Newspapers, magazines, the 6pm news, social media – everywhere I look, I see “predictions” and “forecasts” for the 2015 real estate market.

I know it makes headlines, and there’s definitely genuine interest from readers and watchers, but do these “outlooks” and “prognostications” have any merit?

What good are predictions if they’re not based on anything, and more to the point, what do we make of a prognosticator if his or her past predictions have held no merit? Shouldn’t they be judged by their track records?

As I said at this very time last year, I’m not one to make predictions. But as we start 2015, I do want to look back at some predictions and see how they panned out…..or didn’t….

Ah yes, 2015!

A magical year!

I have wildly high expectations for 2015, but one thing I know I’m almost guaranteed to experience during the next twelve months is a good old-fashioned hover-board chase:

Yeah, I know, I’m a bit late to this party.

For weeks, we’ve been hearing about how “Back To The Future II” was a look ahead to the year 2015, when the Chicago Cubs won the World Series, where cars didn’t need roads, and where hover-boards were all the rage.

But I’d like to think I was the first one to think of this, mid-2014, while watching the movie on a lonely Saturday night on TNT. Why didn’t I just rent it for four bucks and skip the commercials, you ask? I’m not sure….

So if there’s one thing we learned from looking back at Back To The Future II, it’s that even if you’re as intelligent and qualified as a Hollywood screen writer, you might not be able to see into the future.

There are other examples not being able to accurately see into the future, of course, especially when it comes to real estate!

Just take a look at this prediction from March of 2008:

“I bought a home in Leaside in 1995 for $540,000, which just changed hands for $1.3 million. It’s on a 30-foot lot, with no garage and a driveway so narrow the car door scrapes on the neighbours’ decorative stones when you exit the vehicle. The backyard has zero privacy and the street is cluttered with construction vehicles as bungs are torn down for McMansions.

But, for some reason, people think it’s worth putting their entire financial futures on the line to live there, and that the houses will be worth $2 million in another five years, which is absurd.”

That’s great stuff!

Except the prognosticator was wrong, not only about the $2 Million mark being “absurd,” since these houses are now trading for up to $2.3 Million, but also wrong to sell his home for a paltry $1.3 Million when he could have made another $1 Million, tax free!

Well, it’s not like this person has legions of followers, has written books on the subject, and constantly gives seminars where he advises people not to buy real estate, but rather invest their money with Turner Investments and Raymond James Ltd.

Oh, wait. That’s incorrect. Since the quote above is from one of Garth Turner’s 2008 blog posts.

Remember his book: “The Greater Fool: The Troubled Future Of Real Estate?”

He predicted, among other things, that the Toronto real estate market could correct up to 25%.

At the start of 2008, the average price of a Toronto home was $376,236.

At the end of 2014, the average price of a Toronto home was $567,198.

That’s, on average, an increase of $190,962, or 51%.

This also represents a tax-free capital gain.

So if you were “Joe Average” who started 2008 and read, and took to heart Mr. Turner’s comments, you’d have lost out on a $190,962 capital gain, which probably takes about $250,000 worth of income to generate. And at $250,000, with the average salary of a Torontonian being under $50,000, it means you’d have to work for free for FIVE YEARS to make back the money you “could” have made if only you’d bought a home.

It could be worse, of course.

You could have been more than Joe Average – you could have been the person who emailed Mr. Turner in March of 2008 to ask whether or not you should buy that Leaside house, and you could have lost out on a $1,000,000 tax-free gain, possibly while throwing your money away renting.

Anyways, I didn’t mean for this post to hammer on Garth Turner. I think enough people have been doing that over the years, especially after he bought BACK into the Toronto market in 2013 for $1,700,000…

My point to this is that nobody, not Hollywood writer Robert Zemeckis, nor real estate “guru” Garth Turner, can see into the future.

And I’ve been wrong a few times myself.

Like this, from a blog post I wrote at the start of January, 2013:

“By the end of 2013, we’ll have seen stagnant growth. I think on average, the Toronto market might lose 3-4%, and might gain 3-4%, but that’s about all I see for the market as a whole.”

Stagnant growth? I was clearly wrong, as the 2013 real estate market went up 5.2%.

I was a bit wishy-washy two years ago:

“I do not think the real estate market is going to implode like so many pundits, and I think by now, you all know that I’m an honest enough guy to tell you what I really think. I’m still going to work with buyers and sellers, no matter if the market is up or down, so if I foresaw a catastrophic implosion, I’d be the first to tell you about it.”

I honestly did believe that 2013 could have been a year of little to no growth, and perhaps to stir the conversation, I suggested that it “could go up, or down.”

But the market went up 5.2% in 2013, and another 8.5% in 2014.

The reason? Same reason we see every year: inventory.

When it comes to single-family homes, there just isn’t enough inventory to satisfy the demand, and the market has gotten tighter in the past two years. I really thought at the end of 2012 that maybe the year ahead might show little growth, but then as we moved forward, every house seemed to have more offers than the year before, and the prices increased accordingly.

As we move into 2015, you still have bulls and bears, as you always will, and you still have pundits calling for a real estate implosion, while others are calling for another year of growth.

Re/Max, who published a 36-page “Housing Market Outlook Report,” which you can download HERE, suggests that the Toronto real estate market will add 4% in 2015.

Of course, Re/Max is a brokerage, so perhaps they’re biased.

What does the Bank of Canada think?

Apparently, the Canadian real estate market is over-valued by as much as 30%.

But we’ve been hearing that for a half-decade now.

And what I find funny about all the folks who say that real estate is “over-valued” is that they never seem to update their numbers. If somebody said, back in 2008, that real estate was “over-valued” by 10%, then how can they say the same thing in 2010 after prices have climbed another 10%? Wouldn’t that mean that prices are now 20% higher than they should be?

Going back to Garth Turner’s prognostications from when he started “The Greater Fool” blog in 2008, if he thought, at the time, that the market was over-valued by 20%, and the market has risen 51% since the closing price at the end of 2007, then does that mean he thinks the market is now over-valued by 70%?

I’d like to hear his thoughts put into sheer percentages, but alas, I can’t find any bold predictions on his blog, which believe it or not, I do read regularly.

I guess I just want one of these prognosticators, who started predicting “the crash” in 2008, to stand up and say, “Good GOD was I ever wrong, and I hope nobody listened to me, otherwise they’d have lost out on a sum of money which they’ll probably never have the opportunity to earn again.”

Is it naive to think that might actually happen?

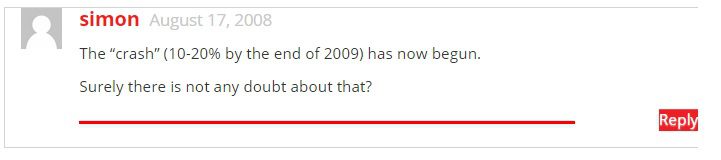

I remember a blog post I wrote back in 2008, where one of my regular readers at the time, posted this:

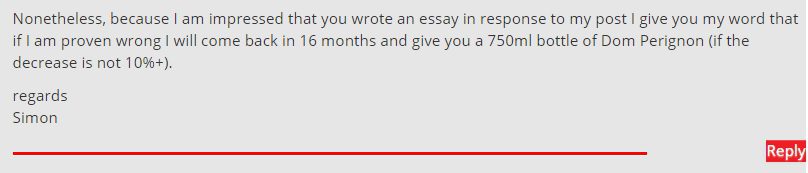

I posted a follow-up blog to this comment, and “Simon” wrote back:

And sixteen months later, a bottle of Dom Perignon was dropped off at my office by this mysterious blog reader, who I still have never met.

“Simon” had predicted a correction of 10-20%, and yet the market actually went UP about 13.6% in the 16-month period following August of 2008.

It’s nice to see people admit when they’re wrong, and I guess I just wonder how somebody can wake up every day, for eight years, call for the Toronto real estate market to collapse, and still sleep at night.

Does it work the same way in the stock market?

If you have the idea to short-sell oil in the Summer of 2014, and your broker tells you not to, because that’s “crazy,” and the world needs oil and it would never drop, then what does he say when you call him in January of 2015?

HERE is an article from two years ago, called “How Low Will House Prices Go?”

In the article, it mentions how David Madani, a well-known and often-quoted economist, was predicting for months that house prices were about to drop 25%.

And alas, prices went up 5.2% and 8.5% in Toronto in the two years since that prediction was made.

So what good are predictions?

They’re useless.

Especially when the predictors never follow-up.

I predicted that the Pittsburgh Steelers would “annihilate” the Baltimore Ravens on Saturday night, and yet my wife took Baltimore in our playoff pool, and while I was eliminated in week one, she went 4/4 in her picks and sits in a tie for 1st place among 76 entrants.

I can admit when I’m wrong, and believe me – I’ve said “I WAS WRONG” to my wife about a dozen times, as any good husband does.

In my year-end 2014 blog post, I did predict that Toronto house prices would rise a “modest” 4.5% in 2013, and some of the comments suggested that price was low.

At the risk of sounding hypocritical, having just said “predictions are useless,” I’d like to hear what my readers think.

Readers of this blog are both bullish and bearish, although probably more the former, and even if we can admit that predictions often can come out of nowhere, with nothing to back them up, I’d like to hear where people’s heads are at, nonetheless.

So put your two cents below, for what it’s worth.

And in Wednesday’s blog, we’ll talk more about trends and hot-button topics, in the 2015 real estate market, and how they might affect prices long-term.

myeo

at 7:33 am

Interest rates may cool things yet.

Appraiser

at 2:03 pm

@myeo: Interest rates, really?

The Canadian 5-year Bond (highly correlated to 5-year mortgage rate) is trading at 1.28 today, which is 2 basis points above the 52-week low and 69 bp’s below the 52-week high.

Fixed mortgage rates are going nowhere, except possibly down. While the variable rate may rise in the fall, it won’t be by very much. Do you actually think that 25-50 basis points higher on a variable mortgage by year’s-end is a game-changer?

Boris

at 2:30 pm

Look at Fed Fund Futures dummy.

Appraiser

at 7:06 pm

Your comment requires further explanation. For example, why would I consider using an American indicator of potential future interest rates in the first place, instead of Canadian Overnight Index Swaps? Given that neither the Fed Fund Futures nor Canadian OIS have been particularly accurate at predicting future interest rates, why should I use them at all?

daniel

at 12:01 pm

I’m not saying that Boris is right, but certainly some observers think that BoC will only raise rates on the heels of the Fed doing so. I think it’s very reasonable to say that US interest rates are an important consideration for the BoC.

More interestingly, i think the plummetting CAD could really kick inflation into gear (everything imported that’s priced in USD now costs 20% more for whomever is importing). If inflation takes off, and the AB oil sands economy doesn’t grind to a halt, the BoC could raise rates, which could set things off. Obviously this doesn’t jibe with the yield curve which suggests very low rates for the foreseeable future.

Overall, absent some external shock, i think we’re in for a repeat of 2014.

myeo

at 7:27 am

“may”

Johen

at 7:48 am

A balanced article… nice to see. I agree that market timing is impossible and that assets generally appreciate. In the stock market it is hard to argue with simple index investing with periodic re-balancing to avoid the problem of trying to time the market. But when assets appreciate so far so fast it is a concern. In particular, I’ve been wondering myself about supply as you mentioned. I am wondering if supply is low because the pipeline has seized up. Its hard to imagine that there are a lot of people able to move up from their small semi that they stretched for in the first place to a larger home in Toronto. If people are unable to move up then would it only be those that are forced to move for some reason or estate sales that would be supplying the supply? Prices would still be forced up for those willing to take the punt but on thin trading.

Appraiser

at 9:31 am

@Johen: another empty theory based on poor comprehension. Don’t confuse low inventory with low supply. There were over 88,000 MLS transactions in 2013 and over 93,000 transactions in 2014 on TREB. The supply is plentiful, but is being snapped up quickly. Low inventory in the GTA is a result of overwhelming demand, not because of people unwilling or unable to move up – because many thousands are doing exactly that every month.

Thanks for your amateur analysis though. You can slink back to Barf Turder’s advertorial blog now where amateur anaylsis abounds.

Johen

at 10:08 am

Disappointed to see that the reasonable tone of the article is not shared by its readers. Forgot I was on the internet for a second there.

Tina

at 3:01 pm

Why do you have to be so nasty?

John

at 7:52 pm

Please define inventory versus supply, not sure what you mean by this. Inventory is housing available for sale, supply is housing available for sale? what is the difference?

Appraiser

at 7:30 am

Supply is the number of new listings coming on to the market. Inventory is measured in the number of months it would take to deplete the existing listings on the market. The sales to new listings ratio is perhaps a better measure of the market in that regard. Also average days on market (DOM) is a good indicator of how quickly the market is moving. Bottom line is you can’t have 93,000 transactions without at least 93,000 listings (supply). Although the official numbers aren’t out yet, that’s near record territory for TREB.

John

at 8:47 pm

Got it, the DOM as an indicator helped wrap my head around it, thanks for the detailed explanation.

ScottyP

at 10:51 am

Ladies and Gentlemen, before your very eyes you’ll find the Bad Appraiser (presumptuous, prone to ad hominem attacks, outright nasty as Tina aptly put it above) and the Good Appraiser (knowledgable, helpful in his/her explanations, a valuer of proper evidence)… all in one convenient mini-thread!

donny

at 7:57 am

There is an immigration explosion in this city and I believe the day will come when the population hits 8-10mm people….I wonder what home prices will be then?

Boris

at 9:11 am

One new issue is the negative wealth effect created by capital markets. Most people that buy a $1mm + house sell other investments to do this. Portfolios, bond and stock, have performed dramatically well since 2009. In the past 3 months we have experienced the opposite in Canada – A dramatic negative wealth effect exacerbated by the oil selloff. Bank stocks, insurecos et all have not been immune. At the margin the US economy is outperforming Canada, Fed Fund futures are pricing a US rate hike schedule sooner than it did 3 months ago.

I could see the $1mm+ market giving back 5% this year, easily. The amount of leverage in the system is terrifying, but that’s not my thesis.

Appraiser

at 9:43 am

@Boris. What evidence do you have that “most people” that buy $1M+ homes sell other investments to do so?

Do you have any empirical data to back that up, or is it just another empty theory that you pulled out of your arse?

Appraiser

at 11:27 am

@Boris: Anecdotal evidence does not count, no matter how much of it you CLAIM to have.

As you can see, I don’t suffer fools gladly; and you are a fool.

Boris

at 11:32 am

Hey appraiser, it does count.

Use your brain. Of course most people that upgrade from a $900k house to a $2mm house sell securities. Common sense, and yes it counts because i SAID SO!!

Mike

at 11:22 pm

I’m not sure you can call programs created by the government that allow people to use other investments to fund home purchases “anecdotal” (RSP home loan et al).

Kyle

at 9:33 am

Ben Myers did some analysis of Toronto home prices over the last 286 months (24 years) of Toronto house price data. In a “normal” market there is a 51% chance of a 0-6% annual gain. However, i don’t believe the current supply/demand situation, where there are 3+ buyers for every seller could be called “normal”.

I think average Toronto home prices will rise 7-12%, because:

1. Supply will get even tighter – people who have bought will opt to stay put longer due to the high transaction costs, and not wanting to become a buyer again in a sellers’ market. Combine this with fewer new condo completions in 2015 and far fewer TCHC properties being disposed of means fewer homes available for sale.

2. Demand to live in the core will continue to increase – Toronto will continue it’s urbanization trend as people shun the long commutes and the lack of walkability. Price per sq ft in the core will outperform prices in the suburbs and even out perform many of the established cachet neighbourhoods of the inner burbs.

3. Developers will finally start to build more two and even three bedroom options for families that are priced out of SFHs. So the mix of properties that make up the average condo price will no longer be as skewed towards 1 bdrms and bachelors.

4. Interest rates will remain low for at least the first 3 quarters of 2015, and lower $CAD and lower oil prices mean lower inflation and lower prices on other goods. Combine this with tax cuts from the Federal level and affordability will improve.

Ben Myers

at 11:04 am

Hey Kyle,

Just to be clear, my figures were for new homes only:

http://fortressrealdevelopments.com/news/what-canadian-housing-bears-dont-want-you-to-know-part-2/

But thanks for reading.

Kyle

at 11:10 am

Thanks for the clarification and the informative writing.

Ben Myers

at 2:43 pm

No problem. Please share your thoughts on the 2015 housing market by taking this Buzz Buzz poll: http://news.buzzbuzzhome.com/2015/01/big-data-with-big-ben-smarter-than-housing-analyst.html

Martian

at 12:50 pm

This all sounds exactly right to me – sadly.

Point 1: Some relatives own a VERY large home in a very desirable neighborhood, although it’s not in great shape. They are getting older and looking to sell and downsize. The only thing they want is an affordable 3+ bedroom with a yard, walkability, ample space for hobbies, a master bathroom, a potential basement rental apartment, access to parks, transit nearby… you get it right? What they want is going to cost 90+% of what they have, and so they aren’t going to sell.

Point 2 – although I really don’t want to live there myself… I totally agree. Traffic is horrible and getting worse. Even living 4-5 km from downtown as I do means a 40 minute commute each way. This makes downtown more attractive, especially as more and more commercial office space is built and so even MORE jobs are right in the core.

Point 3 – well, they say they’ll build them. I hope it’s true because it’s really the only hope at this point for first time buyers with families. I live in a neighborhood where that trend SHOULD be happening – lots of young parents, zoning that only allows low- and mid-rise buildings – but I’m not seeing it.

Point 4 too true. Interest rates are rising… oh this time it’s going to happen. It never happens. I really wish it would, for many reasons. But it can’t too many people would get crushed.

Don’t forget the last factor… The dollar dropped 20%. Hey that makes Toronto even more attractive to people buying in rubles/yuan/yen/euros/US dollars/rials/whatever.

Boris

at 1:29 pm

Martian, good points.

Be careful on the FX thing – the CAD has mainly declined vs the USD. The CAD has actually strengthened against the EUR, JPY, Ruble, in the last year/quarterm although weakened against the Renminbi.

Martian

at 2:25 pm

I take your point. I just mean that it makes Canada even more attractive relative to the US if you’re looking to ship a lot of money out of [insert unstable repressive country] and into a nice safe investment.

Kyle

at 1:36 pm

Good point, the low $CAD makes Toronto homes cheaper for foreigners, but even worse than that makes hover boards more expensive to Canadians.

http://www.dailymail.co.uk/sciencetech/article-2657090/Great-scott-1-500-hoverboard-flies-air-using-high-powered-jet-water.html

Kyle

at 10:59 am

@ Martian

Regarding Point 3 – With such a large price gap between 2 bedroom condos and small starter homes in the city, the economics of building larger units is really starting to make more sense.

http://www.thestar.com/business/2014/12/28/the_return_of_the_larger_condo.html

Huuk

at 2:22 pm

Great points Kyle.

You seem to actively state that prices will continue to increase in the GTA.

I am curious, do you believe that if interest rates increase in Q4 (point 4), house prices will decrease immediately? Like, will a (artificially large for hypothesis purposes) 50 basis point increase in rates have a corresponding effect on prices?

Kyle

at 2:55 pm

If interest rates rise gradually and methodically i can see the rate of price appreciation maybe slowing to medium to low single digits, but i don’t think prices will go negative without an economic shock. IMO the last thing the BoC wants, is to be even remotely associated with being that shock, so i see them raising rates as slowly as they can get away with, without inflation rising above 3%. Also the falling oil prices will give the BoC breathing room on the inflation front.

In terms of buyers’ sensitivity to a one time 50 bp rate hike, i don’t think that’s going to be enough to push prices into the negative. IMO, i don’t think that will even register to most Toronto buyers. On a $450K mortgage, a 50 bps increase translates to about $120/month increase in mortgage payment. To put this in perspective, a family with two children will receive an extra $120 per month in Universal Child Care benefit from the Federal Government in 2015. So a 50 bp interest rate hike is just as unlikely to tank the housing market, as a $120 increase in Child Care benefit is to set the market on fire. My guess is, rising interest rates will not push prices into the negative unless they are hiked in a prolonged aggressive manner, like 2-3% in under two years.

Martian

at 3:21 pm

Interesting point. But don’t you think interest rates are more about perception than reality? I mean sure, <1% increases aren't super significant day-to-day, but it will feed the story – that's it, the market has turned, the boom is over, etc.

As I said I actually hope rates rise for a number of reasons. But I'd bet for a rate CUT before I'd bet on a hike. Look what's happening with the housing market in Calgary… a key vote-rich conservative base area… couldn't they use a little help right now to make things better before the election?

The US housing market got way too hot, the fed raised rates (yes they used to do that) and that crashed thing. I assume the thinking in Ottawa is simply: well if we never raise rates, we will never crash things. So far so good!

Kyle

at 3:36 pm

From what i’ve noticed over the years, i think buyers and sellers react differently to interest rate changes. I find sellers tend to be far more easily spooked than buyers. When rates rise, i’ve noticed that sellers tend to respond more to the perception than reality by taking/keeping their homes off the market, for fear of being caught out, while buyers who are more attuned to their affordability and to regularly crunching and re-crunching their payments, seem to be less affected by the perceptions.

Kyle

at 5:08 pm

I don’t think i articulated the above that well so i’m going to try again, because i think it shows the quirkiness and irony of human nature. I find sellers and buyers worry about different things and respond to those fears differently. Strangely though, their differing responses tend to lead to higher house prices.

An active seller worries about sale price, and if he thinks his sales price will fall, he only has two options: 1. sell for less than he’d really like to 2. don’t sell and ride it out. Unless circumstances force them, most sellers tend to choose the latter. In 2008-2009 after the crisis, a whole bunch of sellers tried to get out in the months immediately after the crisis, but the rest of the sellers said screw this i’m riding it out. Months of Inventory (MOI) had a large short term spike during Winter 2008-2009, then MOI completely evaporated by the summer to record low levels.

An active buyer on the other hand worries more about monthly affordability than sales prices, and if he thinks his affordability may erode he has three options: 1. don’t buy 2. buy now to get ahead of the changes 3. readjust expectations based on revised affordability. Most active buyers tend to choose 2 or 3, very few actually end up giving up.

The irony is unless things get really bad (i.e. a true economic shock where a lot of people MUST sell and a lot of buyers CAN’T buy), house prices tend to actually rise in times when things start to look less rosy.

rob fjord

at 2:35 pm

india just lowered their interest rate, but its still much higher then canada and US. where do you want to put your money, in old N america where senior citizens living in their cars are getting their 3rd part time job at walmart…or in young dynamic india, pouring 20 billion a year into solar projects, a new pro business government and the hindu religion advocates the buying of gold (real money)…and they their bonds pay a much higher return then N american bonds.–we will be competing with them for debt issues…we will lose!–rates must rise and rise substantially. the reckoning is coming to glib n.americans.

Kyle

at 3:24 pm

I’ve been all over India. Living in a car would be like winning the lottery for a huge portion of their population. There’s a reason their interest rates are higher than ours, and there’s also a reason soveregin debt is rated BBB- and we’re rated AAA.

Paully

at 9:48 am

I have heard it said that rising markets climb a “wall of worry,” so if/when all the bears finally capitulate and decide that the real estate bull will never be slain, then I guess that would be the correct time to exit. If nobody thought that real estate was looking overvalued, then I would be really worried.

Here in Willowdale you have a continuing “supply” problem because every more-affordable older house gets immediately snapped up by the speculators and taken out of the market while it is torn down and rebuilt into a McMansion. This makes the property uninhabitable and unavailable for something like two years, maybe more. On my block alone, there are at least four properties empty and in some stage of redevelopment. Block after block around here are muddied by lots of rebuilding activity. Closer to Yonge St. the zoning typically allows for the lots to be severed, so the net supply will ultimately go up marginally, but further away from Yonge, they don’t generally allow severing, so rebuilding only chokes supply in the short term. Until the speculators get squeezed out, their ongoing activity ensures a continuing tight supply and supports more price increases and more speculator activity in a classic virtuous circle.

Ed

at 1:28 pm

Here is my two cents (with rounding = 0 cents).

I think the Toronto market will see another hot year in 2015, here is why.

1-cheap oil= more disposable income for consumers and also good for manufacturing in Southern Ontario.

2-depressed Canadian dollar= good for export manufacturing in Southern Ontario. More jobs.

3-USA growth is starting to escalate= good for exporters as about 70% of all exports go to USA

4-USA growing economy may lead to prime rate hikes in USA and the msm will put the scare into consumers that rates will rise here also, this is turn will get those who’ve been sitting on the fence into the market to beat the rate hike.

So here is hoping for another banner year with regards to price appreciation because I am this close to selling and getting the hell out of Dodge.

Boris

at 1:50 pm

Ed – on a net basis the decline in energy prices will be net negative for Canadians. The MSM overhypes the consumer benefit of lower gasoline prices.

Let’s say the average person that drives drives 2k km per month. That’s 24k km a year. This is in line with CAA’s estimates for ‘average’ whatever that is. Let’s make it simple and estimate mileage at 10 L/100km. That is 2,400 litres per year. According to NRCAN, the national average for gasoline was 127.9 in 2013. Assume now most are paying 90 cents. That’s a savings of 37 cents per litre over 2,400 litres, assuming all else constant. This results in savings per person of $888 per year. Not exactly enough to get people into new bidding wars on $1mm properties.

Secondly a lot of people, especially in the GTA don’t drive, or drive but commute to work on transit.

Most importantly, the real losses in teh economy due to energy;s decline is multiple times that of any savings on gas. CIBC estimates that gross national income will decline $34 billion as a result.

http://research.cibcwm.com/economic_public/download/feature1.pdf

Chart 7 tells the story, but chart 5 indicates they expect a -ve GDP shock to Ontario as a result of lower energy prices.

Ed

at 2:14 pm

Boris, the decline in energy prices may well be a net negative for All of Canada as a whole but it will be a net positive for Ontarions (sp?). But then again who knows how long oil prices will stay this low.

Boris

at 2:34 pm

I’d say maybe a small net positive for Ontario. But remember capital is mobile and does flow from province to province to purchase assets. Also, asset prices are discounting mechanisms, At the margin there is -ve change w regard to capital & personal liquidity for the average CDN. Plus people’s portfolios have been trashed.

Martian

at 3:29 pm

This is such a great point, I was thrilled about lower gas prices. I filled up on the weekend and compared to my usual tank I saved… $18. Wow I’m really rolling in the dough now!

The story of it benefiting southern Ontario, I’m not so sure. A lot of manufacturing is gone and it doesn’t just turn on a dime and come back from Mexico/Michigan/Southern US. Ask anyone who lives around London whether Ford or Caterpillar is going to move back.

Ed

at 1:31 pm

Oh yeah.

The biggest reason we will see another great year for Toronto real estate.

Because Garth says we won’t.

ScottyP

at 10:55 am

Ah yes, the DOG Theory. (Do the Opposite of Garth.) I’m a big fan myself.

Marina

at 1:45 pm

Hard to say what will happen in 5 years, but for 2015 it’s pretty obvious.

Any halfway decent SFH in Toronto sells – fast and over asking. There is a backlog of people looking to buy. Of course prices will go up this year. After that, who knows.

But if prices fall in 2015 it would have to be because of something so economically damaging that real estate will be the least of our worries. That’s my 2 cents anyway.

On the wish front, I do wish prices would soften a bit – I’d love to move up to a bigger house, but can’t afford it in my area. Thank God we bought when we did or living in Toronto would be a pipe dream.

Paully

at 3:25 pm

I think that the only safe prediction for 2015 is that a certain individual will continue to be rude and insulting to other commenters rather than simply trying to make an intelligent argument when posting.

My wish is that our esteemed host will choose to edit/delete/ban that individual if he/she/it continues to be so consistently rude to the rest of the generally pleasant and intelligent readers and commenters that visit this blog.

David Fleming

at 3:37 pm

@ Paully

I already deleted/edited three comments from today. The problem is that they’re from three regular readers/commenters, who 9/10 times, have something very informative to say.

These guys know who they are.

All I can ask is that they stop name-calling and swearing, because I’m going to delete those posts.

Somebody said earlier “This is the Internet,” which is true, and it’s always been a place where chaos reigns supreme. On this blog, I’ve been blessed that the readership is educated, savvy, intelligent, and most of all – informed. But sometimes in an argument, people revert to being five years old. I can’t control that.

I will make a better effort to edit/delete/ban in 2015, even if it means fewer comments, or less intelligent insight that contains insults.

When I launch THE FORUM later this month, it’ll be constantly monitored, and I’ll have a giant red button on my desk that simply shuts it down forever. As Kyle said in my year-end blog, “Be VERY careful!” It’s true. The forum can be an incredible source of insight and an amazing collection of individuals, or it can be a kindergarten class. We shall see…

Kyle

at 3:42 pm

Actually it was Joe Q, who advised to “Be Very Careful”, but i agree with him.

David Fleming

at 6:00 pm

@ Kyle

Dammit, I can’t tell you guys apart!

Kyle

at 8:17 pm

Here’s where i have to steal one of Chroscklh’s excellent lines: We both have the smouldering good looks, but i be the taller

ScottyP

at 10:56 am

Kyle is the feisty one.

A Grant

at 8:08 pm

I think the reason some many were willing to take the prognostications of the bears to heart is from year to year, we saw home prices in the core rising at rates significantly higher than inflation. Or, more to the point, at a rate significantly higher than the average household income (which has been stagnant in terms of real buying power since the ’70s)

Predictions aside, if the market does undergo some sort of correction, it’s those of us living in single family homes in core urban neighbourhoods that will be impacted the least. I worry more about those in suburban track housing, only accessible by car.

Unless there is a significant global financial collapse, of course.

hoob

at 12:08 am

What I want to know, is will the maker of multicoloured year date blocks figure out that there’s no need to put “1” on multiple sides of the yellow or any block, and only the finaly digit block needs to change.

Potato

at 1:29 am

You need to plug things in to the models to make predictions. In 2008 prices in Toronto were about 30% over-valued, and interest rates were about 6%. The market started to roll over… then interest rates plummeted.

Then we had a long couple of years where the BoC kept indicating rates would go back up in the near term (next few years) but it kept not happening. So if you assumed rates would go back up, the over-valuation was still there, but was nowhere near as bad if you assumed low rates were here to stay (who knew!).

Well, rates have stayed low for 5 years and the economy’s back to looking ill, so we can really lower our long-term rate expectations… except now there’s been so much appreciation on the back of that stimulus that we’re back up to ~30% over-valuation even with those updated, rock-bottom expectations on rates. If you think rates are going to normalize around 6% then it’s more like ~45% over-valued now.

You only get to lock in your cost of housing once, and you can rent as long as you like. So even forecasts that are wrong post hoc (short-term) can still lead to the right a priori choice. And of course many of the people who called the US meltdown did so years in advance of the actual peak — laughing at them four years after they first identified the problem would have been the height of folly. So, do you put a time limit on a forecast/warning? 7 years or it’s out, no matter the GFCs throwing monkey wrenches in the meantime (should I turn in my bear card now that it’s 7?)? Do you base it on fundamentals? As long as rents and incomes are stagnant while prices are on a tear the thesis only gets stronger — and significant rent inflation is the point of capitulation rather than a time limit?

Will 2015 be the year that it crashes or at least starts to turn? I don’t know; possibly, given what the BoC has said, and the increasing visibility of bearish stories in the media. I’ve got some hope that 2015 looks better than 2014 did (though 2013 looked even riper than 2014 and nothing came of that). Maybe people will listen. But it’s never a stock-like flash crash, if and when it does correct it will take years and years to play out.

Appraiser

at 7:48 am

@Potato: Clearly you are a dyed-in-the-wool real estate bear, so there is little use in attempting to alter your perspective.

However, allow me to make my bold prediction. We will have a real estate correction when we have a recession, and not before.

Just like every other time.

Kyle

at 9:03 am

@ Potato

This will likely sound harsh, even though i don’t mean it personally. The reality is this – bears may be many things, but they are not active buyers. So regardless of whether they choose to keep the faith or accept reality, their capitulation will have zero impact on house prices. It is no different than when i finally capitulated, and accepted that i will never be able to afford a new Ferrari. And to no ones’ surprise new Ferrari prices did not come crashing down.

rob fjord

at 2:44 pm

“years and years to play out” not with wide spread isis attacks in the west..YES, im predicting that! so you can all nominate me as the most extreme nut job here. i gladly accept. islamic terror and russian/chinese terror will be the biggest movers of all markets going forward

Jonathan

at 12:15 pm

Even if house buyers are not selling securities to fund their move-up house purchases, there is definitely a correlation between high-end house prices and the stock market. Many people buying those homes are working professionals in finance, law and other fields that are linked to financial markets, both in terms of overall compensation (bonuses) and job security. When markets drop, people worry they will get fired or bonuses will drop to the point where they can’t afford to buy (and carry the costs of) a trophy house.

I’m not one for making bold predictions due to the inherent uncertainty of the relevant inputs, but it does seem pretty clear that the average SFH price in Toronto will increase (or remain flat at worst) unless unless one of these things happen:

– interest rates increase by a material amount (say 100bps)

– another significant stock market correction (say >20%) that isn’t followed by a quick rebound

– drastic CMHC policy changes (such as mandating a minimum 20% downpayment for all purchases)

In the absence of any of these external shocks, I can’t see any other reason why prices would fall. What else is there, really?

ScottyP

at 10:40 am

“So what good are predictions?

They’re useless.”

^^ THIS.

Tyler

at 6:16 pm

Garth goes on in his latest blog post about the house that he says he rents in Toronto. Think you you got his attention! I assume whether he owns or not is easily proven through public or mls records though?

Kyle

at 9:21 am

Haha, i read that post and laughed my ass off. He says of his $2M rented home, “So, I rent, although I’m fortunate enough to be able to buy this house with cash”. What a clown! Everyday, he pretends to be looking out for the average middle class guy, and now rubs salt in their wounds “by basically telling them i’m filthy rich by screwing you”. The people who follow him are in no position to live in that neighbourhood, regardless of whether they rent or buy, because they didn’t make millions doing the following unscrupulous things:

– Own a TV Production company called Millenium Media, where he produced a show called Real Estate Television, which was a big RE pumping machine that generated revenue from developers. Funny how he doesn’t mention any of this on his blog

– Write and sell fictional books about the crash that never came, and try to pawn them off as non-fiction

– Collect payola from mutual fund companies and financial advisors, for doing television advertorials

– Make a bunch of tax free equity off of the house he bought, at the same time he was advising everyone else to get out of real estate

– Become a Financial Advisor, who has gained lots of notoriety for telling people to underweight real estate and over weight their Investments.

– I could go on, but lets face it many of his followers aren’t really interested in facts

David Fleming

at 5:06 pm

@ Tyler & Kyle

Garth sold his house this past year at a loss.

It would have made serious headlines, but apparently there were health concerns, and so the media (myself included) decided to leave it alone.

Wut

at 1:09 am

Doesn’t the media have a responsibility to report that? He’s making his living telling people to sell their homes and invest with an advisor which he happens to be. Meanwhile he is buying and selling properties the whole time since 2008. And apparently used a realtor (whose boards he regularly slams as dishonest) as his sales history must be in MLS for you to know that.

If Garth truly felt the market was a bubble in 2008 how can he buy? Would you trust a financial advisor who does the opposite of what he advises you? What would you call that?

Wut

at 12:59 am

I’ve posted on his blog a few times (both agreeing and disagreeing with some of his points, I’m not a bear or bull), and challenged him on his claim that his rental has not appreciated at all in 2 years. Creb says his area appreciated over 8% for sfd year over year from December. He would not post it to his blog.

If he did earn 10% on his portfolio, which is good, once you take out taxes and rent he didn’t do as well as the house he’s renting. Ironic.

Wut

at 1:15 am

As for GT admitting his predictions were wrong on his blog, if he did that he’d have no time to make new predictions. He’s already backed off his guarantee that the TFSA was going to 10k contribution room this year. That only took a couple weeks. Now his guarantee of rate hikes this year are looking bad. He’s like the George Costanza of financial advisors. Whatever he says, do the opposite.

rob fjord

at 2:21 pm

from 2000-2007 i predicted the tor real estate move wrong, 8 years wrong! 2008 i was right, 2009 i was wrong, 2010-2014 i was right. 2015 is the first time im not definitive with my prediction, but i say this, first half up, 2nd half down, overall i lead to a negative year overall, with a possible implosion in the fall if terrorism finds the streets of US and canada, which i believe is only a matter of time, a when not an if. last year i predicted Us would raise rates this year 2015, i stand by that and think it will come sooner than most believe, could be a surprise rate hike next week…many central banks have been surprising us lately.

Former Leaside Realtor

at 2:11 pm

Posting late on this, but I’m surprised there are no new comments since the BoC rate cut. Add Joe Oliver’s comments that the Feds aren’t concerned about house prices now and its a new mix.

Love your introduction David. I was a GT blog reader while I was home shopping in 2009. When I posted to his blog in Nov/09 that I had just bought, he asked “Are the idiot who bought the 30′ property last night in Leaside for $1M ?”. I wasn’t. Partly because of Garth’s cautions we took a safe route and bought a duplex, now triplex, for just under $1M. Current status – up nearly $500k plus mortgage balance down $85k. Even with 5% down our monthly costs were lower than rent. So, tastes great and less filling too.

For predictions, because of the volume demand in Toronto I don’t see a down trend until rates rise by 1% or more. And that now looks further away now than before – at least a year.