Have you ever gone on your loved one’s laptop browsed random internet pages, just to see which ads pop up?

I haven’t. But it might be an interesting experiment.

The “cookies” and “tag marketing” that follow us around the web are downright scary.

Every page I visit on the Internet now has advertisements for autographed hockey pucks and vintage sports cards for sale on eBay. It’s just amazing how well the internet knows me and my habits.

Sometimes, I don’t know whether I’m viewing an article because it’s organic or because Mr. Robot and his team are force-feeding me news.

But in the past few days, all I’ve been reading about is interest rates.

This started on Wednesday, although the Bank of Canada’s next announcement on rates isn’t until December 4th. So either the media is getting out well, well ahead of this announcement, or it’s just a really popular topic.

Are you familiar with “Posthaste?”

It’s a regular column in the Financial Post, and I find it to be the perfect combination of news and opinion.

This appeared in the Financial Post on Wednesday:

“POSTHASTE: The Real Reason Bank of Canada May Stay On The Sidelines For Awhile”

Financial Post

November 27th, 2019

The theme in this column seems to be that if rates aren’t cut, house prices have nowhere to go………but up.

From the article:

Growth is likely to slow more than the Bank of Canada expects in the fourth quarter and the labour market is softening, but another issue looming on the horizon may give the BoC reason to keep its powder dry, say economists.

Capital Economics estimates that the unseasonably cold weather, Keystone pipeline outage and CN Rail strike alone could shave 0.3% off GDP for November, slowing growth to 0.8% annualized in the fourth quarter, lower than the Bank’s forecast of 1.3%. That would appear to leave the door open for a cut, but there’s another concern.

“While the Bank’s inflation forecasts make a convenient excuse, it’s pretty clear that the real reason why the Bank hasn’t cut interest rates is its fears about pouring further fuel on the resurgent housing market,” said Stephen Brown, Capital’s senior Canada economist.

Capital says housing price momentum is building quickly, with monthly gains of 0.5% month over month in each of the past three months. It estimates that if that continues, by March house price inflation will be near 5%.

Remember back in July when I wrote “What Happens If Interest Rates Don’t Rise?”

In this blog, I referenced a Reuters poll of economists that showed 40% of those surveyed expected at least one rate cut by the end of 2020.

Earlier in the week, another Financial Post article explained that predictions for interest rate decisions in 2020 have changed substantially.

“Bank Of Canada To Hold Rates Through 2020, Call On A Knife’s Edge”

Financial Post

November 26th, 2019

From the article:

The Bank of Canada is now expected to hold rates through to the end of next year, according to a slim majority of economists in a Reuters poll, with forecasts on whether or not the central bank holds or cuts sitting on a knife’s edge through 2020.

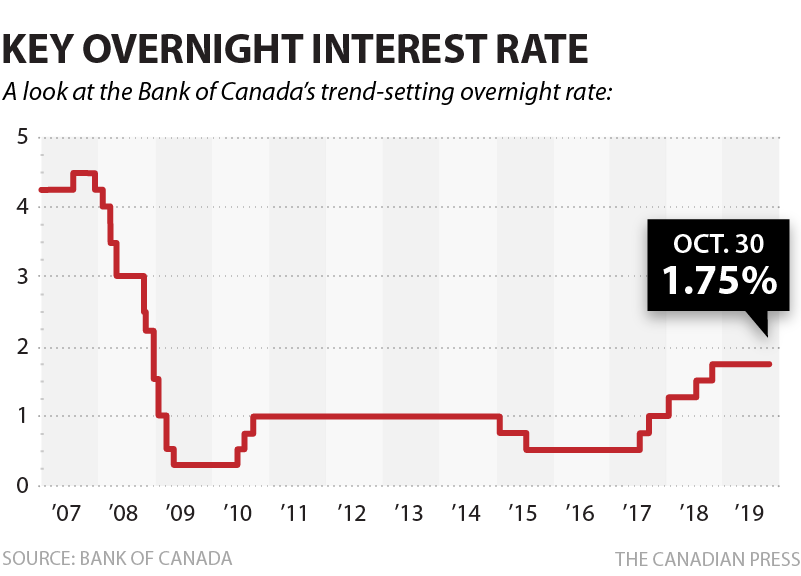

The latest Reuters poll of over 30 economists taken Nov. 19-26 showed the BoC will hold its key overnight interest rate at 1.75% this year and next, flipping from equally narrow expectations for a rate cut early next year in the last poll.

That change in expectations was primarily driven by comments from BoC officials – Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins – who spoke last week at separate events about Canada’s monetary conditions being “about right” despite global trade tensions.

Every respondent in the poll expected rates to remain on hold at the conclusion of the BoC’s Dec. 4 meeting, in line with market expectations..

When asked if the Canadian economy actually needs a rate cut before the end of next year, a slim majority of economists – 13 of 24 – said no. Just a month back, a similar set of economists were slightly inclined toward a cut.

Now I don’t want to draw a correlation between interest rate expectations and some of the real estate forecasts our there, but I can’t help but notice a general bullishness in the real estate market.

I know, I know, there are still those of you waiting for the crash.

An agent in my office was telling me yesterday about his sister’s husband, who in 2016, said “Prices are coming down, we’re going to rent.” They’ve been renting now for over 3 1/2 years, and recently they started their search again, only to abruptly put it on hold when they found that market conditions weren’t to their liking. Their reasoning? “Prices are going to come down.”

That’s the excuse of every person who can’t afford real estate, can’t justify the price, can’t get what they want, etc., etc., etc.

So what do they think of headlines like this?

“Canadian House Prices ‘Set To Surge’ In 2020, Forecasts Say”

Huffington Post

November 27th, 2019

From the article:

The most optimistic forecast (or the most pessimistic, if you’re hoping for lower prices) comes from Capital Economics, which in a report last Friday said “momentum is building” in house price growth. If things stay at their current trend, house price growth will be running at an annual rate of 6 per cent by March of next year.

“The rise in the sales-to-new listing ratio suggests that house price inflation will surge,” senior Canada economist Stephen Brown wrote.

The sales-to-new-listing ratio measures how many houses are selling against how many houses are coming on to the market. The higher the ratio, the tighter the market, so the larger the price growth you can expect.

Though it varies from market to market, in general a ratio above 60 per cent suggests price hikes ahead. According to data from the Canadian Real Estate Association, that ratio was 63.7 per cent for the country as a whole in October, well above the 54 per cent long-run average.

Brown said the increased demand for housing comes from “a combination of (lower interest rates) by central banks elsewhere in the world and expectations of interest rate cuts in Canada.”

The best rates available for a five-year fixed-rate mortgage at the major banks fell to around 2.7 per cent today from 3.5 per cent at the start of this year, Brown said, citing data from RateSpy.com. The lower rates mean Canadian buyers can afford about 10 per cent more on the purchase price of a home than they could a year ago.

Now we all know that lower interest rates generally lead to higher real estate prices.

But the Bank of Canada’s decision on whether or not to cut, hold, or raise interest rates doesn’t revolve around the real estate market. It’s based on far broader implication for the entire economy and the well-being of Canadians from coast-to-coast.

A recent speech by Carolyn Wilkins, the #2 at the Bank of Canada behind Stephen Poloz, was profiled in another National Post article which you can read HERE.

Interest rate policy seems to be more geared toward household debt and inflation than anything else. Although in recent years, trade has become a major factor, thanks in part to our neighbours down south and their policies, as well as the reactionary policies that resulted around the world.

This excerpt from the article sums it up nicely:

“The Bank of Canada and other authorities must assess the risks and have the right safeguards in place,” Wilkins said. “Ideally, you want to put the winter tires on before the snow falls. It not only protects you, but also everyone else who’s on the road.”

Wilkins acknowledged the possibility of a slowdown, telling her audience that even if the trade wars stop getting worse, they still could result in US$1 trillion of lost global economic output by 2021. But for now, the central bank remains extremely reluctant to do anything that would cause companies and households to add to an already menacing pile of private debt.

Lower interest rates might offset some of the anxiety over trade heading into next year, but only at the expense of sowing the seeds of a new financial crisis down the road. Poloz’s Bank of Canada approaches policy as an exercise in risk management, and at the moment, policy makers think an interest-rate cut would ultimately do more harm than good.

“With vulnerabilities high and inflation close to target for more than a year, we said at our most recent interest-rate decision that taking out insurance wasn’t worth the cost at that time,” Wilkins said. “We also said that in considering the appropriate path for policy, we’d watch how the trade situation and household vulnerabilities evolve as well as fiscal policy developments.”

Currency traders who keep losing money by basing their bets on verbiage would do better by following developments related to those key points: household debt, inflation, trade and government spending.

The line that speaks volumes, in my opinion: “policy makers think an interest-rate cut would ultimately do more harm than good.”

It seems as though in May of 2019, more economists thought Canada was not only headed toward a rate cut in 2020, but that the economy could handle it. As was noted in my blog post from July, four out of five of the major banks thought a rate cut was coming in 2020.

But today, as we approach the end of 2019, it seems as though a rate cut is far less likely, and from what I’ve been reading in the past week, it feels as though a cut would put the economy at risk.

We also don’t think a rate hike is in order either.

So could we see rates remain flat for an extended period of time?

The current rate of 1.75% has been in place since October 24th, 2018. We’re now at 13 straight months, with no hike or cut on the horizon.

If we actually did make it through the end of 2020 with no adjustment in the overnight interest rate, this would represent 26 months with no change.

But you know what?

26 months is nothing, if recent history is any indication.

Does 2010 to 2014 ring a bell?

On September 8th, 2010, the Bank of Canada raised the overnight lending rate from 0.75% to 1.00%.

This rate remained in effect until January 21st of 2015.

For over fifty-two months, we saw the rate remain exactly the same.

So is it that unreasonable to assume that the current rate of 1.75% could remain in effect through all of 2020, and perhaps even longer?

That’s my honest prediction, and recall that I said a cut was coming well before a hike. I still stand by that, but I too have to back off the idea of a cut.

I’m sure I don’t have to tell you how I feel this will impact real estate prices…

Have a great weekend, everybody!

Appraiser

at 10:17 am

Low and steady interest rates, under-control inflation, low unemployment, 4% annual wage growth, steady population increases and low listing inventory, all point to future increases in real estate prices in the GTA.

Not to mention burgeoning pent-up demand due to the artificial demand dampener (mortgage stress-test).

Bal

at 11:31 am

No recession in sight?

Gary

at 11:38 am

Forecasts may tell you a great deal about the forecaster; they tell you nothing about the future.

-Warren Buffett

Bal

at 11:54 am

I guess as long as no Recession…everything will stay peachy….

Appraiser

at 6:07 pm

No recession in sight.

Appraiser

at 6:08 pm

I’ve been right for 33 years in a row. How about you? Still waiting for the crash?

Bal

at 6:26 pm

Naa I am waiting for nothing…i already got my house.

Bal

at 6:44 pm

33 years in Row…wow….pretty confident or overconfident…

condodweller

at 1:20 am

33 years takes you back to 86. Did you sell all your real estate holdings in 89 and bought back in 90, no wait..91, no wait..92..93..no..94..95……right, the market went down for 6 years straight so being the eternal optimist and bull you would have been wrong for 6 years. We don’t hear you bragging about that.

Bal

at 9:02 am

:)…..maybe because he knows that will never happen again….as that was caused by higher interest rates….

Professional Shanker

at 11:07 am

Keep him honest Condo with actual facts! Appraiser pats himself on the back for merely owning property since the early 2000s, so everyone who is 45+ is a genius and is “right”.

What are the chances he is less exposed to RE than some bears on this site?

Osama

at 5:28 am

Mobile Phone Repair In Toronto

https://110wireless.ca/