Friday’s post was fun, right?

I got to hear from two people who were involved in the story, the readers seemed to enjoy it, and only a handful of comments were from naysayers.

Then again, we need the naysayers to balance the debate, that is, if there is a debate…

If you’re like me, you’ve been waiting desperately to sink your teeth into the November TRREB numbers just to see if certain parts of the market, whether you’re basing it on October’s numbers or the last six months’ numbers, are for real.

One reader commented last week that the November condo numbers in the 416 would “not be pretty.” That reader was correct.

I’ve been waiting to look at rental figures, since I think that’s having a massive effect on the overall condo market.

And as far as the freehold market goes, the feeling of weakness in some segments of the market, I do believe, is due to listing price and strategy, and not a decline in prices.

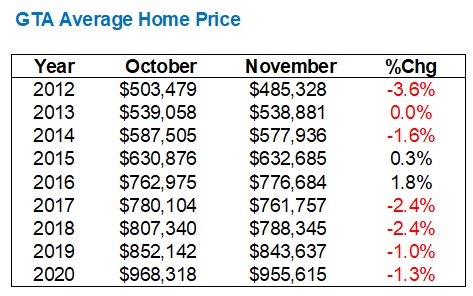

So let’s start off with the average home price in the GTA, which I think is most people’s go-to.

This past month we saw a modest decline in the average home price as follows:

Recall that the “peak” in April of 2017 was just over $920,000.

Also recall that when we saw a pre-pandemic “peak” of $910,290, many armchair quarterbacks thought we wouldn’t see that price again for years.

Starting in June, we saw five straight all-time record prices. And while the $955,615 average sale price recorded in November represents a 1.3% drop month-over-month, it’s still significantly higher than the pre-pandemic “peak.”

Now, seasonal variations have to be taken into consideration here, so I’d like to look at the percentage of increase, year-over-year, for each month in 2020 just to see how that changes our opinion of the last few months’ activity:

The eye is automatically drawn to the 0.2% and 3.0% year-over-year increases in April and May, and for good reason. Those were tough times, no doubt.

But as we figured out how to live in a society during a pandemic, and as some semblance of normalcy returned, the market returned as well. And then some.

The year-over-year increase in June of 11.8% trailed the busy months of February and March, and that led to an even busier July, and a downright frenetic August. I can tell you from personal experience that August of 2020 was the busiest month of my 17-year career, and so I find it ironic that the year-over-year “peak” in price increases seems to fall in that month.

What we’re seeing here is the classic “increase, at a decreasing rate.”

Yes, the average home price went up for six straight months from May to October, and yes it actually declined in November, but if you look at year-over-year increases as a statistic, you can see that while the price itself peaked in October, the year-over-year increase peaked in August. If we’re adjusting the market for seasonality, it looks like the market has essentially been slowing since August.

And what should we expect in the month of November?

I’ve shown you this before….

Only twice in the last nine years has the November average home price out-paced October, so it comes as no surprise that we saw a drop this past month from $968,318 to $955,615.

Now, what do we make of the sales figures?

First, look at the number of sales in November: 8,766.

This represented a massive 17.0% drop from the 10,563 in October, but again, what should we come to expect?

First and foremost, let’s look at past sales in the month of November:

2012: 5,793

2013: 6,354

2014: 6,476

2015: 7,385

2016: 8,503

2017: 7,374

2018: 6,206

2019: 7,090

2020: 8,766

Alright, then! So we’re looking at a record month?

It would seem that way. And this is why noting the 17.0% decline in sales from October to November, and drawing any negative conclusion, is misguided.

But how does the 17.0% decline from October to November stack up against previous years?

Important to note: 2017 is not a typo. Remember that the market fell off a cliff in April and then slowly climbed back, so that 3.6% increase is a severe outlier but is, in fact, correct.

Ignoring that outlier, we see that sales drop from October to November, every year, and ignoring 2017, the average decline is 17.3%.

So this past November, sales did exactly what we should expect them to do.

Now, what do we make of inventory?

First, let’s look at new listings in the month of November as we did above with sales:

2012: 9,838

2013: 9,281

2014: 8,716

2015: 9,609

2016: 10,456

2017: 14,349

2018: 10,538

2019: 8,650

2020: 11,545

Perhaps not the same pattern here?

Again, recall that 2017 was that insane year where we saw huge inventory after the market decline, so that record of 14,349 new listings in November of 2017 isn’t a surprise.

But also note that there were only 8,650 new listings in November of 2019, so when we see the big, bolded, +33.5% in TRREB’s report for “Year-Over-Year Increase in New Listings,” the only reason why that number stands out is because of the slow market in 2019, and not a busy market in 2020.

To take away that the month of November saw “huge” inventory based on that figure would be incorrect.

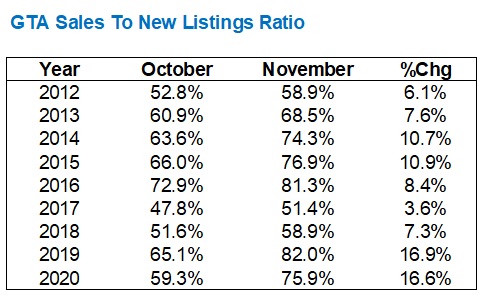

So now let’s put these two together and look at the sales-to-new-listings ratio, which is a measure of the rate of “absorption” of inventory.

Here is the SNLR for November over the last nine years:

2012: 58.9%

2013: 68.5%

2014: 74.3%

2015: 76.9%

2016: 81.3%

2017: 51.4%

2018: 58.9%

2019: 82.0%

2020: 75.9%

What jumps at you?

Well, once again, I’d have to start with that crazy year of 2017! An SNLR of merely 51.4%, down from 81.3% the year prior, was because of the change in the market that spring.

But I would also point out that the nine-year high was last year! That’s 82.0% in November of 2019, which explains why prices jumped significantly in January, February, and March of 2020. The market dried up toward the end of last year, and all of those holdover buyers hit the ground running in the new year.

Another way of taking this past month’s sales activity into context is to look at what usually happens between October and November with respect to SNLR, and then compare.

Make sense?

What do we make of this?

The sales-to-new-listings ratio typically increases from October to November, which it’s done every year in this nine-year period.

While sales do slow down, as we saw above, listings don’t slow down at the same rate, but rather slow down at a higher rate.

So declining sales, combined with declining listings – at a higher rate, means the sales-to-new-listings ratio will increase from October to November.

The 16.6% increase from October to November is just off the “peak” in 2019, and given how frenetic last fall was, I find it very interesting that 2020 has kept pace. The “feel” out there in the market right now is nowhere near the same as it was in 2019. The condo market is performing poorly, the freehold market can be spotty in certain areas, and all told, it feels much slower than last year. Perhaps these numbers are a sign of things to come in early-2021?

There are two more things that I want to look at before I break and come back to these stats on Wednesday:

1) TRREB district average home price through September, October, November,

2) 416 average home price by property type through September, October, November

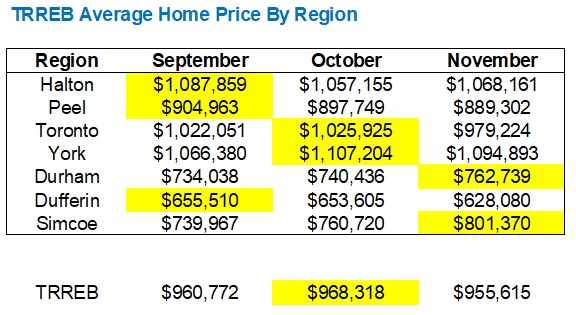

First, we’ll take a look at the average home price in each region.

There’s been a lot of talk about 905 being red-hot this fall, and I’d like to see where these figures land, and then compare them to the TRREB overall average.

The peak month for each region is highlighted in yellow:

This is interesting.

Of the seven regions, three saw a peak in September, two in October, and two in November.

And if we look at the largest areas (Halton, Peel, Toronto, York, Durham), the delta on these is negligible.

The drop in average in the 416 (Toronto) from $1,025,925 to $979,224, a decline of 4.6%, is the largest drop of the group.

Halton actually saw a higher price in November than October, but the decline from October to November was still only 2.8%

Peel region has operated in a very small band from $889,302 to $904,963, for which the 1.7% delta is essentially a rounding error.

York region saw a large 3.8% jump from September to October, before coming down slightly, and now the November price is merely 2.7% off from September.

And Durham, the only region to “peak” in November, is up a 3.9% since the start of September.

All in all, no major shifts here, save for perhaps the drop in the 416 from October to November.

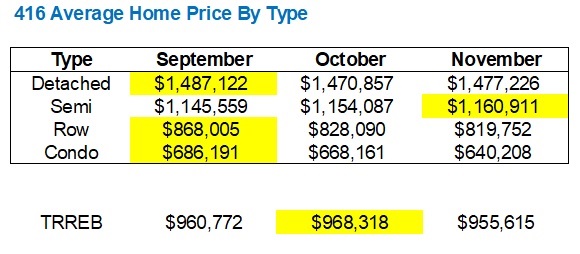

So now let’s look at the 416 specifically and analyze the average prices for each of the four major property types in the same months:

This is fascinating – the “peak” came in October, at $968,318, but the peak for 3 of 4 property types came in September. In fact, the other property type peak, semi-detached, came in November.

How can the overall price peak in a month when none of the individual property types saw a corresponding peak?

Well, I would argue the answer is the small delta.

Detached prices operated within a very small band: from a low of $1,477,226 to a high of $1,487,122. That’s literally ten thousand dollars! The three prices fell within 0.6% of one another. Average home price by property type often sees some vicious swings, month-to-month, so this is quite fascinating to see a $10,000 delta.

Same story for the semi-detached, however, where we see a range of $1,145,559 to $1,160,911, only 1.3%

The rowhouse prices saw a much larger range, about $60,000, which is surprising.

But it’s condos where my eye is really drawn, especially since the drop is so pronounced: from $686,191, to $668,161, to $640,208. That’s’ a 2.6% drop into October followed by a 4.2% drop into November.

Overall, the average condo price dropped 6.7% from September to November, on paper, at least. In practice, is a $500,000 condo in September now worth $466,500? No, it’s not. But it’s worth less, that, I believe unequivocally.

The condo market took it on the chin in the latter three-quarters of 2020, but there is light at the end of the tunnel.

And that’s where I’ll pick it back up on Wednesday as we spend the whole post looking specifically at the condo market…

Appraiser

at 8:32 am

Excellent analysis. Two things I’ll comment on:

“The condo market is performing poorly, the freehold market can be spotty in certain areas, and all told, it feels much slower than last year. Perhaps these numbers are a sign of things to come in early-2021?

The condo market took it on the chin in the latter three-quarters of 2020, but there is light at the end of the tunnel.”

Very perceptive.

The condo market once again proves to be almost invincible (puts one in mind of Mark Twains famous cable…”The reports of my death are greatly exaggerated.”

Also, a levelling-off of the current low-rise market fury might be prudent.

I prefer CEO of Mattamy Homes’ Peter Gilgans take on the long-term view of the real estate market:

“A moderate level of inflation in real estate prices is very good and very healthy. It’s been a huge contributing factor to building this country over the last century, to inspiring people to own their own homes and working that little bit harder to achieve that. I’d like to see it remain like that. ”

https://www.cpacanada.ca/en/news/pivot-magazine/2020-05-06-peter-gilgan-interview

J G

at 2:09 pm

Back on Apr 24th 2020, I predicted 416 condo market would drop by 20% from the Feb high of 727k (median-price per HouseSigma).

https://torontorealtyblog.com/blog/interview-with-ben-rabidoux/

Even Dave was skeptical when he had the interview with Ben Rabidoux a couple of days later. Take a look now, it’s at -15% and decreasing. Preliminary December numbers look even worse.

https://housesigma.com/web/en/market?municipality=10343&community=all&house_type=C.&ign=

Rents have absolutely plummeted, basically at 2016 levels. Check on Kijiji or FB Market place. Most investor who bought in the last 3 years are cashflow negative.

Prices have held up a bit better, although good downtown units selling at $900-950/psf is the norm. I wouldn’t be surprised if it continues to fall into the $800’s/psf range.

Chris

at 10:18 am

Speaking of Ben Rabidoux, his contribution to Maclean’s annual “Charts to Watch” was on the topic of the Toronto condo market:

“Things will eventually improve as immigration picks up in 2021 and the surplus of rental supply is worked off, but trends may get worse before they get better. There are still just under 12,000 whole-unit Airbnb listings in Toronto, some of which will certainly find their way into the long-term rental market as the city moves to restrict usage. In addition, 70,000 apartment units are under construction across the GTA, with 2021 set to see a potential record number of new completions. Roughly half of new condos end up in the rental market at completion, so there’s plenty of new supply that will need to be absorbed.”

https://twitter.com/macleans/status/1336041540142182401

J G

at 1:29 pm

I agree at some point 416 condo will start to recover, it could be as early as next Spring. However, if you compare with the stock market (which has been on absolute fire since April), then it’s clear condo investors with all their capitals tied up have lost out.

For example, if you were lucky enough to buy Tesla earlier this year, you would have 9Xed (!!!) your investment. Yep, if you invested $10k in Tesla stock in March or beginning of year, it would be $90k today on Dec 7th. Fun year eh?

Professional Shanker

at 2:13 pm

Did you buy Tesla?

J G

at 2:23 pm

I did, but not $10k.

J G

at 2:33 pm

Btw, I personally don’t recommend buying Tesla at the current level. However, I was wrong about this before, as I would have bought way more than $10k if I had known 🙂

Chris

at 2:29 pm

“Stocks, real estate, gold and bitcoin hitting new highs during a recession. Fiat currencies are being debased at an impressive pace.”

– Steve Saretsky

https://twitter.com/SteveSaretsky/status/1336358822965755905

Seems the only asset not appreciating these days is a condo.

J G

at 1:35 pm

Sorry I forgot to mention, one more thank you to Appraiser for “dead cat bounce” comment (referring to stock market) back in April!

Chris

at 2:56 pm

His “caution against being caught in a bull trap” was on April 7th.

From that date to today:

DJI +32.74%

S&P500 +39.41%

NASDAQ +59.67%

TSX +29.66%

TREBB Composite HPI +3.72% ($870,100 in April to $902,500 in November)

https://torontorealtyblog.com/blog/join-the-conversation-qa-session-episode-2/#comment-118577