks.

When it comes to commodities, money is the most commoditized item of them all….

XYZABC

at 9:16 am

I don’t think i got the discount off the prime rate right. If the calculation was to be correct you would end up with a variable rate of 2.21% with a good lender.

craijiji

at 11:30 am

Seriously. I got Prime -1.25% five months ago on a 5 yr variable. This isn’t new, maybe to the big 5 banks, but not to people who actively shop for their mortgage as opposed to just strolling into their branch and signing some paperwork.

Housing Bear

at 3:19 pm

Ahhh now I see why you are so defensive. Enjoy that debt trap bud!

craijiji

at 3:22 pm

I’m not defensive at all, I see benefits to both variable and fixed. I’m ok with the downsides of the variable rate mortgage I have because I know that I’ll most likely win out in the end in comparison to the fixed rate I could have signed.

When you learn what the difference between an open and closed mortgage is, then you can come back at me. Bud.

Ralph Cramdown

at 9:30 am

“Just Completed!” = staged and on the market for 15 months through a 25% price drop and a change in brokers. 0% = the power of FREE.

First, mention of a Robert G. Allen book, now a VTB sighting on MLS. What’s next out of the tickle trunk, David, Hammertime videos?

Housing Bear

at 11:36 am

VTBs can actually make some sense if the market starts to really decline.

I view variable closed at record low discounts to be the ultimate debt trap. Payments do not incease if rates do but rather get added to the term of you mortgage. 100 bps increase would result in you being on the hook for approximately an additional 3 years.

BOC has indicated that they plan to raise their rate to neutral, which they define as somewhere between 2.5-3.5%, unless of course the economy breaks before then. So that implies anywhere from a 1.25%-2.25% raise over the common years.

Buy a, 25yr variable closed at 2.5% today. Rates go up 100bps. In 5 years from now you have to renew 23yrs at at least 3.5% (assuming record discount still holds)

If rates go up 200bps then in 5 years that 25yr – 2.5% is getting renewed at 26yrs – 3.5%(or higher).

I think BOC should now raise in May, to stop fools from jumping into this.

XYZABC

at 1:18 pm

Depends on how quickly the rates go up, and how much do you use 20/20 (or even 5/5) privileges.

The fixed to variable decision isnt one you take based solely on how much you thinks the rates will go up; its a question of timing, prepaying, and the spread between fixed and variable. If the spread is around 0.8% (which it is now), that means it will take three+ increases before you start paying the fixed rate of today….

what does your crystal ball say on when each of those three increases will go into place…

XYZABC

at 1:26 pm

Why dont we have an edit button here…???

The spread is actually >1% from the lowest variable to lowest fix; so 4+ increases needed to get your variable rate to be same as today’s lowest fixed rate.

Housing bear

at 1:51 pm

Variable closed is what I am talking about. Payments don’t go up. Your term gets extended. My point being that this type of loan can have you in debt for a lot longer then most wouldnthink. In more extreme scenario could have you renewing at a long duration and at a higher rate the the terms you first took the mortgage at. I personally do see this as a last ditch effort by big banks to get as many people trapped as possible

That being said, I expect 1 hike in May or July followed by another in the fall. No crystal ball, just pay a lot of attention to what the BOC is saying. Could things change? Sure.

craijiji

at 2:36 pm

I’m convinced you don’t really know what you’re talking about. The differences between an open and closed mortgage are: lower interest rates associated with closed mortgages, and penalties when paying it off early. The end.

Also, your whole thing about the term getting extended…where are you getting this from? Sure, your payments remain constant but all that happens is you pay less towards principle. Are you talking about the equivalent of being on the hook for a longer term? Maybe I’m missing something, but from what I’m reading you’re not making a whole lot of sense.

Geoff

at 3:06 pm

First craijiji, take it easy.

Second, I thought that lower interest rates are associated with variable rate mortgages, versus fixed. Third, I believe that the ‘term’ being referred to is in fact the amortization period, not the term of the loan (stop being so literal). So on a variable, as interest rates adjust your payments don’t, but the portion going to interest does — which in fact means the amortization period is extended.

Housing bear

at 3:11 pm

Your payments stay the same with closed even if rates move up or down. At least with the great deal TD and BMO are offering right now.

If rates go up, more of your monthly payment goes to interest, less to principle. Is this just a a loss the bank takes to do you a favour? No

When you renew less of your principle has been paid down if rates are higher vs had they stayed the same (you win if rates go down). The difference in paid down principle works out to about 3 years of payments per 100 basis point increase.

My way of spelling out the effects above is so that average joes like you realize what you’re signing up for

craijiji

at 3:14 pm

Nah I’m good. Thanks for the suggestion though.

Amortization period doesn’t mean term, so if he meant amortization period he should have wrote that. If you’re going to come on a blog and try to sound like an authority, be prepared to get called out if you don’t make any sense. It’s not up to me to try and figure out what he’s talking about when he’s using terms that mean something totally different interchangeably, especially when both terms are related to the subject matter.

craijiji

at 3:18 pm

@Housing Bear. That’s not what a closed mortgage is dude. All you’re talking about is a variable rate mortgage, it being open or closed has no bearing on the payments remaining constant. You’re trying to spell it out for Average Joes like me, but you don’t know what you’re talking about. Maybe you should read up on mortgage terms, unless you want the Average Joe to school you some more?

Housing Bear

at 3:31 pm

Variable open will generally allow you to keep payments the same, but you can increase them or jump to fixed whenever you want. Variable closed you are trapped. Much harder to switch out of. Rates move up and your just going to fall further and further behind on your principal…………. Debt trap. When you go to renew 5 years from now you may find that your payments have skyrocketed and you have made zero ground on your principal. Why do you think the crazy discounts are only be offered on the closed rate variables right now?

If thats the only thing you can afford. Probably best to wait it out on the sidelines.

Housing Bear

at 3:37 pm

AKA you take a 500k loan today at 2.5%. 5 years from now your are looking at 500k outstanding, and are faced with a higher rate.

craijiji

at 3:39 pm

Once again, whether it is open or closed has no bearing on the payments. It dictates whether the loan is open which means it can be paid off at ANY time during the term with no penalties; or closed which means that there are penalties (either 3 months interest or the IRD) for breaking it early.

My variable rate is closed, however, I can prepay 20% annually and/or increase my payments by 20%.

Housing Bear

at 3:45 pm

If you can increase payments on your variable Closed by 20% at will with no penalties, then I have misunderstood how that works.

craijiji

at 3:53 pm

Ya, I think we’ve established that you’re not quite sure what the difference between and open/closed mortgage is.

Housing Bear

at 4:08 pm

I always went fixed before, which turned out to be a losing strategy between 2009-2017. Not a mortgage broker and will be paying cash for my next property……… Shouldn’t comment on that I guess, looks like you got me. Still think jumping into a record discounted rate is a mistake (unless you can afford to bail yourself out via higher payments or lump sum.)

Just thank god it was on this blog that i embarrassed myself.

craijiji

at 4:10 pm

Let me know if you want me to explain to you how it’s virtually impossible to take out a $500K mortgage today, and still have $500K outstanding when you renew. That’s a whole other can of worms which really makes me question your knowledge.

Housing Bear

at 4:23 pm

Please do. I believe your payments do increase if the rate jumps to a level where you wouldn’t even be covering interest.

Please walk me through the numbers if I were to take a 500k mortgage today (variable closed or fixed) , within a year rates are 2% higher. (not likely but as an extreme) What will my principal be upon renewal 5 years from today?

Libertarian

at 4:25 pm

I acknowledge that Housing Bear has some details wrong, but his basic idea that increasing rates will extend the length of time needed to pay off your mortgage is accurate. At least, that makes sense to me – more of your payment goes to interest than principal, so you’ll need to make more payments.

Isn’t TD known for screwing over clients? So doesn’t this offer fit in with that theme?

Daniel

at 5:26 pm

you could just overpay the mortgage (almost all of them have some feature that allows this) while rates are low at the beginning. Even if rates rise you may have gotten far enough ahead in the early days to offset the pain if rates rise.

no protection against an immediate and drastic spike in rates. That said, if you’re confident that’s whats going to happen then maybe you should just be renting anyway.

craijiji

at 8:10 am

@Housing Bear – even if your rate jumped 2% per year, from 2.5% in year one up to 10.5% in year five, you’d still pay approximately $50k off of the principal in a five year term.

Geoff

at 8:20 am

@ craijiji

RE your comment that “Amortization period doesn’t mean term, so if he meant amortization period he should have wrote that.”

Though I believe you understood what he meant, most likely. Just as everyone here understood that when you wrote “Sure, your payments remain constant but all that happens is you pay less towards principle.” that you meant ‘principal’ as in the amount of the loan that remains outstanding, and not principle as in a fundamental belief.

But if you believed in your own principles, then you wouldn’t have written principle, would you?

craijiji

at 11:45 am

@Geoff – I’m pretty sure there’s a difference between a small spelling error due to autocorrect on my phone and using a totally incorrect term. Keep reaching though.

Housing bear

at 6:18 pm

Your total payment would more than double if rates went from 2.5 to 10.5. (Increase is all interest). Safe to assume no principal is being repaid under that scenario.

Yes because your early payments would include principal you would not end up exactly at 500k (unless they jumped the day after you signed)Not sure the exact breaking point. But what happens if rates rise to a level during your term where all your payments equal out to interest only. No principle being repaid at all.

What happens if rates go up to a point where your payments would not even equal interest (like your 2.5 to 10.5 example)………….. payments jump or margin call.

In either case it has debt trap written all over it when by all indications today rates will continue to increase

craijiji

at 1:19 pm

If your payments fluctuate (which wasn’t what we talked about originally), and rates jumped from 2.5% to 10.5% (adding 2% per year on the anniversary date), payments would increase from $2,243/month to $4,721/month. Obviously massive in terms of the increase. However, you’d still pay off about $50k in principle during this time. even with rates at 10.5% and payments at $4,721, you’re chipping away at a rate of about $550/month.

To put things into perspective, if rates increased 10% per year (year five rate of 42.5%), you’d still pay off close to $20K in principle due to year one and two. By the end, your payments would be astronomical at close to $18K/month, while paying off about $3/month on the principle.

joel

at 3:05 pm

That is an adjustable rate mortgage and in Canada most mortgages that are called variable will go up in payments. There are very few that actually extend the amortization and keep the payment the same. This is a huge difference between mortgages in Canada and the US.

XYZABC

at 4:11 pm

Yeah, Bear is completely off on this. Confused about what is what.

joel

at 3:08 pm

I have seen a few of the vendor take back mortgages from builders, but mainly in condos. They are using them as a sales incentive, but after the 1 year is up the rates go way up. Last client I dealt with that had one was at a rate of 4.99% the day the year expired.

Appraiser

at 7:52 am

Looks like someone (‘Bitter’ Dwelling) wasn’t looking at the whole picture regarding Toronto.

“Millennials, on net, are coming in droves, at least lately.”

Brain DePratto, TD Economics, May, 16, 2018. https://twitter.com/BrianDePratto

Chris

at 8:05 am

The Better Dwelling article from the other day was clearly discussing intraprovincial migration. Hence the headline including the term “local millennials”. You can question how relevant intraprovincial migration is when compared to overall migration. That’s fair. But don’t try to make it out like it was misleading. They clearly stated what they were analyzing, and explained intraprovincial migration for anyone who didn’t understand.

By the way, even Laurin Jeffrey, a local agent and big time market bull, thinks you’re dumb if your properties are cash flow negative.

https://twitter.com/condoloft/status/996727960890740738?s=21

Didn’t you say you bought a place to rent out recently, appraiser? What’s the cash flow like on that one?

Appraiser

at 9:09 am

You do know what “whole picture” means, don’t you?

Chris

at 9:16 am

The article clearly states that it is discussing net intraprovincial migration. It even explains this concept, and differentiates it from total migration.

So yes, they make it abundantly clear that they are not looking at the whole picture, but rather a subset. Hence your attempt at a “gotcha!” really falls flat.

Keep swinging, bud.

Appraiser

at 9:11 am

Direct quote from Laurin Jeffrey: ” If you buy to hold and rent, you are an investor, or landlord. But not a speculator.”

Nice cherry-picking dumbass.

Chris

at 9:13 am

“But those who buy & have negative cash flow… they’re mainly dumb.”

What’s the cash flow situation of your latest property, appraiser?

Kyle

at 10:18 am

BetterDwelling is classic fake news. Time and again there is a very clear pattern of them taking some piece of data and making it out to be something it isn’t. With a title like “See Ya! Local Millennials Are Abandoning Toronto And Vancouver”, it is very clear that they are trying to paint a picture that the millenial population is shrinking in Toronto and Vancouver, when in fact the millenial populations in those cities is growing.

Any suggestion that a reader should understand that they aren’t talking about the whole picture and are only talking about the intraprovincial aspect is weak and apologist at best.

Chris

at 10:31 am

Intraprovincial migration is explained in the second paragraph, before the article discusses the data. The article also states that this measurement is distinct from immigration.

If someone were to only read the headline and nothing more, then yes, there’s a chance they won’t understand that Better Dwelling are talking only about the intraprovincial aspect.

If they read the article, however, they should at very least have a cursory understanding of intraprovincial migration, and recognize that this is the statistic the article is discussing; not total migration.

Kyle

at 10:42 am

So at the very least can you admit the title is totally misleading and an outright lie?

Honest question, do you think Tommy who quoted the article, came away thinking the millennial population could be expanding in Vancouver and Toronto?

Chris

at 10:52 am

I think the title is purposefully inflammatory, likely in an effort to garner clicks. While they do qualify that it is “local millennials”, thus alluding to the intraprovincial aspect of migration, they have definitely taken some liberties in the headline. A more neutral headline would have been something along the lines of “Intraprovincial migration statistics show higher numbers of millennials leaving Toronto for other parts of Ontario. Doesn’t quite grab the attention as much though, does it? Plus, we both know that Better Dwelling is not a neutral source. They have a slant to their articles, just like Ben Myers has a slant to his, and you and I have slants to our comments. But, I see value in reading all of them, to get differing opinions.

As for Tommy, I’m not sure what he thinks. If he read only the headline, then yes, he may have missed the fact that the article was discussing intraprovincial migration exclusively. But, in his post, all he stated was that this was “another not so positive trend”. Doesn’t shed a whole lot of light on how much of the article he read, or his level of understanding of intraprovincial compared to total migration.

Kyle

at 12:10 pm

BetterDwelling’s slant is a whole different order of magnitude, and not even in the same realm as anything Ben Myers has ever imparted. So making that kind of comparison is totally disingenuous. As much as you despise him, Ben Myers, has never made a completely false statement, backed only by some minor factor, knowing the other major factors outweigh and contradict his statement. For BetterDwelling that’s their whole business model.

Your need to immediately add qualifiers when i post Zolo data because you don’t like how bullish they look stands in very stark contrast to the amount of leeway and license you give to BetterDwelling when they purposefully put out misleading articles that support bear narratives. I find it funny that on one hand you feel it so necessary to immediately warn people that the real time zolo data may not capture every transaction, and therefore could be subject to change, but on other hand you feel people should just know that BetterDwelling is only talking about Intraprovincial migration and not total migration, despite their headline falsely claiming total population is shrinking.

Chris

at 12:42 pm

I never said I despise Ben Myers. I disagree with some things he postulates. Yet I think he’s worth reading to see different opinions. And just because I don’t agree with him, doesn’t mean I hate him. It’s odd that you seem to equate those two things.

I also never said that I expect people “should just know that BetterDwelling is only talking about Intraprovincial migration”. I said they should read the article, where it is explained, rather than just reading the admittedly inflammatory headline. That being said, the headline also doesn’t claim that total population is decreasing, so I’m not sure where you gleaned that from?

Finally, yes, I focus on things that bolster my position. Just like you, appraiser, tommy, housingbear, etc. Notice how appraiser only posts bullish tweets and articles? Notice how housingbear hasn’t brought up the increase in condo prices? Why weren’t you posting zolo graphs around this time last year when prices were sliding across the GTA? Funny that you seem to take exception to it in this one particular instance.

Kyle

at 1:57 pm

Perhaps this is where i got the impression you despise him….

Chris said:

“You mean Ben Myers who works in marketing for Fortress, the real estate developer? The same Ben Myers who has a B.A. in economics from a low ranking American college? The same Ben Myers who regularly contributes to the Huffington Post, BuzzBuzz Home, The Toronto Sun, and other lackluster publications?

Ya, I don’t think I’ll be placing much weight on his opinion. You would be wise not to either. “

Chris

at 2:07 pm

Exactly. I frequently disagree with his opinions, and find his recent employment with Fortress Real Developments concerning, particularly after the involvement of the RCMP in investigating syndicated mortgage fraud with the company.

But I certainly don’t hate or despise him. I’ve never met the guy. He could be a perfectly nice person?

Just because I disagree with someone, doesn’t mean I hate them. For your sake, I hope you’re also able to draw a distinction between the two.

Ben Myers

at 2:53 pm

I am a nice guy by the way.

Condodweller

at 1:50 pm

“And the question that many of you are asking is – how high would rates have to go to really have an effect on the market?”

I’m surprised nobody has analyzed the prime rate graph. I thought housing bear would have been all over this based on his situation and recent posts.

I think it’s a worthwhile exercise for anyone with a stake in the RE market to overlay this historical rate graph with the historical RE price graph that was posted recently. The first thing that jumps out for me is that both market tops in terms of price were preceded by several years of interest rate increase in the magnitude of about 5%. Those who think this can’t happen need to keep in mind that it has happened about 6 or 7 times in this chart. Another fact to keep in mind is that the average RE price deviation from the mean is much higher than during either of the past two market peaks which suggests to me that we would not need as much as a 5% increase in rates to set a market peak this time around. Given that mortgage amounts are significantly higher today would also reaffirm this theory. It is also interesting to note that the government stress test of 2% above current rates seems to be right on the mark and if anything it may be too conservative.

In any case, it would not be a horrible idea for people to use a 4-5% rate increase over 5 years as the worst case scenario of their risk analysis. Those in variable rates will feel the immediate impact of increasing rates, however, those who took out a 5 year fixed recently might be in for the shock of their life at renewal.

Considering that prices are at record high and interest rates are at record low, there is a lot of room in the other direction for both.

Chris

at 1:59 pm

Two Globe articles from the other day:

https://www.theglobeandmail.com/investing/investment-ideas/article-us-10-year-yield-hovers-near-7-year-peak-after-bond-sell-off/

https://www.theglobeandmail.com/investing/investment-ideas/article-rising-us-yields-clip-bank-of-canadas-control-over-borrowing-costs/

Housing bear

at 6:26 pm

Ive tried to point that out, all falls back to my main thesis that it will be thebcredit cucle that does is in. I’ve shared that graph before to show that the interest rate manipulation over the past decade is unprecedented. Have also pointed out that all assets which are dependant on financing rise and fall inversely to rates. Once defaults pick up banks raise rates further to offset loan loss. Becomes a vicious cycle, especially when a large chunk of your economy is tied to the health and growth of the real estate market

Housing bear

at 6:29 pm

I only think our rates would jump that high though if inflation starts to really take over. That’s the big thing I’m watching today

Kyle

at 2:12 pm

“Finally, yes, I focus on things that bolster my position. Just like you, appraiser, tommy, housingbear, etc. Notice how appraiser only posts bullish tweets and articles? Notice how housingbear hasn’t brought up the increase in condo prices? Why weren’t you posting zolo graphs around this time last year when prices were sliding across the GTA?”

Again you make another disingenuous comparison. There’s a massive difference between a bull not posting something bearish (or a bear not posting something bullish) vs what you do. You literally frantically search for the the tiniest black lining in and then try to hold that out as some sort of rebuttal when someone makes a majorly substantive bullish point. Or you post/defend/make excuses for “articles” that are pure narrative pieces which usually end up being debunked garbage. None of the other commenters do this, just you. As much as you pretend, it’s never been about debate or discussion with you, it’s flat out dogma.

You are a fundamentalist bear and every time Appraiser blows a massive hole in one of these bear articles, your persistent attacks on him, just show what a hardcore fundamentalist bear you are.

Chris

at 2:56 pm

Yawn. Your entire second paragraph is just you rehashing your opinion yet again. We get it, dude. In your mind, I’m some big mean ol’ bear spouting dogma and loving bear theories or whatever, and you are a nice neutral balanced commentator. That’s swell. You go right on believing whatever you want. I will continue disagreeing with your opinion, and posting whatever I damn well please. You’re welcome to ignore or comment on my posts as you see fit.

As for appraiser, guy’s a troll, plain and simple. Swearing and insulting others when they disagree with him. Feel free to scroll down to the latest example where he cherry picks a quote, then calls me a “cherry picking dumbass”. But sure, I’m the one attacking him…ok there bud, whatever you say! I must just be lashing out because of all those times he blew holes in my arguments, right? Or maybe I’m still upset about him telling me to clean my room? Boy, good thing we have him to provide such quality content!

Kyle

at 3:26 pm

If you have something substantive to rebut with then by all means post away. But the true yawns should be saved for every single time you feel compelled to immediately bury all substantive arguments in an avalanche of your cheap ones.

Actually when i scroll below what i see is:

– Appraiser showing evidence that the BetterDwelling “article” is misleading (was there ever any doubt?). Not directing anything at you in anyway.

– You immediately making a sad excuse for BetterDwelling, then taking a personal jab at his investment property.

Chris

at 3:33 pm

Nah, I’ll keep on yawning at you and your constant whinging. “You’ve never met a bearish opinion you don’t love!!!” and all that tripe. Don’t care. If you don’t like my posts, ignore them. Quit your bitching and crying.

Ah, now making sad excuses for your troll buddy, eh? We’ve been over this already man. The Better Dwelling article clearly states it wasn’t looking at the whole migration picture. If you and your troll can’t figure that out, then you two must be illiterate.

I made no personal jabs. I said a local realtor called cash flow negative rental investors dumb. That’s the quote, click the link for yourself. Then I asked about appraiser’s cash flow. To which he responded by calling me a dumbass. Still waiting to find out if he’s cash flow positive or negative on that one! Only crickets so far…

But sure Kyle hahaha I’m the one taking personal jabs. Whatever you say buddy! You and appraiser are saints hahaha. Cheers pal.

jeff316

at 3:35 pm

Prodding someone unnecessarily and unrelated on their property detracts from your points. Posts like this just make people ignore you.

Chris

at 3:40 pm

It’s a simple question. Cash flow positive or negative. Hell, he could have even said he didn’t want to answer. But instead, he cherry picked a quote, then called me a “cherry picking dumbass” haha talk about hypocrisy.

Odd how you find that off-putting, yet seem alright with the insults, swearing, personal attacks, etc. But feel free to ignore my posts if you’re suitably offended. It’s no skin off my back buddy.

Kyle

at 3:42 pm

Chris, you can keep on posting your flimsy weak arguments, and trying to shout down others, and bury their points with ridiculously cheap comebacks. Frankly i’d expect nothing less from a fundamentalist.

And i’ll keep on calling out your hypocrisy of your cheap one-sided arguments. Hey try taking some of your own advice, if you don’t like it don’t read it, pal.

Chris

at 3:50 pm

“Flimsy weak arguments”, “ridiculously cheap comebacks”, “cheap one-sided arguments”. All your opinion. Zero fact. What’s that saying about opinions, again?

And nah, I’ll keep reading so I can keep on calling you out on your fact-less whining and defense of your hypocrite troll-buddy. Sorry!

Kyle

at 3:55 pm

“The Better Dwelling article clearly states it wasn’t looking at the whole migration picture. If you and your troll can’t figure that out, then you two must be illiterate.”

WEAK A.F. This would be like defending an article that claimed Diet Pepsi as being healthier than milk because it has less calories. As long as the article included the definition of what calories are. If you can’t understand that analogy then you must be a fundamentalist.

Chris

at 4:08 pm

“WEAK A.F”

Oh wow, you capitalized it? Welp, now you’ve convinced me of your opinion!

The article’s second sentence clearly states “Statistics Canada’s latest intraprovincial migration numbers…”. It then goes on to discuss this, and how it is distinct from total migration. I don’t know how to make this any more clear to you? If you want to take umbrage with the headline, go right ahead; as I said, it is inflammatory.

But you and appraiser are crying up and down about how the article doesn’t look at the whole picture? Ya, no shit guys. It says that. Pretty clearly.

To take your straw man example, it’s as if an article said “Diet Pepsi has less calories than milk!”, then explained that calories are not the sole determining factor in “healthiness”. Then you come out whining that the article didn’t look at the whole picture of healthiness between the drinks. No shit. It was looking at calories. It clearly said so.

Kyle

at 4:17 pm

No one believes that when YOU first read that article, that you didn’t also think that the population of millennials was decreasing, just like Tommy who quoted it and probably the vast majority of other people who read it. Your argument about them defining or qualifying is nothing more than apriori horseshit, bud.

Chris

at 4:28 pm

Boy, you sure are able to glean a lot about Tommy’s thoughts, based on his simple quote saying “another not so positive trend”.

And now you’re able to peer into my head as well, huh? Very impressive stuff, Kyle! You’re absolutely right, I read only the headline, assumed that it meant millennials were streaming out of the city at a torrid pace, and then grabbed my bell and sandwich board so I could hit the streets, spread the news and single-handedly bring down the market!

You know, the sad part is, you and appraiser could have legitimately questioned the article, and it’s insistence that intraprovincial migration is as important as total migration. I’m not even convinced of that one myself; sure, some millennials may be leaving to other places in Ontario, but if far more are coming in from other places, the impact is likely outweighed.

But instead, you two decided to choose the “whole picture” argument as the hill to die on. Which again, no shit the article isn’t discussing the whole picture of total migration. If you read two sentences, that becomes abundantly clear.

Kyle

at 4:36 pm

That’s ok, i knew you weren’t going to be honest and admit it and instead stay silent on it and hide behind sarcasm. But you should at least be honest with yourself….That is if your dogma will let you do that

Chris

at 4:42 pm

You got me dead to rights, Kyle! Kudos! Boy you and appraiser are amazing, calling me out on my messy room, my mom’s basement, and my thought entire process! How did you guys know??

Natrx

at 4:05 pm

My variable mortgage rollsover this year. Whew, good to know I can stick with Variable.

Housing bear

at 6:49 pm

@kyle @ shanker

Believe it was the two of you who were debating with me about the weight of housing on our GDP.

https://www.macleans.ca/economy/how-real-estate-feeds-the-canadian-economy/

Good little video that touches on a few of the points I was covering. Whether an extended period of flat prices would trigger a recession or not is still debatable. I think it would because it would kill a lot of investment. But let me know your thoughts

Kyle

at 9:45 pm

Like i’ve said before anyone can come up with a bunch of hypotheticals (both bullish or bearish). Doesn’t take much other than an imagination. That is all the guy in the video manages to do (and none of his hypotheticals are new or ground breaking to any of us). But also like i’ve said before what it comes down to is probability and sensitivity.

Here’s my take:

Strong pre-sales over the last couple of years, basically locks in Construction jobs for the next 4 to 5 years, so probability of much pull back here is low. Construction workers generally have not been the ones buying up Toronto real estate, some maybe, but i would definitely not say the majority. So even if there were a pull back in this area in my view real estate spending sensitivity is low.

If activity doesn’t rebound, then mortgage activity will be slower vs recent years, so probability of some pull back here is in my view moderate, but again i don’t think it’s the PBRs at the bank branches that have been buying up Toronto real estate, so again i think the sensitivity here is low.

Realtors, Lawyers, Inspectors etc will also probably see some slowing of activity, and yes i do think the successful ones have actually been buying up Toronto real estate, but only the successful ones. From David’s assessment of how many transaction most Agents actually do in a year, the actual number of people affected is only a small percentage of the total number people gainfully employed in these jobs. So i don’t think this is going to have that big an effect.

Kyle

at 10:13 pm

Not to mention if any of these things do actually start to impact the economy severely, that will likely cause the BoC to stop or cut rates again.

Housing bear

at 10:45 pm

It could cause them to stop or cut provided inflation is not being imported to us via the US

Housing bear

at 10:55 pm

And we are already in a recession at that point anyway. Banks don’t lend as much suiting a recession. Recession + bad debt = worse recession = more bad debt.

Kyle

at 11:16 pm

I disagree with this idea that the only time the BoC will stop raising is if we are already in a recession. Not sure where you’re coming up with that. If GDP is growing at less than 2% and there is no specter of inflation they are not going to blindly keep raising just to get to some neutral band.

Housing bear

at 11:42 pm

Will at least raise until it is evident we are headed for a recession. I’m getting that from the fact we follow the fed unless something extreme is in the works, NAFTA getting torn up could do that, plus the BOC will want to get rates to a level that they could make an effective cut from to stimulate the next bull run. Can’t say that for sure and neither can you. Will probably find out pretty soon though. Canadian bond yield just inverted for the first time since 2007 (strong indication of a coming recession) we will see what the BOC does with rates over the next few months

Housing bear

at 12:11 am

Partial inversion I should add. Only 10 yr crossed 30. Full inversion would imply expectation of rates going down in the future. Let’s see if BOC gets cautious, I bet the pull trigger July latest

Housing bear

at 10:42 pm

Wouldn’t call 20% of gdp a hypothetical. Think he does highlight a lot of the industries attached to this.

I agree high rise construction sector has enough worked lined up for next few years. Ones tied to house flipping not so much.

20% of gdp does not mean 20% of those employed, but does account for a lot of the money going around in our economy. Think it’s safe to assume that some construction workers and bank reps own their own properties, I know a few with multiple. Then there is just the broader effect of impacted groups not spending money on other areas of the economy. Restaurants, trips, cars etc.

You highlight the most exposed group. I am not arguing that these people will have to dump their properties and then their will be a recession. I’m arguing that we are on our way to a recession (next 8-12 months), and depending on how much bad debt it out there, bunch of those groups might then have to liquidate.

In regards to prices, even if the bulk of properties bought recently are owned by wealthy people, and those people can weather a recession, I still expect them to decline somewhat simply do to the fact the money supply is being tightened and the next wave of buyers will not be able to borrow enough to pay more for a home then recent buyers did. As the credit cycle continues to turn, if we find out a bunch of those “wealthy”people have bad debts and can’t handle a recession than it could be very ugly for prices, and our economy as a whole. That’s a hypothetical, but we have already started to hear some stories about bus drivers, massage therapists and even real estate agents who have been burned in the last year. Me thinks there is a ton of bad debt out there

Kyle

at 11:31 pm

I”ve been hearing those stories about the taxi driver or hairdresser that owns 3 houses for decades now. IMO, those are largely urban legends from the bear echo chambers. I’ve lived in the core of the City and followed real estate all through the run up since my first purchase in the early 2000’s, and the people i see buying in Toronto are white collar power couples. They come from Finance, Law, Consulting, IT, Business, Marketing, Asset Management, and whole bunch of other diversified industries that will largely go unscathed by any stall or slow down in real estate. Now if there was a recession that took out all the Finance professionals and Lawyers in this City, then yeah i could see a crash coming, but the yarn spun by the guy in the video simply doesn’t convince me.

Housing bear

at 11:49 pm

A bunch of those industries are tied to Real Estate.

Bus driver story from April

https://www.thestar.com/amp/business/2018/04/04/they-bought-their-prebuilt-homes-at-the-markets-peak-now-they-face-financial-ruin.html

Also from April

https://www.macleans.ca/news/canada/the-wake-up-call-for-a-generation-of-wide-eyed-home-buyers/

Hey one from May!

https://www.google.ca/amp/www.macleans.ca/economy/realestateeconomy/toronto-real-estate-losses/amp/

Meet John

John works as a RE agent

John likes to speculate on property and doesn’t worry about debt

Now John is broke

Don’t be like John

Kyle

at 9:04 am

I wouldn’t put too much stock in those “articles”. Those are exceptional cases, but they get lots of media, because they resonate with reader’s emotions. I have seen over social media lots of “Journalists” and writers casting a net asking for people who have been affected by the changing market. David who is often approached by writers, has often revealed how the sausage is made, for stories like the ones you’ve linked to.

It was Appraiser who actually put things in to perspective when he took John Pasalis’ numbers of adversely affected transactions into context to the total number of transactions. That percentage was largely immaterial to the whole market.

Chris

at 9:39 am

“Last year there were 92,286 sales on MLS. “According to real estate brokerage Realosophy Realty, at least 988 households were directly affected by a sudden drop in Greater Toronto Area home prices last year.” WOW! That represent slightly more than 1% of all transactions. What an absolute tragedy!”

– appraiser

“Combined, these 988 properties lost a total of $135 million in market value in 135 days – the average number of days between the first and second sale for all these transactions.

This is likely a small subset of the transactions that failed to close in 2017. Our analysis found another 1,784 properties that were sold in 2017 that were subsequently listed for sale either in the same year or during the first quarter of 2018 and did not sell. We did not go through the process of evaluating these transactions individually to see what proportion of these listings were listings for transactions that had fallen through vs transactions where the buyer took possession but for some reason decided to list their house for sale shortly after taking possession.”

– John Pasalis

2,772/92,286 = 3.0%

Immaterial? Maybe. More material than 1%? Definitely.

Housing bear

at 11:08 pm

Here my bull argument and what I’m looking out for to determine if I should jump back into the market sooner than my plan.

Condos put a floor on how far prices can fall. They have been holding up and showing growth. The gap between condos and sfh is declining. Eventually those with equity in their condos will either trade up or will pull equity out to get into sfh, that will cause a spike in demand for sfh. Downsizing boomers who are now able to get their liquidity combined with the next wave of first timers will maintain enough demand in the condo sector so that this market doesn’t get flooded when those mentioned above try to move up. B20 didn’t come out too late. We have plenty of time for bad debt owners to sell to those who have been stress tested and are financially sound.

Kyle

at 11:56 pm

Here is my bull thesis and what i would consider a signal to jump back in, if i were in your shoes.

Just before the Fair housing plan was announced there was a butt load of real living breathing demand actively putting in multiple offers on a record low inventory. Which caused the insane price increases. Then after the rules changed all of that demand got scared to the sidelines, i highly doubt that any of these people have suddenly changed their mind about owning, as surveys about home buying intentions continue to show, that the vast majority still want to and expect to own in the near future. So this sideline waiting IMO is temporary only. The only thing holding them from jumping back in is uncertainty on where prices are going.

Now some of those sideline sitters will be weeded out by the the new mortgage rules, but the remaining pool has also been building up since people haven’t been buying (like if you dam up a river, it starts to build up pressure). If prices give a clear recovery signal, and supply doesn’t increase to match, then prices once again have no where to go but up.

If i am right, the price drop we saw last year is only temporary and will reverse. Just like what happened in Vancouver. So i would closely watch each month’s y/y. If it keeps improving (which we’ve been seeing) and then switches back to black, we will see fence sitters become active once again. And potentially could have a dam breaking effect if inventory doesn’t rise in response.

Housing bear

at 12:21 am

I agree there are a lot of people on the sidelines that are waiting to see what happens. I just think you are highly underestimating B20. I was expecting to see higher sales in the last few months due to people with pre approvals from before January 1st. About 20% removed from anyone’s max borrowing power ( there are creative ways to make up the difference)

Vancouver had a turn around but larger homes still languished and now sales have fallen off a cliff. Most of the strength they had was also in condos. Condo pre sales were still selling at 94% in January of this year but it then started dropping month over month and for April only 43% sold.

https://biv.com/article/2018/05/realtors-developers-brace-crash

Kyle

at 9:28 am

While not quite the top end of the market (especially compared to Vancouver), i have noticed WAY, WAY more houses in the $2M – $3M range selling in the last couple of weeks, and they are selling fast. If you go on Mongohouse and check the last 7 days for Toronto South of Lawrence, the Super-prime neighbourhoods that were frozen are starting to thaw (with the exception of Forest Hill).

And the Downtown neighbourhoods are starting to really heat up. I’m seeing renovated houses basically are going for well over $1000+ /sq ft now, even Semis/towns.

Some people claim that i am a bull, but even i am mind-blown by some of these sales in the last 7 days:

54 Gelndonwynne Rd Sold for $2.05M

385 Wellesley St E Sold for $2M

83 Willcocks St Sold for $3.06M

39 Sharon Dr Sold for $1.73M

703 Shaw St Sold for $2.05M

I don’t think anyone can honestly tell me those sales prices would have been below last years’ peak. Will be interesting to see how May ends up. And unlike last year where the Spring market was basically extinguished by the Fair Housing Plan mid April, This year it will likely keep running right into June.

Chris

at 9:55 am

Recent years of strong appreciation likely encouraged investors to jump into the market in high numbers:

https://www.movesmartly.com/hs-fs/hubfs/PctHomesPurchasedByInvestors.jpg?t=1526599870033&width=1000&height=582&name=PctHomesPurchasedByInvestors.jpg

Curious to see what these numbers look like for Q1 2018. Personally, I wouldn’t count on this demand coming back into play from the sidelines, unless price appreciation picks up, particularly in some of the more far-flung areas of the GTA.

As for Vancouver, you’re bang on. SFH are struggling, detached inventory way up, sales way down. Condo market is hot.

“Last month’s sales were 22.5 per cent below the 10-year April sales average. There were 5,820 detached, attached and apartment properties newly listed for sale on the Multiple Listing Service® (MLS®) in Metro Vancouver in April 2018. This represents an 18.6 per cent increase compared to the 4,907 homes listed in April 2017 and a 30.8 per cent increase compared to March 2018 when 4,450 homes were listed. For all property types, the sales-to-active listings ratio for April 2018 is 26.3 per cent. By property type, the ratio is 14.1 per cent for detached homes, 36.1 per cent for townhomes, and 46.7 per cent for condominiums.”

https://www.rebgv.org/news-statistics/home-sales-down-listings-across-metro-vancouver

bal

at 8:25 am

housing bear can you please call me