The topic of renting isn’t nearly as sexy when compared to million-dollar-homes, multiple offers, and bidding wars.

But wait……there are bidding wars on rentals, haven’t you heard?

No joke, no exaggeration – there are full-on bidding wars happening in the Toronto rental market.

So today, let me tell you two stories I heard from my colleagues in the past few weeks, and we’ll go over some slides from Urbanation.ca that tell us what’s going on in the rental market.

Rentals are not my forte. No longer, at least.

I did a lot of rentals when I was just getting into the business; that’s how it works, after all.

I do a lot of rentals on the listing side for my investor clients, but even then, I often tell them that they can use Craigslist and Kijiji to find a renter if they’re willing to put 10-12 hours of work into it, and the renters without representation (ie. no agent, not looking on MLS) are often misguided, and always seem to pay more.

For lessees, I do the odd rental now and again for past clients, but I have nowhere near the stories that some of the kids in my office have.

I’m constantly told, “You have no idea what the rental market is like,” and it’s often coming from a very frustrated agent who is making his or her third or fourth offer with a client. And yes, you read that right – third or fourth offer, to lease.

We hear a lot about that in the market for sale, but it’s happening out there for leases too.

I enjoy the stories, not because I’m a sadist, since all the stories are of the tough-luck variety, but because I want to know what’s going on.

So here are three recent ones that tell a pretty accurate tale…

A young agent in my office has been looking with another young 20-something client for a “lofty unit,” which of course means, in his or her head, the tenant wants that beautiful brick and beam unit that we see in the movies and on TV.

The tenant has lost on two units of a similar variety over the last few weeks, but he’s not exactly out on the street without a lease agreement in hand, you know – because he lives at home.

That’s the case of a lot of these tough-luck renters, who hear the horror stories about what it’s like trying to buy a house or condo in this market, and then find out it’s the same when it comes to leasing.

So a new unit comes out last week in a loft building, and the agent jumps on the phone and convinces his client to go see the unit on his lunch break.

Great move. I love the aggressive decision, and that should be rewarded, but isn’t always, in this market.

By 1:00pm, the agent was back at the office, and had an Offer to Lease signed by the client, and emailed to the listing agent within the hour.

The offer was set to expire at 11:59pm, which is fair, given you can’t really hold a gun to a listing agent and/or landlord’s head in this market, but it also means there are several hours whereby other offers can come in.

That happened to be the case, in the end, unfortunately.

By 7:30pm that night, the listing agent called the young agent from my office and told him that there were six offers on the property – three of them from tenants who were offering sight-unseen.

That means two other would-be tenants rushed over either on their lunch or after work, and put together offers as my colleague’s client had done. But they were competing with those who had completely thrown caution to the wind, and were willing to lease the condo just by looking at the photos.

At $1,700 per month, for a 1-bed, 1-bath, with no parking, the bidding war was in full flight.

The listing agent, who must have felt like a Triple-AAA baseball player getting ready for his call-up to the majors, was working the phones, and working the agents and their clients, and in the end, the unit leased for $1,900 per month. The “winning” tenant also provided four months’ rent up front.

I told the agent, “There’s nothing you can do there,” but then the obvious popped into my head: “I suppose he could have told his client to offer $1,950 per month.”

That’s crazy though, right?

Or is it the same mindset as buying a home?

My second story is even crazier.

It’s not as long, and doesn’t have the panache of a sexy loft, or the jaw-dropping “lease-to-list” ratio of a $1,700 condo going for $1,900, but it’s far more telling of where the rental market is.

Another agent in my office was looking to lease a property for her client, and like the unit above, it was brand new on the market, and relatively sought-after.

She showed the unit very quickly, as did the agent in my first story, and rushed to put together an offer.

She called the listing agent to ask, “If I send this over with a four-hour irrevocable, is that enough time for you to look at it?”

And that’s when the incredible happened.

The agent said, “We won’t look at it tonight. We’re not looking at offers until tomorrow.”

Well THERE you go!

It’s official, folks.

We’re holding back offers……..on RENTALS!

Need you hear any more about the rental market than that?

To have six offers on rental, that’s nothing new.

To pay $200 over the list price for a 1-bedroom, that’s nothing new either.

But an “offer night” for rentals? Refusing to look at offers until a pre-determined day and time?

I think the real estate market has reached a new level. No question.

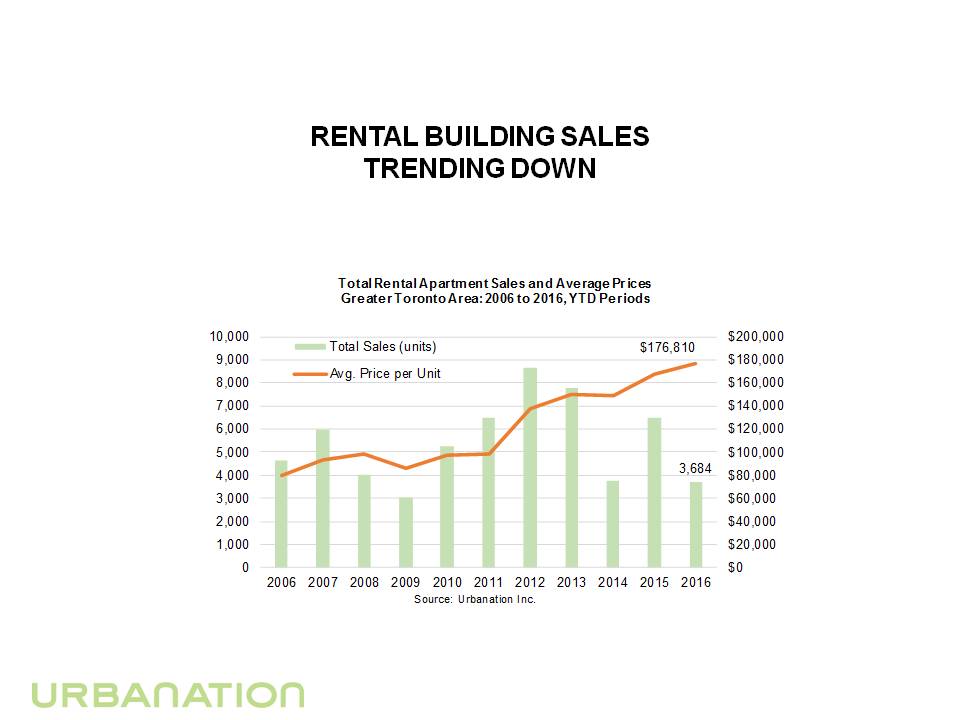

Now as promised, here are a few more slides from Urbanation that back up a lot of what we’re already saying.

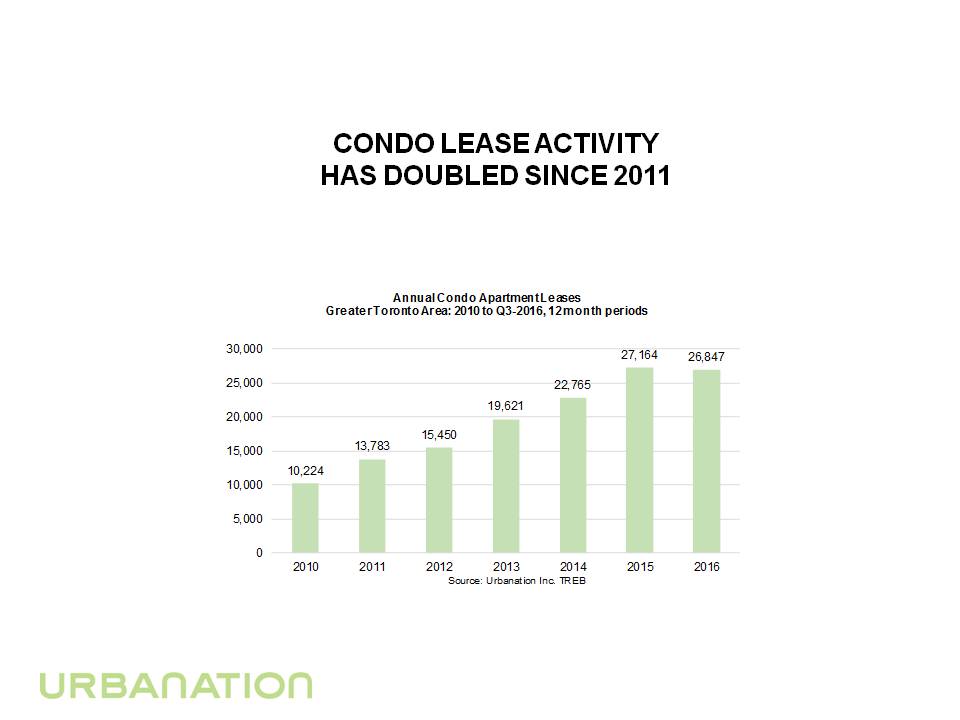

Here’s the lease activity since 2010, which shows that condo leases have doubled in only five years:

This is interesting.

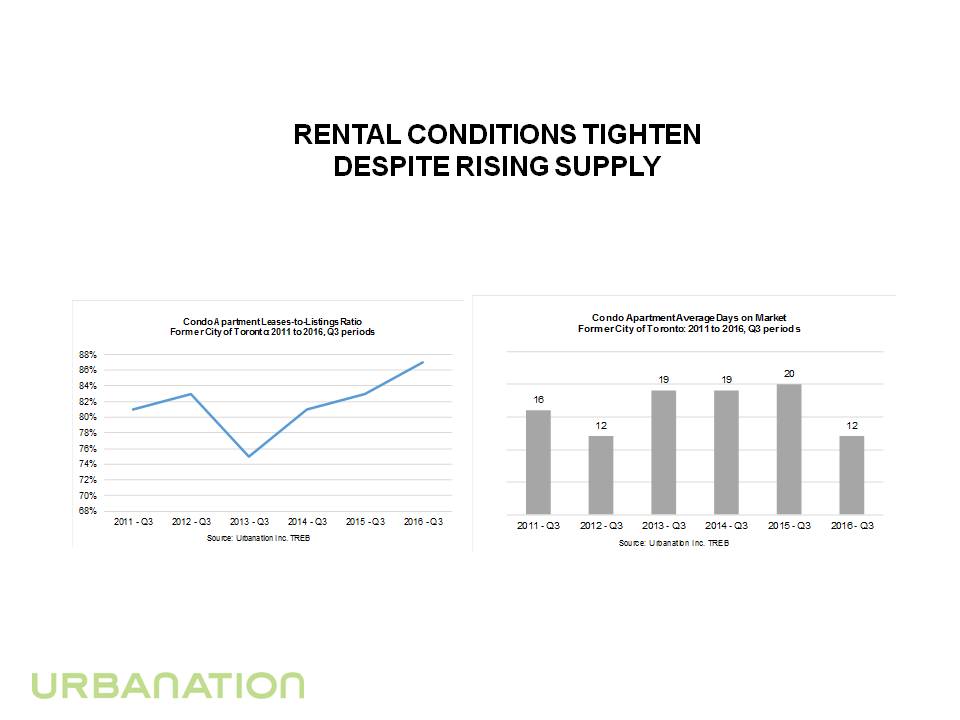

Even though supply has risen, the lease-to-listing ratios are rising:

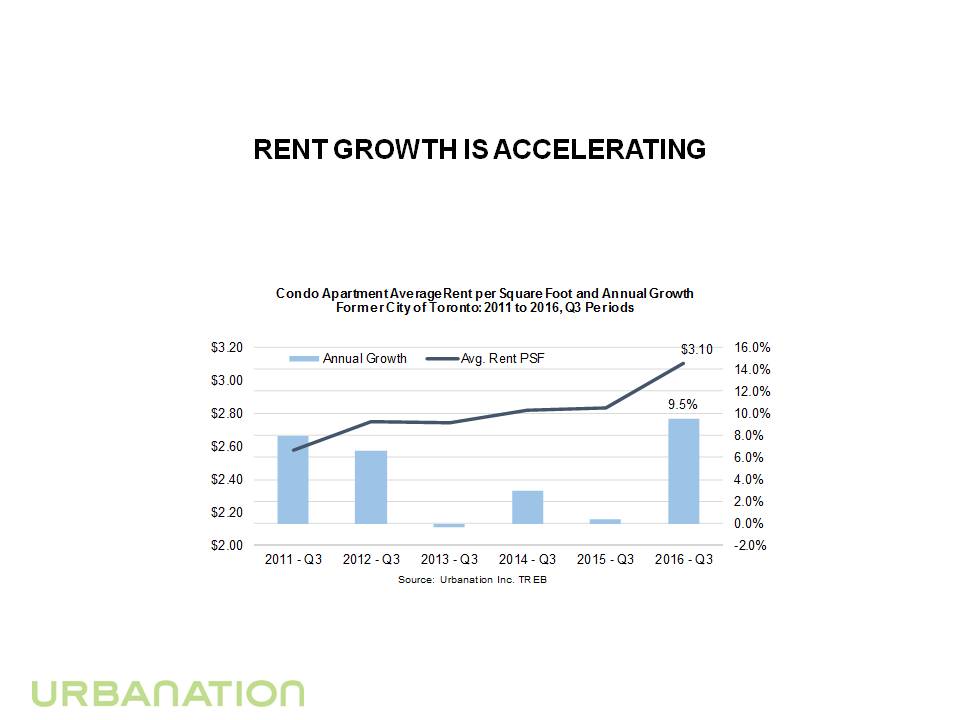

And as you might expect to follow, the average rent per square foot is increasing – almost 10% this year, which is only half of the 20-something-percent increase in the average home price, but still shows you’re not getting a “deal” on the rental market:

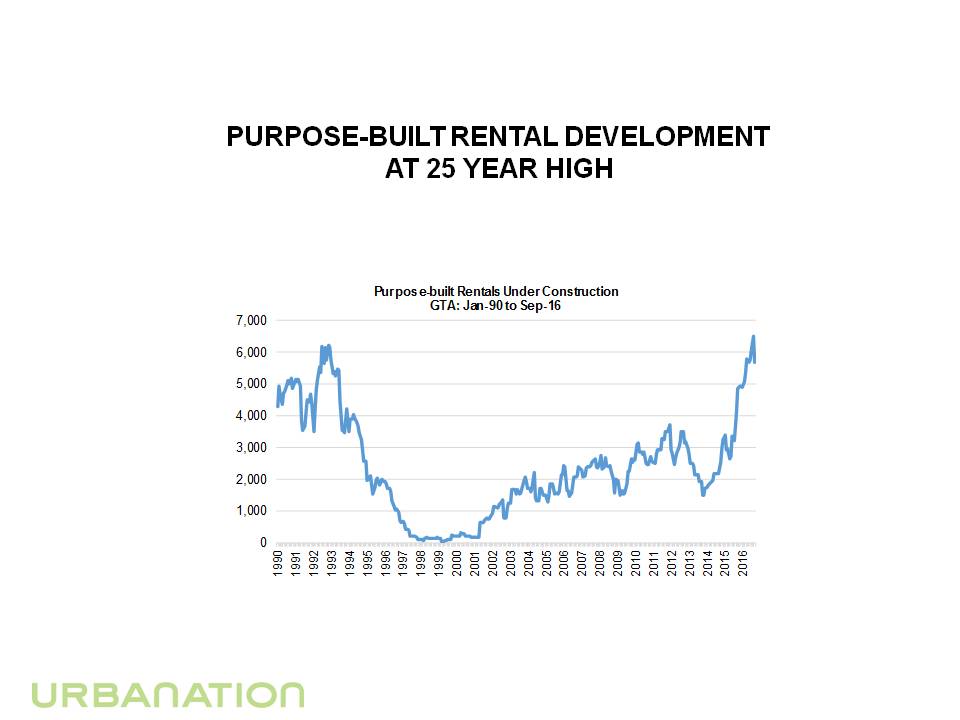

This is also quite interesting, and perhaps a whole other topic – purpose-built rental development is skyrocketing.

You would think that developers want to continue building condos – get in, get out, make money.

That attitude has been a major driver of the condo boom in the past decade, but now it seems developers are turning back to rentals.

I think the major driver behind that trend is the demand from pension funds and other institutions that are extremely long-term focused, who want to own a rental building, rather than a slew of condominiums.

Think back to failed condo developments like “The Selby” which was launched and sold as a condo, but eventually converted to apartments. Same story for “King’s Club,” the infamous debacle by now-bankrupt Urbancorp.

Here are few of the new purpose-built rentals:

And last but not least, the number of rental apartment units has dropped off dramatically, but the price, of course, has continued to rise:

If you’re reading this, and you have a crazy rental story of your own, please share!

Ralph Cramdown

at 8:06 am

Getting into a bidding war for something that isn’t rent-controlled? Yikes.

As for the move to purpose-built rentals, I don’t know. They seemed like a great idea when the consensus was lower interest rates for longer (i.e. last month), but the bigly new theory in the US bond market is higher rates coming soon, with the 30 year moving from below 2.2% in July to almost 3% today — that’s yuuge! Who’s gonna build a tower in Toronto for a 4-5% cap rate (and execution risk) in a rising rate environment? Already-built residential and commercial towers in Calgary are on sale, though.

Kyle

at 9:06 am

Rising interest rates are supportive to rental price increasing.

Ralph Cramdown

at 11:10 am

Partially true. If they’re rising because YOUR economy is improving, then yes. If they’re rising because other large developed market economies are improving and your country’s bond prices are dropping to remain competitive, not so much — though an improvement in the US economy should improve our lot eventually, IF trade conditions remain the same.

Rising rates also depress prices, as new investors demand higher cap rates. If rates rise slowly enough from a reasonably high starting point (with reasonably high inflation), then nominal asset prices don’t fall, and you win. If they go up from 3% to 4% with inflation at 2%, there’s no way rents rise fast enough to cover your loss of equity. For a big investor with 50% leverage and a mortgage locked in for 10 years on a 25 year term, it’s “well, we could have timed that better.” For a small-timer with 20% down and a 5/30 year mortgage, it may mean a cash call from the lender at renewal time.

Kyle

at 11:32 am

When rates go up, the demand for rentals increases, as affordability decreases. Real estate investors take the long view, they are not watching their short term equity fluctuations, if you’re a big investor you mark your book once a year for financials, if you’re a small investor you don’t even bother getting your placed re-assessed.

Appraiser

at 9:56 am

@ RC:

The greater golden horseshoe and the GTA in particular are bullet-proof. Time for denial is over Ralph – throw in the towel already, it’s been a long, long time after all. GTA is on fire. Record sales EVERY month this year on TREB. Record prices to go along with. Rental market is ‘smokin hot (see above).

Open your eyes Ralph. Slightly higher rates will have no effect here in an undeniable seller’s market where listing inventories are at all-time lows and days on market continue to decline. It would take a 300-400 basis point rise in rates just to “normalize” this market.

Keep dreaming Ralph.

Ralph Cramdown

at 11:13 am

Careful what you wish for. You know what happens when the last bear throws in the towel, right?

Appraiser

at 11:28 am

Well at least get it out of the linen closet. Long…long… time…

David

at 3:55 pm

How about a 100BP rise in unemployment? That would make a much bigger impact.

Interest rates go up = people become more house poor. They start shopping at No Frills instead of Whole Foods. Walmart instead of MEC. Pizza Pizza instead of CIBO. You get the idea. For sellers who have a price in their mind – they just don’t sell unless…

Someone loses their job? Unless they have a lot of savings on hand, mortgage payments can’t be made. Houses then HAVE to be sold.

That is what is going to kill the market. Unemployment, not interest rates.

Condodweller

at 11:07 am

I disagree. I think it is interest rates that are going to kill the market and here’s why:

1. Despite what most people think, higher interest rates are a sign of a good or at least improving economy. With improving economy we should see job gains, not job losses. With the recent surprise of market action in bonds, it does look like rates are going to be moving up.

2. With a stable jobs scenario and rising rates it’s just a matter of time before people can’t meet their mortgage obligations. Yes, I am well aware people can cut back spending and use savings for a while but there is a limit to that. Remember that 50% of Canadians can’t meet their financial obligations if they lost their job today as it is today. Also keep in mind that percentages magnify the amount with higher mortgages i.e. with high mortgages incremental interest increases will take a larger bite out of people’s savings, forcing them to cut back further which is going to mean that people will HAVE to start selling their houses.

I know it’s going to be a small percentage but we only need a few to break the dam.

Of course the question is when it might happen, and it may well take years but that’s how I see it unfolding. Obviously this is barring any black swan events which could cause sudden job losses at any point.

I agree that job losses will be a big negative for the market if and when it happens, however I think it will be interest rates that will do it first.

Shields up! 🙂

TorontoBallerz

at 2:34 pm

@Appraiser

With an average price of 1.3M, if it keeps increasing at 20% annually, then after 10 years your average house will be $8M!!! The big question is what will you be doing with all your extra cash?

Joe Q.

at 8:59 am

David, is the rental data from Urbanation collected from MLS, or from another source?

David Fleming

at 10:54 am

@ Joe Q.

From what I understand, Urbanaton has access to a lot of data outside of of MLS.

That’s their competitive advantage – they’re not just re-purposing the same data everybody else has.

They have stats on pre-construction numbers (and demographics such as investor-owned, foreign-owned), not to mention rentals which surely is not MLS-exclusive.

Wilson

at 9:21 am

Bully offers on rentals will be next.

Condodweller

at 11:09 am

Increased interest in rentals is not surprising given owning is becoming out of reach for more and more people.

Kramer

at 3:41 pm

David,

By now there are plenty of 55 year olds thinking about retiring early and blowing town for a house on easy street.

Is there any analysis pointing to a period in the not too distant future when a large range of baby boomers are going to flood the market with listings of $1.2MM 1800 Sq. Ft houses? Has this been looked at? Is this all in my mind?

Kyle

at 5:21 pm

I’m not David, but i’ll share a personal anecdote. About 13 years ago i owned a house in an old money enclave, where the Olde English stone and brick homes on sweeping lawns were all owned by couples whose kids were just about ready to go off to University. What happened over those 13 years is what i think has or will repeat across the city. A few of those older couples have kept their homes, because those University students returned and still live with them or because they’re just attached to their homes. But many of those older couples have already sold and moved to nearby luxury condos. Many new families have already taken their place in those big old homes. Basically, because the boomers have already or are gradually transitioning their housing over a decades long period, IMO there isn’t a flood on it’s way, more like a gradual fade for the remaining older home owners.

Kramer

at 8:17 pm

I’m happy to hear that viewpoint.

And I suppose there is also the old argument of whenever a $1.5MM house is sold, the proceeds are going somewhere – into the condo market, into the economy, into inheritance and back into housing, etc. If this happens gradually it will only keep the cycle going.

Until rates normalize… which is clearly not going to be for a long time.

Or until unemployment spikes as David mentioned below.

crazyegg

at 10:27 am

Hi All,

Raising Interest Rates:

The impact on this will be even higher rents for renters.

Banks are passing the buck onto investors with upping the prime out of step with the BofC. In turn, landlords will naturally pass amount (and more) this onto their renters. Rent controls do not apply to condos built after 1991.

I would hate to be renter now. But it is prime time to be a landlord now. This is capitalism “at it’s finest”.

Regards,

ed…