I haven’t seen anything like this since….well, since this time last year.

Say what you want about the market; give your opinion on where we are. But there’s absolutely no denying what’s going on in the condo market right now, and even the most ardent market bear can’t show us data to the contrary.

Let me take a moment to show you where we are, where we were, and God help us – where we might be headed…

I just couldn’t bring myself to use a photo of an actual building on fire, so this really cool candle will just have to do.

Folks, what I said in the introduction there, about “the most ardent bear showing us data to the contrary,” is said out of necessity, rather than self-consciousness. I often remark that Toronto real estate makes for one of the most passionate, and often controversial, topics out there today. The “Big Three” things you don’t talk about in social settings used to be money, politics, and religion. Well in 2018, in Toronto, you can certainly add real estate to the mix.

Over the last couple of years, I’ve never seen the level of passion – and by that, I also mean excitement and joy, as well as frustration, anger, and resentment – expressed toward the Toronto real estate market.

It’s become a hobby for many, whether they own a home and are never moving, or are years away from owning one. It’s also become an area of sensitivity, for many with aspirations.

So whenever I write anything remotely positive about the market, those that have different outlooks, or different wishes, come out in full force.

I mail out an “E-Newsletter” each month to my clients, as well as my TRB subscribers who sign-up at the top of the page. And last month, I spoke of how busy the market is, and how things really took off in the last week of January.

To my surprise, I received one response from a person who accused me of “fear-mongoring,” which I didn’t think made sense, given my bullish outlook, but perhaps he meant that I was trying to create fear for those that don’t own real estate? Anyways, not important. Within his email, was a list of a dozen reasons why the market could, or will, decline. There was also a section on how TREB “fudges” the numbers each and every month, and that’s when I figured he was a tinfoil-hat type, and moved on.

So when I say today, “the most ardent bear can’t show us data to the contrary,” I’m basically asking for some opposing views.

The issue I always have is trying to convey what’s actually happening out there in the market, through my stories and experiences, and having the data to back it up.

Case in point, how about the 23-offer melee on a 1-bedroom condo on Front Street on Monday night?

Does that seem like a normal market occurance to you?

A relatively unspectacular, $499,900 unit, under-priced but not drastically, solicited twenty-three offers.

And it sold for almost $100,000 over the list price.

When I say “unspectacular,” I mean it’s nothing out of the ordinary. It’s a great location, but the unit itself is not made of gold; it’s simply square footage.

But in the 2018 Toronto condo market, as was the case in early-2017, “just a condo” is good enough to solicit multiple offers.

And this isn’t about under-pricing. Sure, a handful of those twenty-three offers could have been at the list price, with conditions. But most offers in this market are from people who play to win.

Virtually every condo listed in the central core right now has a “hold-back on offers,” and most of them are selling in multiple offers.

It’s just uncanny.

I thought I had found a unicorn earlier this week. I know it’s “an” unicorn, but that just looks weird…

A King West condo hit the market; 566 square feet, priced at $449,900, with offers any time.

No parking, no locker, and still $795/ sq ft. Add in the 110 square foot balcony, and I thought this was a real opportunity.

With no holdback on offers, I thought it was a great spot to see the unit over lunch (it had hit the market around 11am), and if everything checked out, make an offer with a short irrevocable, and see if we could catch the listing agent with his pants down.

I pulled the MPAC report for the unit (it costs $5.00 and TREB should make it mandatory for every listing in the city, to show square footage to buyers and buyer agents), and as luck would have it, the MPAC “square footage report” showed the unit at 456 square feet.

456 square feet, eh?

Where did the listing agent get 566 square feet from?

Oh, gee – the 110 square foot balcony. Let’s just add those together, and voila!

If something seems too good to be true in this market, it usually is.

At 456 square feet, this unit was actually priced at $987 per square foot.

And the irony is – a colleague remarked thereafter, “Nine-eighty-seven a square, with a balcony, a BBQ gas line, and in that location? Hmmm, not bad!”

Not bad, at a thousand bucks a square foot.

$1,000 per square foot. That’s such a big number, is it not?

And the crazy thing is – it’s not a rarity.

I’m looking through MLS right now…

New listing at 318 King Street East – 790 square feet for $719,000, hold-back on offers, and this unit is spectacular – it’s going to obliterate any record in the building. This will go well over $1K/sqft.

New listing at 510 King Street East – a bachelor unit, probably 450 square feet, for $400,000, with offers reviewed on March 5th. Could we see $1000/sqft here?

New listing at 390 Cherry Street – 600 square feet for $599K.

And on, and on, and on.

Many of you are thinking, “I thought the market was slow! Didn’t things change last year?”

That’s a fair line of questioning, and it’s something people email me whenever I use words like “hot” to describe the Toronto real estate market. As the theme went in last week’s blog posts, people will create their own narrative, and say things like, “Interest rates went up, and the B-20 rules came into effect. The United States is a mess, and it’s getting consumer confidence down. NAFTA…..the Canadian dollar…..manufacturing…….jobs……words……”

And while I could tell another dozen stories about my experiences thus far in the 2018 condo market, I want to show you what happened in the condo market last year.

More specifically, I want to show you what happened in the condo market last year, and contrast that with what happened in the housing market overall.

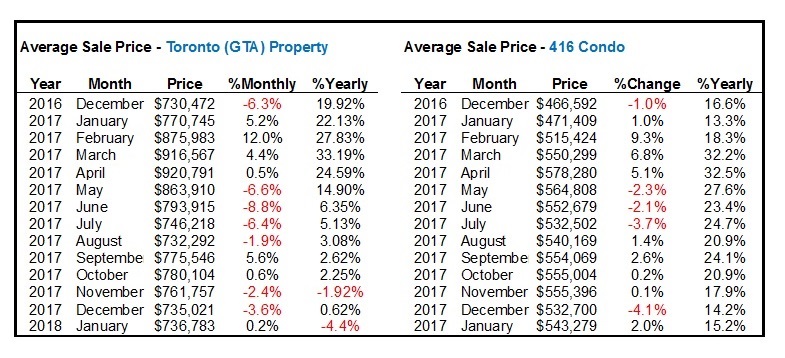

Take a look at the following chart.

On the left, we have the “Average GTA Sale Price,” which is the most-used metric of the Toronto market. This includes every single sale, for every type of property.

On the right, we have the “Average Sale Price – 416 Condo,” which is only looking at condominium sales, and only in the 416:

Some of you will choose to analyze this data at length, and I welcome your own interpretations.

The %Monthly refers to the increase/decrease in month-over-month price, and the %Yearly is obviously the same for year-over-year. Those percentages refer back to prices not shown on the chart.

As we all know, the Toronto real estate market in the spring of 2017 was probably the hottest 4-month period on record.

Look at the month of February, where we saw the average home price appreciate 12.0% alone.

Again, there are reasons for this.

January is typically slow, without a lot of new listings, and much of the inventory is “junk” that’s held over from the previous year. So to suggest that every property in the city was selling for 12% more in February than in January is misguided.

But taking these numbers at face-value, and comparing the overall market to that of the condo market, we can see how the condo market has risen to its current value.

First and foremost, I don’t put much stock into the month of December. Nobody lists real estate for sale in the month of December, if they can help it. Much of what is sold is simply the leftovers, but I included the month just so you could see how we came into 2017.

The start to 2017 was fast and furious, as noted in this space many times before. And it was the freehold market that did most of the work, as you can see from a comparison between the overall GTA market compared to the 416 condo market.

The average home price increased 5.2% in January, but the average 416 condo price only added 1.0%.

And then in February, as mentioned above, we saw a whopping 12.0% gain in the overall GTA home price, as the 416 condo market lagged behind at 9.3%.

But this is where thing started to change.

March saw another 4.4% added to the overall market, but it was outpaced by the 416 condo market, which added 6.8%.

Then in April, when the overall market stopped on a dime around mid-month, we saw only 0.5% added to the overall market, and yet the 416 condo market kept moving – adding 5.1%.

Everything dropped thereafter, but the condo market didn’t decrease in line with the overall market average.

May saw a -6.6% drop in the GTA home price, and only -2.3% in the 416 condo market.

Those numbers were -8.8% and -2.1% respectively in June.

And then -6.4% and -3.7% respectively in July.

Then in August, as the GTA overall price dropped -1.9%, the 416 condo market actually increased by 1.4%.

Come September, when most home-buyers were back out again in full-force, the overall GTA average increased 5.6%, compared to a more modest 2.6% increase in the 416 condo market.

The finish to 2017 was somewhat similar for both numbers, after a more balanced couple of months.

For the month of December, 2017, the “Average GTA Sale Price” was up 0.62%, from December of 2016.

For the month of December, 2017, the “Average 416 Condo Sale” was up 14.1%, from December of 2016.

That, in my mind, tells the story of the current condominium market in the central core.

The entire market shot up like a cannon to start the year, but as things levelled off in the overall market, the condo market just kept going.

And as is usually the case, it’s the lowest-priced, easiest-to-acquire properties that outperform, as there is more demand.

You can see from the chart below that the average 416 condo sale is up 2.0% in January, compared to a modest increase of 0.2% for the overall GTA market. I expect this trend to continue into February, and if I had to guess, I’d say the average 416 condo sale price will show a 4% increase, month-over-month, when the TREB numbers are released next week.

It’s worth noting that a 6.4% increase would take us back to the average price in April of 2017, which represents the “peak,” and I would expect this to be met by the end of March. Hell, the February data might show it’s already passed.

I’ll leave you with this final thought, because I know people love when I compare Toronto to New York city.

The average price per square foot for condos and co-op apartments (they’re grouped together, unfortunately, otherwise the number would be far higher), in 2017 was $1,775 USD, or approximately $2,272 CDN, to compare to our market.

“Luxury” properties, which is basically anything being built new, averaged $2,978 per square foot in 2017, or $3,812 CDN.

I’m not suggesting that Toronto, is in any way, shape, or form, comparable to that of prime New York City.

But it sure makes for an interesting discussion…

Natrx

at 9:52 am

IIMO, the rent rules imposed last year have had a huge factor in this. For example, there was an REIT owned apartment building I rented at Yonge n Eglinton a few years ago. These type of buildings have had stable rent for along time. I would check here and there even after moving out just out of curiosity. The price stayed consistent in the $1,250-1300/month range while the 2 bedrooms were in the $1,800 range. Since the rules, that same 1 bedroom is listed at about $1,800/month and 2 bedroom at $2,400 type range. Historically, they were ‘cheaper’ than an equivalent condo, but even with them, the gap has closed.

With those rates, why not just buy a place like a condo.

Plus, you have the softening of non-multi residential units (prices still high, harder to get higher loans) + more and more millennial reaching the historical house purchasing age + more and more immigrants to the city + now rising price euphoria and FOMO = hot hot entry level condo market.

Marina

at 10:14 am

Agree!

I rented at Y&E for years at that rate too – I wonder if it’s the same building. It’s exactly what everyone sane said was going to happen when the regulations came in.

To your point about millenials, I think we are getting into a property ladder type situation. I hadn’t heard the term until a friend in London went in with her sister on some run down row house in a rapidly gentrifying outskirt. She said basically there you try to buy as soon as you can, because the market will always outpace your saving power. You buy, pay down, and when you can, you upgrade, but the property you own has appreciated with the market and gives you a boost.

I know of a lot of younger people who are trying to jump in the market as soon as possible because they are worried 5 years down the line they won’t be able to buy anything. I know my husband and I could not afford our house right now. Thankfully we bought 8 years ago.

Sardonic Lizard

at 4:28 pm

>> She said basically there you try to buy as soon as you can, because the market will always outpace your saving power.

Smart friend you have there.

>> I know my husband and I could not afford our house right now. Thankfully we bought 8 years ago.

Count your blessings.

George

at 11:40 pm

I recall you saying never buy a pre construction condo 5 years ago. Most have gone up $500 per sq ft. Do you wish to comment?

Sardonic Lizard

at 4:11 pm

Five years ago? You must have me confused with someone else, since I haven’t been posting for that long.

Travel Consultant

at 10:19 am

A new life awaits you in the Richmond Hill colony!

Tired of being treated like a number in the downtown condo market? With 350% of last year’s selection, and dollar volumes at only 26% of last year’s levels, you are NEVER just a number in the Richmond Hill detached market! Our agents are well trained and obsequious. Talk to one of our leverage consultants today, and secure LAND for yourself and your heirs!

Sardonic Lizard

at 4:18 pm

Sounds like paradise! Where do I sign up?

I bet the locals are wonderful. Should I brush up on my Mandarin?

Kyle

at 10:25 am

Condos are the new starter home. And half of young adults (ages 20 – 34) in Toronto still live with their parents, over the next few years many of these people will be looking to move out. As others have mentioned renting certainly isn’t a bargain, so buying becomes more attractive. Don’t expect to see condo prices coming down anytime soon.

Real estate millennial

at 10:57 am

I love the New York comparison most people take that literally but if you take the perspective of what New York means to America I think we can find the correlation very easily. New York is the economic hub and the engine that powers the United States. Toronto is no different when we look at Canada, Toronto and the GTA represent our largest populous, it’s the most diversified economy we have in Canada, and it attracts more immigration and migration than any other city in Canada. So clearly Toronto is the economic engine to Canada and prices have a long way to go in Toronto before this is reflected. Toronto is not the most expensive city in Canada with Vancouver holding that title, but Toronto has a gdp 3 times Vancouver. So until Toronto passes Vancouver for the most expensive city in Canada I still think it’s on the cheap.

Sardonic Lizard

at 4:14 pm

> New York is the economic hub and the engine that powers the United States.

No, that honour belongs to California.

Drowzee

at 9:20 pm

The GTA is now more expensive than the New York metro area: http://www.huffingtonpost.ca/2017/01/24/toronto-nyc-affordability-house-prices_n_14344230.html

Kyle

at 11:13 am

The basis for which they are using to measure “expensiveness” is the median income / average price. Which isn’t apples-to-apples from City to City. Toronto’s multiple is higher because the average price is made up of a mix of freeholds and multis, whereas in New York the average price is comprised of many more tiny studios.

Drowzee

at 8:42 pm

I said “metro area”, which even includes parts of New Jersey in New York’s case. Many people live in detached houses in those suburban areas, like in our 905. Even if we’re talking NYC proper, most people don’t live in Manhattan: they live in the other boroughs.

In any case, it doesn’t make much sense to compare the two cities, when the US economy is 12 times as big as Canada’s. More comparable US cities might be Atlanta, Boston, Chicago, Dallas, or Washington.

Derek

at 11:14 am

What types of buyers should be entering the 1 or 2 BR condo market currently, in your opinion? Is it a good time to get on the property ladder with a 5 year horizon to sell and move up to bigger or detached? Is it a good time to buy a condo for the purpose of renting for income or capital appreciation? Is it only a good time if your plan to keep it as primary residence for a decade plus? What advice are you giving to clients relative to their plans and goals for ownership?

Sardonic Lizard

at 4:13 pm

> What types of buyers should be entering the 1 or 2 BR condo market currently, in your opinion?

Retirees and boomers looking to downsize, foreigners, students, or young couples who are no longer approved for bigger mortgages (B20). Of course there will be speculators in that mix, as well as flippers.

Ryan

at 11:32 am

Definitely agree with the results that 416 condo market kept increasing especially in downtown area. Could you kindly provide any thoughts from a market participant pespective for the reasons behind current hot condo market?

Geoff

at 11:38 am

here’s my unnecessary comment: it’s actually ‘a unicorn’ not ‘an unicorn’ because it begins with a consonant sound – just as you’d say ‘I earned an MBA degree (true by the way) versus ‘I earned a MBA degree’ because it begins with a vowel sound (‘e’). Language, like real estate, has rules that aren’t 100% enforced 100% of the time.

Jackie

at 11:46 am

I think the 1BR condo market is on fire in C01 and C08 only. Zolo shows that from Jan 28 to Feb 25th, sold listings are down 38% YoY for 1BR. Overall condo is down 35% YoY for this time period.

C'mon!

at 1:16 pm

You appear to be confusing and conflating sales volume with sale price.

iwill

at 1:17 pm

sales are down but not prices…

Paul

at 12:19 pm

Basically takes 90-100K income to buy a 1B in Toronto. Is that reasonable/sustainable?

Kyle

at 1:04 pm

The median household income is $80K (i.e. a bit shy of your 90-100K benchmark), it means that a bit shy of half of Toronto’s 2M households can afford to buy a 1 bdrm condo. Since there are only roughly 50K condos sold in a year, i would say it is perfectly reasonable and sustainable for the foreseeable future.

Chris

at 1:48 pm

Some quick math on Ratehub’s Affordability calculator (available here: https://www.ratehub.ca/mortgage-affordability-calculator)

Inputs:

Annual Income – $80,000 (two individuals making $40,000 each)

Debts – $0

Property Tax, Condo Fees and Heating Costs – Estimated by Ratehub (dependent on property value)

Down payment – $100,000

Amortization period – 25 years

Mortgage rate – 4.15% (current available lowest rate + 2.0%, for B20 stress test)

City of Toronto, first time home buyer rebates applied, condominium home type.

Output:

Home Price – $456,791

Bit of a gap between that and the average condominium price of ~$545,000, let alone the 1B David cited that sold for ~$699,000.

Feel free to adjust the inputs and see what you get. Obviously home price will vary depending on these numbers, particularly down payment and annual income.

Kyle

at 2:54 pm

We’re talking about reasonability here…

The point was never about whether the median household can afford David’s sample condo. No one ever said or implied that.

The point is a large chunk of a large number of households can afford a 1B condo, so it is reasonable that the 50 or so thousand condo sales per year can continue to sustain these prices.

Chris

at 3:14 pm

“The median household income is $80K…it means that a bit shy of half of Toronto’s 2M households can afford to buy a 1 bdrm condo.”

“We’re talking about reasonability here…The point was never about whether the median household can afford David’s sample condo.”

I think you’re moving the goal posts a little bit here. Your initial post seemed to assert that the median household can afford a 1B condo.

Yet, with the exception of the bachelor apartment, none of the examples David provided are affordable with the inputs I used. The average Toronto condo is not affordable with the inputs I used. The average 1B condo in Toronto from Zolo, priced at $486,000, is not affordable with the inputs I used.

Yes, that still leaves many households for whom it is affordable; many more than the number of condos that change hands in a given year. But I don’t think I would go so far as to say that it is affordable for those at the median income level, as the math demonstrates.

Kramer

at 3:57 pm

How many times do we have to have the old “median/average income” relevance conversation?

Chris

at 4:05 pm

Kramer, please carefully re-read Kyle’s post.

He brings up median income, asserting that a median household income of $80k means a 1B condo is affordable.

You’ve already explained at length that you place no value on the metric of median household income as it relates to home affordability; that’s your prerogative, albeit one that I, as well as many others, disagree with (RBC publishes a quarterly report looking at affordability as defined by home price to income http://www.rbc.com/newsroom/reports/rbc-housing-affordability.html).

In this case, however, my argument is that Kyle’s assertion, that a 1B condo is affordable for a median income household, is incorrect, given the inputs I have used on Ratehubs affordability calculator. If you would like to debate this, by all means, have at ‘er. If you’re just going to re-hash the fact that you feel median income is irrelevant, well, I don’t think there’s really any more to be said on that front; we can agree to disagree.

Kyle

at 4:12 pm

Again Chris, i’m not referring to specific examples provided by David. I’m talking about r-e-a-s-o-n-a-b-i-l-i-t-y….So not sure why you keep trying to bring it back to specific cases. It has nothing to do with me moving the goal posts, because i am not talking specific goal posts, i’m talking ballparks (or stadiums). Paul used a rough benchmark, not a precise specific example, which is what this conversation is about.

Average condos of all varieties (bach – 3 bedroom) is $543K.

Kyle

at 4:23 pm

…Continued from above clicked Post by accident….

Average condos of all varieties (bach – 3 bedroom) is $543K (which is what you chose as your first goal post), but Paul and i were talking 1B all along (which you acknowledge is actually only 486K) – so who’s moving goal posts now?

The point i make has nothing to do with what the median household can afford, the point i am making by using the median is that the median person represents halfway mark of the distribution. Meaning the entire right half of the distribution lies above the median. Therefore close to half the households out there can afford a 1B condo.

Joel

at 3:05 pm

For the mortgage qualification you have to use 5.14% as a minimum. So those numbers will be slightly less.

Chris

at 3:16 pm

Ah, good point, I forgot that it was the higher of the posted BoC rate (currently 5.14%) or +2.0% to the contract rate. In this scenario, yes, it would be stress tested at 5.14%, rather than 4.15% (2.15 + 2.00).

EDWIN

at 7:35 pm

How is it reasonable that it takes an above average DUAL income to afford a 1B condo?

A 1B condo should be able to be supported by a single income.

Kyle

at 9:27 am

“A 1B condo should be able to be supported by a single income.”

But why “should” this be, when it isn’t the case in just about every other global city?

Drowzee

at 8:40 pm

Wages and salaries tend to increase over the course of a career. So most above-median households will be older ones with kids. I don’t think they’d be in the market for 1BR condos.

Most childless households will be below that median income.

Dave

at 12:36 pm

What about the pool of people who’ve locked in their mortgages in Dec-2017 and are trying to get on the property ladder before their pre-approvals expire end of March. Wouldn’t this be a notable driver for the current condo market? I don’t think it’s sustainable that people are willing to pay $1000 psf for condos now with all the headwinds and uncertainty ahead for the Canadian economy…

C'mon!

at 1:50 pm

Name a time when the future of the economy was “certain.”

Joel

at 3:03 pm

David: From your personal and purely anecdotal experience what is the age range of those buying condos in the core in the last year? Are we seeing an older demographic 30+ entering the real estate market by purchasing their first home as a condo, or is it still largely the mid to late 20’s and investors purchasing these properties?

I am more wondering if we are seeing an actual mindset switch to people choosing to live their lives in these condos, or if it is the same people purchasing the same condos, but at higher prices?

Professional Shanker

at 3:29 pm

What David’s 416 condo market anecdotes likely proof is that B-20 and recent interest rate increases are having a significant impact on the market – specifically the higher end detached market in the GTA. If condo sales (volume) are moderate/high and record prices are being achieved why wouldn’t we be seeing increasing sales and prices in the detached market given that most of the sellers should be move up buyers?

Is this because most of the sellers are not re-buying (either foreign capital, choosing to rent, boomer’s downsizing, increased speculation in the lower end of the market) or what other reasons could you attribute softness at the top the market while the bottom end is scorching hot?

Sardonic Lizard

at 3:53 pm

> Is this because most of the sellers are not re-buying…

It’s because most of these sellers already have a primary residence, and the condo they’re selling is just an income property.

Professional Shanker

at 4:58 pm

in that case, congratulations on crystallizing their equity gains…

steve

at 8:45 pm

time to check the demographic?

pkap007

at 3:54 pm

would be interesting to know David a little more about the buyers. A 1Bed in downtown even if it goes for say 2200 pm in rent @20% down per ratehub min pm mortage comes to $2500 so from day one an investor will be cash flow -ve. but if one is looking to buy for personal use even then paying $700K for a 1B just crazy..

Professional Shanker

at 4:57 pm

Re: investors – you have not even included maintenance and property taxes into the equation yet. But the presumptive argument is that the negative cash flow will be more than offset by leveraged gains in market value which over the past couple years has proven true – in 5 to 10 years will it?

steve

at 8:43 pm

good question … it’s a speculative move …. I prefer never to buy with negative cash flow

Chris

at 4:24 pm

Kyle, please carefully re-read what I posted. Yes, I included an assessment of the specific examples David used in this post. I also included the overall average condo price (which, you are correct, includes bach – 3 bedrooms), and the 1B condo price from Zolo, of $486,000.

That hardly seems like I’m trying to “bring it back to specific cases”, despite your assertion to the contrary.

You seemed to claim that a 1B condo is affordable for the median household. A 1B condo, from Zolo’s data, has an average price of $486,000 (if you have another figure to offer for this segment of the market, I’m all ears). Using the median household income, as well as the other inputs, I calculated affordability to be ~$456,000.

Thus, it does not appear that a 1B condo is affordable for the median household. With a higher income, greater down payment, etc., sure. But using the inputs I stipulated above, no. Sorry, but the math doesn’t work.

Kramer

at 4:29 pm

Why is the median income so important?

Why isn’t the 40th percentile income the most important metric?

Or the 60th percentile?

Seriously. Try explaining why.

Kramer

at 4:31 pm

You can’t because unless you attach it to other variables in the equation for some specific reason (i.e. population size, sales, number of houses/units/whatever available, number of people needing a home, etc, whatever) median income is as arbitrary as 40th or 60th percentile income.

Kramer

at 4:33 pm

And “WELL, BECAUSE IT REPRESENTS AROUND THE AVERAGE” is not the answer.

Chris

at 4:34 pm

Kramer, please refer to the following:

https://torontorealtyblog.com/archives/20490#comment-81329

I don’t really feel like arguing with you yet again about the usefulness of median household income. You clearly don’t think it’s important. That’s fine. Others do place value on it as a metric upon which to trend over time, such as RBC in their affordability report.

But again, this isn’t really what we’re discussing right now, nor do I feel like wading into it once more.

Kramer

at 4:46 pm

Exactly.

I think it’s quite possible that some other income metric is most important. i.e. Top 30th percentile income, for example.

Because despite the average/median being $X… with a 30th percentile of $Y, and a growing population of Z… the number of people that make up the 30th percentile vs the total supply is great enough to determine the prices.

Something like that.

Or you could just ignore the multi-decade diverging trend line and say that the arbitrary median income metric is all powerful no matter what. Because it’s in the middle, nothing else considered.

Kramer

at 4:52 pm

And for anyone to say that median income is all powerful in ALL real estate markets, no matter what, no matter how different the markets are, regardless of other statistics, trends, profiles, politics, etc … well that’s just plain ignorance.

Chris

at 5:17 pm

I get the impression that you want to debate one thing while we’re currently talking about something else.

As I said, I don’t really feel like arguing with you again regarding the use of median household income.

Kyle

at 5:27 pm

“You seemed to claim that a 1B condo is affordable for the median household.” Wrong, this is not what i am claiming at all.

I don’t actually care whether the median household can afford the average condo or not. My argument is not predicated on the median being able to afford it.

Pay close attention here – I am saying that (regardless of whether they can or not) if the median household is close to being able to afford a 1BD (which they clearly are 457K vs 486K – uding your numbers ), then of the 50% of all households that lie above the median, a huge chunk of them can afford a 1B.

Professional Shanker

at 5:47 pm

but with home ownership at 70% of the population, wouldn’t roughly 70% have to be able to afford it on a long term basis, notwithstanding other factors (interest rates, etc.) which increase or decrease ability to purchase property?

That said the share of multiple property owners have increased, combined with increased domestic speculation and lastly increased foreign investment have all factored into the ability for prices to decouple itself from local income.

Kramer

at 5:56 pm

Shanks,

With that I would ask that of the 70% of the population that are homeowners, how many of them already own their home outright? Or have it 80% paid off… etc.

I think you need to add that perspective and probably more to the mix. Know what I mean?

Professional Shanker

at 2:06 pm

With that I would ask that of the 70% of the population that are homeowners, how many of them already own their home outright? Or have it 80% paid off… etc.

The stats say a significant majority of people own their home outright or have over 50% equity paid off due largely to price appreciation but that still does nothing to support that over the long term median income must support house price appreciation.

My take on your and Kyle’s debate with Chris is that he is arguing a that the metric is important on a long term basis while you are pointing one reasons why it can diverge on a short term basis – both are valid arguments.

Kramer

at 2:56 pm

Shanks, you mentioned price appreciation, but I was talking about their mortgages being paid off completely, or 50% paid off (I said house paid off, i specifically meant mortgages)… so I don’t really care about if their equity has gone up due to price appreciation – that point was more about that even if prices are high, many have zero mortgage, or only 50% or 40% or 30% of their mortgage left… so their house is pretty dang affordable to them… they might not need median income to afford their home.

Along the same lines is the impact of accumulated wealth over time… it also plays a role in detaching home prices from median income.

And as for the other thing, I believe that price has diverged from median income over the long run, and that it is an irrelevant statistic in determine affordability or in determining if the housing market is over or under valued. Some income statistic is, and it’s unique to Toronto. Median income might be relevant for some small town in middle of nowhere USA or Canada… but not in Toronto.

Professional Shanker

at 3:19 pm

I do see where you are coming from, some good points you have, which allows me to understand/partially accept why prices can deviate from income on short term basis.

Your comment on wealth accumulation is why I presume London and other cities (older European) which have more generational money can continue to diverge on a long term basis.

BJA

at 3:27 pm

Surely someone has statistics on people like my wife and me, both in our early 60s, own our house outright (Broadview/Danforth 3BR detached, so probably worth $1M or thereabouts), live on roughly $60K/year from OAS/CPP/small pension/RSPs/TFSAs, so certainly well below median HH income. Must be lots of “us,” particularly in the core.

Kyle

at 7:33 pm

@ Professional Shanker

Perhaps if there was a reason that home ownership rate had to stay constant over time, but there is no reason that this state must hold.

Chris

at 7:59 pm

When I suggested this last during a discussion we had about millennials buying homes, indicating that many European countries had lower ownership rates and more renters, you went off on me, claiming that my statement was purely hypothetical, why would things change from the way they had been, demand will be the same across generations, etc. etc.

Now you’re parroting my talking point in support of your thesis?

You’ll forgive me if I call hypocrisy on this. Which one is it, Kyle? Will trends hold steady as you originally predicted? Or is your new prediction that historical trends will be bucked?

Kyle

at 8:12 pm

You’ll have to refresh my memory (or more likely re-read what you claim i wrote), because i have never said that ownership rates would stay constant over time. I have actually said over time i expect ownership rates to decline as it does in all other global cities.

Chris

at 8:17 pm

“because i have never said that ownership rates would stay constant over time. I have actually said over time i expect ownership rates to decline as it does in all other global cities.”

“”Perhaps Millennials will follow in the footsteps of their European peers, and rent in greater numbers”. We don’t suddenly assume some unforeseen, unprecedented change in behaviour across an entire generation could occur that could invalidate the obvious math that larger % of larger population > smaller percentage of smaller population. Besides the majority of millennials have all stated that they want to own detached houses”

https://torontorealtyblog.com/archives/19735#comment-77343

You seem to be at odds with yourself, Kyle.

Kyle

at 8:56 pm

Once again putting words in my mouth and reframing my arguments into something i never said….cheap Chris, very cheap!

Saying i don’t agree with some ridiculously impossible fantasy scenario that you conjured up (i.e. over the course of few years, millenials suddenly decide en masse that they want to become renters for life), is absolutely not at odds with saying that over time ownership rates will decline.

Chris

at 9:36 pm

In one breath, you claim that ownership rates will decline over time; in the next, you claim I’m completely out to lunch for postulating that perhaps millennials will not buy homes as prolifically as baby boomers and will rent instead (thus decreasing the ownership rate).

And yet, somehow, this qualifies as cheaply re-framing your argument?

Uh huh…makes perfect sense, pal…

Kramer

at 5:48 pm

That’s how I read your original comment Kyle.

And that’s connected to what I’m saying about median income being arbitrary as a relevant income stat.

Maybe the chunk of people you’re referring to are the top 30th percentile and the only ones who matter in determining price of this market.

Chris

at 6:25 pm

Kyle’s original comment doesn’t make any mention of median household income as an important or arbitrary metric. Not sure where you gleaned this from.

Rather, the comment uses median household income as it relates to number of households, to assess the rough number of households for whom a 1B condo is affordable.

As an aside, if only the top ~45-40th percentile are determining pricing of the 1B condo market, what percentile and thus number of households are determining the price of larger condos, townhouses, semi-detached and detached homes?

Chris

at 5:56 pm

“The median household income is $80K it means that a bit shy of half of Toronto’s 2M households can afford to buy a 1 bdrm condo“

““You seemed to claim that a 1B condo is affordable for the median household.” Wrong, this is not what i am claiming at all.”

Your own quotes don’t jive very well, but ok…so just shy of half of households are just shy of being able to afford just an entry level condo.

You may call this reasonable and sustainable. I would not.

Kramer

at 5:58 pm

Weak chris. Stop going back to his old comments where he wasn’t in “watch every word/interpretation debate with chris” mode, and read from where he says “pay close attention here”. Can you deal with that?

Chris

at 6:02 pm

Ah so you’re saying I should give kyle the benefit of the doubt and not hold him to his quotes? The same courtesy that I’m sure you and him would extend to me, right?

Kramer

at 6:15 pm

Good lord.

Chris

at 6:21 pm

“Stop going back to his old comments”

Good lord is right.

By your standards, comments from earlier today are now “old” and to be ignored and discarded, not used in further discussion or callbacks.

Kramer

at 6:22 pm

When you misinterpreted them and he clarified, yes. That’s pretty standard. What is this a courtroom?

Chris

at 6:27 pm

Yep, he clarified, to which I said:

“So just shy of half of households are just shy of being able to afford just an entry level condo.

You may call this reasonable and sustainable. I would not.”

Did you miss that part, where the discussion moved forward, Kramer?

Kyle

at 7:45 pm

@ Chris

When i say “just shy” i mean exactly that. It means not quite half. If i was trying to say the median can afford to buy the average condo, therefore an amount greater than 50% i would have left out the “Just shy”. You need to learn how to read dude.

Chris

at 7:51 pm

Thanks, dude, but I know how to read just fine.

So what is just shy of the median? 49th percentile? 45th percentile? What household income does this translate to? I’m happy to crunch the numbers on Ratehub for you on these ones as well, so we can see how your assertion of 1B condo affordability holds up.

I bet the results would be tubular, dude!

By the way, I already addressed your “just shy” caveat:

“So just shy of half of households are just shy of being able to afford just an entry level condo.

You may call this reasonable and sustainable. I would not.”

Kyle

at 8:17 pm

If you don’t think it’s sustainable that’s fair, you’re entitled to that. You are absolutely not entitled to put words into my mouth. And when you keep doubling down on what is clearly your mistake, then you’ll forgive me for thinking you don’t understand the meaning of “just shy”.

Chris

at 8:20 pm

Once again, what is “just shy” in numeric terms, please and thank you.

Kyle

at 8:47 pm

Using your numbers again, the difference between what you think the median household can afford vs what the 1BD average condo costs equates to about $2K in annual income. While it would not surprise me, if you actually thought 5 percentiles separates someone making $80K vs someone making $82K, the truth is it is actually from a percentile perspective best described as “just shy”

Kyle

at 5:35 pm

“you want to debate one thing while we’re currently talking about something else.”

To be honest Chris, that’s exactly what you are doing with my response to Paul.

Chris

at 5:58 pm

To be honest Kyle, what I did was present simple numbers to mathematically assess your claim. If you feel that is unrelated to your original comment, well I can’t really help you with that one, pal.

Kyle

at 7:38 pm

Actually Chris, what you did was present simple numbers to mathematically assess SOMETHING I NEVER CLAIMED. If you can’t understand that, then it is not me that needs help.

Chris

at 7:53 pm

It was an assessment of a median household income’s ability to afford a 1B condo, which you claimed they were just shy of. As you didn’t give any other figures (percentiles or incomes to work with) I worked with what you provided.

Pretty straightforward stuff, pal.

Kyle

at 8:10 pm

Like i said below, if i were trying too claim that the median could afford it (which i didn’t), i’d have left out the “just shy”. Pretty straight forward stuff.

Chris

at 8:19 pm

I addressed that below. Pretty straightforward stuff, pal.

Kramer

at 6:38 pm

Median income is an arbitrary metric in terms of determining if an individual real estate market is overvalued.

Belief that median income is the overriding valuation input for ALL real estate markets, regardless of their population trends, economics, supply, supply growth potential, and other important variables and characteristics… is ignorant.

For each individual real estate market there must be some percentile income statistic that is relevant based on the market’s variables and characteristics.

For Toronto, with a growing population, strong economy, low supply growth potential, the key income metric is certainly above median price.

Someone should do a full study on this. It’s not going to be me, but there’s the theory.

Chris

at 7:07 pm

Most people don’t lead off presenting their unsupported theories, which lack any study, as a definitive statement. You would have been prudent to phrase it more along the lines of “Does median income have a bearing on determining if an individual real estate market is overvalued?”

Further, nobody, to my knowledge, has postulated that median income is the be all and end all, the overriding factor, against which all other factors are irrelevant. To suggest that many people are…is ignorant.

Rather, most have suggested that it is an important metric, particularly the trend of the home price to median income ratio. How does it compare over time? How does it compare to other cities?

Finally, for the umpteenth time, median household income has been used in previous discussion on today’s post to arrive at a rough estimate of the absolute number of households for whom a 1B condo is (just shy of) affordable. You have steered us into the discussion about it’s usefulness as a metric of valuation, but to launch at me like you originally did for referring to median income (here: https://torontorealtyblog.com/archives/20490#comment-81328) betrays a lack of reading comprehension and/or inability to follow the discussion. A quick scroll up clearly shows how it was being used in the conversation, and that it was Kyle who introduced the term.

Kramer

at 7:14 pm

This comment wasn’t directed at you, but thanks for your useful feedback.

Chris

at 7:46 pm

Happy to help.

Kyle

at 11:37 am

@ Kramer

“For each individual real estate market there must be some percentile income statistic that is relevant based on the market’s variables and characteristics.”

This is bang on! The shape of the income distribution and changes to that shape over time play a huge part in what drives the real estate market. As has been established, when you look at Toronto the entire bottom half of the distribution can largely be ignored since those households earning under 80K are priced out. Which means the median income for Toronto is a terrible proxy for real estate values. In large cities, median income has no bearing on real estate values. It’s only use is for those who (as David eloquently put it) want to perpetuate their narratives.

To my mind it makes way more sense to ignore the left half of the distribution all together and figure out what the mean is of the remaining population, and that will be a far better indicator of what real estate values are supportable. This way you do a far better job of aligning the incomes of the home buying/selling population with the values of real estate.

Kramer

at 4:01 pm

Sorry Kyle, didn’t see this until now.

I absolutely baked in your many previous thoughts/comments (over the months) on the right tail being more important in determining whether the market is affordable, unaffordable, overvalued, undervalued. We can be co-authors of this study.

I think this really ties everything together, the idea that every city has its own individual relevant income metric (i.e. possibly a specific percentile)… and I think it helps make a lot of sense of all the data that is thrown at us constantly.

The model for determining this unique income metric for every city would be an epic one, and I think that the outputs of this model could be the key for actually determining if a particular real estate market is overvalued or undervalued at a given moment in time.

Kyle

at 5:10 pm

So another hypothesis of mine that seems to have very strong correlation and support when you look at what’s happening in various market, is to not just look at income levels, but to think about different types of compensation schemes.

I definitely see a correlation between the growth in home prices and the growth in infrequent but large payout type compensation schemes (e.g.equity participation / option plans, high water mark fund plans, etc.) . Cities where these types of compensation schemes are more common (e.g. San Fran, New York, Toronto, Boston, etc) have experienced very high RE price growth. Cities where these schemes are less common (e.g. Ottawa, Montreal, Chicago, etc) have not experienced the same sort of growth.

And this to me jives with human nature. I can totally see people who suddenly find themselves with a boat load of vested options, or their company goes public and their equity is suddenly worth multiples more, it’s like a lottery win. And what is one of the first things people want if they win a lottery? A new home.

steve

at 8:38 pm

I think it would be useful to consider who’s buying the downtown condos. Sales in the central detached market seem to have dropped as well as listings, but as David points out, condos are up.

susie

at 9:42 pm

detached market is also on fire..everything going over..

Chris

at 9:33 pm

First of all, it’s not “what I think”, the math is there, you can adjust the inputs and see the result for yourself. Math is not an opinion, Kyle.

Second of all, your assertion is incorrect. An annual household income of $82,000 (two individuals at $41k each) qualifies for a home price of $466k (keeping all other inputs the same, with the exception of B20 stress test rate which is corrected to 5.14%).

In order to qualify for the $486k required for the average 1B condo, a household income of $86,000 is required.

Chris

at 9:33 pm

Meant as a reply to this post:

https://torontorealtyblog.com/archives/20490#comment-81384

Kyle

at 9:42 pm

Math isn’t an opinion, but some of the other variables are. So yeah it is what you think

Kyle

at 9:59 pm

As for my second assertion being incorrect, like i said i used your numbers. Difference between 457 and 486, is 29K, which carries for $171/month @ 5.14 over 25 years. That’s $2,064 per year. So if there was a miscalculation it was in coming up with your numbers not mine.

Chris

at 10:27 pm

The only variable I entered was the down payment of $100,000. Any calculation of affordability requires one, and that seemed as decent a middle ground as any. You provided median income. Mortgage rate for B20 is set by BoC. Other monthly costs are estimated by the calculator.

So no, it isn’t “what I think”. Sorry pal.

As for your second assertion, crunch the numbers for yourself with the affordability calculator. Holding all other variables steady and increasing annual income by $2,000 does not allow for an average price 1B condo to be purchased.

Not to mention, paying out $2,000 more per year does not translate directly into making $2,000 more gross per year. You know there are taxes etc., right?

Kyle

at 10:35 pm

And you know they have amortizations greater than 25 years, right?

Chris

at 10:39 pm

And you know that when you extend the amortization to 30 years from 25 on the affordability calculator, it results in a home price of $428k, right?

Same inputs. $82k household income. Feel free to check it for yourself.

Kyle

at 11:00 pm

“The only variable I entered was the down payment of $100,000. ”

Thanks for checking the math, but I’m not saying i used 30 years to calculate. I’m saying YOU chose to use 25 years instead of 30, as in that is another variable that YOU chose.

Chris

at 11:04 pm

25 years is the most common amortization length. And I just ran it with 30 years to show you the results. They’re in my post above.

And yet here you are jumping back a few comments to argue that “I chose” the inputs, rather than addressing the numbers they produced. What were you saying about cheap tactics? Pot, meet kettle.

Kyle

at 11:15 pm

Nothing cheap about my not addressing it. Sorry but 6K vs 2K is not worth addressing, they both fall squarely into the realm of just shy as far as i’m concerned. Nit picking over that 4K, as if it were going to make a meaningful difference in percentile however, that would definitely be cheap.

Chris

at 11:19 pm

Ah so the difference between $80,000 to $86,000, or 7.5%, is, in your books, just shy? Well see, that’s why I asked you define it numerically, because that’s a bit large for “just shy” from my standpoint.

By the way, did you look into the different affordability of 25 vs 30 year amortizations yet? You seemed confused on that point.

Kyle

at 11:28 pm

Truly pathetic attempt at a save. We’re talking about difference in percentiles not what the percentage diff between 86 vs 80 is, but again nice try at trying to reframe the argument to be something that it wasn’t

Chris

at 11:36 pm

What’s the difference in percentile between $80,000 and $86,000 then? Enlighten me. Surely you wouldn’t throw around words like “pathetic” without a solid knowledge base, right?

Kyle

at 11:50 pm

In the Toronto CMA 5.7% of households make between 80 – 90K. So the percentile diff between 80 and 86 is going to be approximately 60% of that or roughly 3.4%.

Chris

at 7:07 am

Ok so in your mind, ~3-4% qualifies as just shy? Was it so hard to assign a numeric value to that qualitative statement?

If you had simply lead with this instead of immediately getting your back up and yet again being rude, would have made for a much briefer and more pleasant discussion.

Kyle

at 9:19 am

As i said at the very, very beginning (without getting my back up), it’s about reasonability. I see no need to try to come up with a precise calculation (which ultimately will be based on assumptions so at best only provides a veneer of precision that in actuality is moot to the discussion), when talking in general terms. I get my back up when people falsely accuse me of making claims of this and that, because they want to manufacture arguments on the internet. As i said before i have no interest carrying on discussions with you. I see no value or purpose in wasting my time.

Chris

at 9:32 am

“As i said before i have no interest carrying on discussions with you.”

And yet you posted twenty-five times in response…interesting way of not carrying on a discussion, pal.

Kyle

at 9:08 am

“And yet you posted twenty-five times in response…interesting way of not carrying on a discussion, pal.”

You clearly have no idea what a discussion actually is. We may have had an exchange, but only the most obtuse would consider that to be a discussion (but considering who i’m talking to i’m not surprised).

As i said i have no interest in carrying on a discussion with you, because you’ve proven time and again that you’re not actually capable of doing that. You yourself add no value whatsoever to any discussion. All you do is argue every point with cheap annoying tactics.

Chris

at 9:47 am

Still going, eh Kyle?

“You clearly have no idea what a discussion actually is. We may have had an exchange”

Please brush up on the definitions for both of these terms:

https://www.merriam-webster.com/dictionary/discussion

https://www.merriam-webster.com/dictionary/exchange

It’s also humorous how you label any point you don’t like as “cheap” or “annoying” yet readily resort to ad hominem attacks, rudeness and straight up bullying.

Do you have anything else to add, or are you just planning to continue with more of your insult-laced rants?

Kyle

at 10:58 am

This is precisely what i’m talking about. Do you even try to understand the meaning or point of what someone says, before the little hamster wheel in your head furiously goes into overdrive to search for some way to argue against it? Dictionary definitions, really?

I can literally picture you sitting there fingers raised above the keyboard waiting for a reply so you can find something to poke at hoping desperately to eek out some kind of gotcha. It’s seriously very sad

Chris

at 11:18 am

Ah, so you are just planning on continuing your rants and insults. Good to know.

You tried to make a distinction between the definition of a discussion and an exchange, claiming that your hurried pace and high volume of replies did not constitute a “discussion”. Yet you clearly misunderstood what the terms mean. Therefore, I provided you with the definitions, so you may educate yourself and use them properly in the future.

Once again, your opinion does not really matter to me. You call me sad for pointing out mistakes, claiming I’m going for a “gotcha”. I would call you sad for how angry, confrontational, and rude you allow yourself to become. I’m sure many other readers would call us both sad for how often we post on this board. Such is life, eh pal?

Kyle

at 9:52 pm

“you claim I’m completely out to lunch for postulating that perhaps millennials will not buy homes as prolifically as baby boomers”

Seriously? You and your cheap re-framing of arguments into something they weren’t/aren’t, is getting so tired.

What you ACTUALLY postulated was that suddenly millenials so many millenials would stop buying that it would more than offset the far greater numbers in the millenial cohort than the previous generation (which by the way were not the boomers). ANd yes that is completely out to lunch.

Kyle

at 10:05 pm

Correcting my last paragraph…

What you ACTUALLY postulated was that suddenly so many millenials would stop buying that it would more than offset the far greater numbers in the millenial cohort than the previous generation (which by the way were not the boomers) as to reduce ABSOLUTE DEMAND – WE WERE NOT TALKING ABOUT THE OWNERSHIP RATE. And yes that is completely out to lunch.

Chris

at 10:36 pm

Thanks for the history lesson, but no, I haven’t forgotten about Generation X. Also very kind of you to tell me what I ACTUALLY postulated, in case I forgot what I was thinking for myself.

So, in your mind, Millennials will continue to buy homes at the rate Baby Boomers did, and simultaneously the home ownership rate will go down?

What’s getting tiring is your petulance, aggression, bullying, and just general unpleasant demeanor. And ya ya, you’re going to say something like I made you do it because of my comments. Whatever. You are, quite frankly, extremely rude. And have nobody to blame for that but yourself.

Kyle

at 10:54 pm

Yup i can accept that i am extremely rude towards those who insist on challenging every one of my comments with outrageously cheap arguments, who try to put words in my mouth because they don’t have any actual arguments, and who after getting caught over and over using the same annoying cheap tactics, persists on doubling down with more annoying cheap tactics. But since you knew that would be my response, you have no one to blame but yourself. Perhaps take you should take your own advice, if it offends you so much, instead of getting worked up over it just don’t respond.

Chris

at 11:05 pm

Blah blah blah yes all my points are cheap and you caught me and whatever.

Just because you make these claims and assign these labels in your head, doesn’t make them true. Sorry pal.

But hey, at least you agree that you’re a jackass.

Kyle

at 11:12 pm

Sure i can admit that i’m rude when warranted, i never said jackass- that would be you putting words in my mouth yet again. Unfortunately you still can’t admit how cheap your arguments are even though it’s plain as day.

Chris

at 11:15 pm

Sorry Kyle, let me fix that for you:

At least you can admit you are “extremely rude”. I would call that being a jackass, but hey, that’s just me.

Again, I don’t care if you think my points are cheap. The opinion of a jackass is not worth much in my books.

C'mon!

at 7:22 am

Hey Mr. pedantic, give it a rest. Your arguments are trivial, pointless and boring.

Chris

at 7:38 am

Hey Mr. Jackass. Simple solution for you: don’t read them!

Alexander

at 11:32 pm

I would say that in 2017 and 2018 condo prices are catching up with the past ( prior to spring 2017 ) price appreciation of the detached houses. And central locations are doing better. At one point condo buyers will realize they are overpaying for this privilege of living in city core. There is better value than 700 K 1 bedroom condo. Tightening mortgage rules did not help at all at the moment and location.

Condodweller

at 12:03 am

Value means different things to different people. Some value living walking distance from work and near thousands of restaurants and entertainment locations. I remember the day when there was a stigma attached to living downtown.

Alexander

at 10:04 pm

I can understand why young people (generally ) would love to live downtown – shorter transit, restaurants, etc. but for me this incredible rush to own a bachelor or 1 bdr condo is a symbol of mortgage and housing policies tightening. And those guys/girls are not going to be in bachelor/1 bdr forever. It would be interesting to see price differences in downtown core condo and midtown SFH over last 10-15 years.

Condodweller

at 10:12 am

I am not sure if you are still reading but I had a window open and saw your comment. You are right, most young people are not going to stay in a 1 bed forever but the important thing is that they get into the market to stop paying rent and start building equity. If prices continue rising forever, as the bulls on this board predict, where these people would never be able to get into the market if they hadn’t bought already they could make a 1 bedroom work for a long time.

Regarding historical prices, you can ask any agent to give these to you and I am sure you can google it and find it on the net if you looked. I can tell you from personal experience that a 1 bed condo downtown went for about $125k in 1996 at the bottom of the market. A SFH downtown would have been about $200k. By about 2004 a 1 bed condo reached $200k and I think SFH by then was around 400-500k. The gap continued to grow after that accelerating up to today.

Condodweller

at 12:00 am

That 1 million average price seems to be the limit most buyers are willing to pay. The trend seems to be heading where I was suggesting which is the focus keeps shifting down to whatever is available under 1 million. I questioned if we will ever see bachelors or even micro condos get close to the 1 million mark. Well, two beds are almost there, 1 bed is heading there. I can’t believe 1 beds are over 600k now. One of the buildings I watch had two sales recently of less than 600 sqft units that went around 600k.

It seems people are buying what they can afford, and it’s 1 bedroom condos now. A couple can live happily in a one bed condo but things will get tricky once the bachelors get up to this price point.

Kramer

at 9:10 am

One esteemed group doing their real estate predictions for 2018 also said that sales in the $500K-$1MM range are going to dominate things, kind of along the same lines of your thoughts, $1MM being a cap for a lot of people, which makes sense…

So yah, does this mean eventually a “good” 1-Bed Condo standard price will be $1MM one day? Maybe… and maybe that will be a base price level where the real estate relevant incomes in Toronto can support the market…

Which would probably make the standard price for a “good” semi $1.5MM and a “good” detached $2MM??? And when I say “good” I mean basically a fairly desirable location, average lot size, parking, and renovated/no work needed.

And then maybe at that point… the market will be in tune with income levels… and maybe at that point we see the real estate market rise in tandem with income (with some minor volatility around the income line, vs clear long term divergence as we have had over decades).

There has to be some point where it does… I’m a bull but I’m also a realist… there has to be a price levelthat strikes some kind of balance or equilibrium with income level where they trend together… unless immigration continues with more and more capital coming into the system… that can always keep prices moving up faster than income.

In my opinion, Vancouver’s prices are always the bar that could be reached in Toronto. So what does a ‘good’ (not full out luxury) 1-bedroom in Vancouver cost today? $750-$800K? So I’d say that’s where we could be.

Condodweller

at 10:50 am

Price levels have been out of touch with income levels for many years now. If you are expecting income levels to balance out with a future 2 million SFH I can tell you it will never happen. Even if incomes were to double it wouldn’t be enough for a dual income household to finance a 2 million SFH and given historical almost nonexistent wage increases where it matters (don’t tell me about recent minimum wage increases) over the past 20 years it’s obviously not going to double anytime soon. In order to achieve any sort of income/price balance, the price would have to come back down.

Having said that, I am not expecting average SFH prices to reach 2 million anytime soon. What I see happening, given the apparent 1 million resistance level is that the price gap between housing types will compress and but up against the 1 million mark. i.e. SHF will be around the 1 million mark, semi around 900k, 2 bed condos perhaps 850k and 1 bed condos around 800k.

One might argue that you would just get the semi over a 2 bed condo for the extra 50k which makes sense, but what if you can’t finance that extra 50k because you are already stretching to pay 800k.

All of this, of course, is assuming that prices stay firm and continue upward momentum. You know how I feel about that from my previous posts.

Kramer

at 12:10 pm

Yes, house prices are detached from MEDIAN income levels and have been diverging for some time.

But why exactly is MEDIAN Income relevant? Why not top 40th or 30th percentile income? Why not the Median Income of the top 500,000 individual income earners in the City? Why, mathematically, is the middle or average number relevant to determining if that real estate market is over or undervalued?

You make it sound like Median Income is chasing house prices (and perpetually losing ground), and it will never catch it, but maybe house prices will fall back to it. This is what everyone sees when they look at that chart, I don’t blame you.

But maybe HOUSE PRICES have been chasing the 25th-to-30th percentile income for decades and still haven’t caught up??????????!!!!!!!!!!!!!!!!!!!

DAMN THAT IS HOT!!!!!!!!!!!!!! AND FINALLY SOMETHING THAT WOULD MAKE SENSE WITH ALL THIS STUPID ANNOYING HISTORICAL “ACTUAL HARD DATA” AND GRAPHS!

I don’t know what the relevant metric is for Toronto, today (i.e. 30th percentile income, 40th percentile income, etc)… But I do know, for a FACT, that it is NOT the same for every city (basically common sense), and is is NOT Median Income for Toronto (because of decades of data).

To determine the appropriate metric, then everything, and I mean EVERYTHING needs to be taken into account. And it is not static, it would theoretically change constantly as all inputs change. And as inputs change, the relevant income metric moves closer to median due to increased headwinds, or toward the right tail of the income distribution as tailwinds increase.

If a real estate market is undervalued, then prices will keep rising until they are in balance with with the RELEVANT income metric for that individual real estate market. And, if real estate market is undervalued, then prices will diverge from irrelevantly lower income metrics, like, in our case, MEDIAN income.

Seriously, how is this not right? Not to have a big head here, but if this starts becoming a topic in the news, you heard it here first people. And I want it to be in the news more than anything just so I stop hearing about IRRELEVANT STUPID ARBITRARY MEDIAN INCOME when it comes to real estate market valuation.

Condodweller

at 4:14 pm

I am not taking the bait on the median income discussion you are duking out in the other threads. You must be over the 100 comment count between the three of you. I never said anything about median income, however, income levels generally must rise for buyers to be able to afford increasing prices.

Kramer

at 4:39 pm

Expand your mind Condodweller… let interesting new ideas in and DWELL on them! And I’m not DUKING IT OUT, I’m trying to present fresh new ideas explaining why things have happened as they have over the past 10 years.

Income IS going up… that’s a baked in point of all this. At the extreme end, do you think that CEO’s salaries have risen at the same pace as median income over the last 10 years? I should hope not because there’s an article every month about CEO salaries skyrocketing. Do you think the other executives who report to the CEOs have had salary growth at the same rate as Median Income? And so on down the corporate ladder…

And when 100,000 new people move into the GTA, and median income stays the even goes up a tiny bit… that means there is a greater number of people at every income level able to afford a home at various price points.

This has all been going on for decades. And people who stare at Median Income are cheating themselves.

Kramer

at 4:42 pm

And whatever the relevant income metric is … i.e. say the 30th percentile income … I would bet that it has been increasing at a faster rate than median income… making it harder for real estate prices to catch up with it over the last decade… This would be supported by the articles citing growing wage gaps, and the disappearing middle class, etc.

Daniel

at 12:16 pm

what about all those condo owners who made big equity gains when condos went to $850k, couldn’t many of them roll their gains into the semis and singles and be easily qualifying.

Appraiser

at 7:31 am

Remember when everyone thought this guy was nuts back in 2015?

“My prediction, and I’ve been pretty accurate to date, is we are going to have a 30-to-40 per cent increase in values of the condo market in downtown Toronto over the next three to four years,”

~Barry Fenton, CEO of Lanterra Developments.

https://lanterradevelopments.com/2015/toronto-condo-prices-could-skyrocket-40-percent-predicts-major-developer/

Keen Observer

at 7:45 am

Yes I do! I even recall one prominent real estate blogger’s opinion on that prediction.

“So let me be the first to call out one of the more outlandish prediction I’ve seen in years: Barry Fenton, President of Lanterra Developments, telling people that there’s going to be a 30-40% increase in average condo values over the next 3-4 years.”

~David Fleming

https://torontorealtyblog.com/archives/13277

Kyle

at 11:49 am

Gotta give credit that he owns it…

“And the last bearish prediction I made – when I slammed Lanterra Developments’ CEO, Barry Fenton, for his 2015 prediction that Toronto condos would appreciate 30-40% in 3-4 years, was in itself, incorrect.

Imagine that.

I finally get bearish on a bullish prediction, and I’m wrong.”

https://torontorealtyblog.com/archives/19825

paul

at 12:32 pm

makes sense the 1 bed condo are hot. minimum wage going up so more competition

Sardonic Lizard

at 11:50 am

>> makes sense the 1 bed condo are hot. minimum wage going up so more competition

You are hilarious.

ed

at 5:55 pm

Kyle, Kyle, Kyle. Chris, Chris, Chris.

The Kyle and Chrissy Show.

steve

at 10:08 pm

So, what/who to believe?

https://www.thestar.com/business/real_estate/2018/02/28/tumbling-toronto-home-sales-signal-a-return-to-normal-market-say-analysts.html

Keen Observer

at 7:14 am

Maybe take the time to read past the headlines?

Mohammad Chaudry

at 3:44 pm

What you think if invest in apartments and what % will get back?

Nicky Breeze

at 8:47 am

I just listed a 750 sq. ft. 1 bed + den condo for $638,000 in Yorkville. At $850/sqft do you think this has missed the mark?

http://properties.gogordons.com/property/20-collier-street-toronto