Do you know I’ve written 2,184 blog posts?

Actually, this one makes it 2,185…

I thought it was more than that to be honest, but then I recalled a special feature I did for my “1500th Blog Post” a few years back, and suddenly 2,185 seems in line.

I’m religious about Toronto Realty Blog. I truly am.

From time to time, I check in with a person who I wouldn’t call a psychologist, but also wouldn’t call a therapist, but I’m not sure fits the mold of a business coach, or even a life coach. While the definition of this person’s occupation eludes me, it doesn’t make him any less important in the context of listening, advising, and helping me keep my head on straight.

I’ve identified that I have a lot of “rules” in my life, and while these rules seem outrageous to some, and unnecessary to others, I can’t help but feel that they keep me grounded, and on the correct path.

I don’t drink during the week. I just don’t, I’m not sure why. I don’t have a pint at lunch like so many people I know. I don’t drink a bottle of red with dinner. I have been known to get shmammered alone on Saturday night and spend too much money bidding on hockey cards on eBay, so it’s not as thought I’m a non-alcoholic saint, but rather I just have this rule that I abide by.

I don’t get home before 5pm. Ever. It feels unnatural to me, and even though the whole world does it, I refuse. And the fact that I’m self-employed, and I work weekends, as well as many nights until midnight, doesn’t “even out” the hours worked, and allow me to go home early. I just can’t do it.

And a rule that I have abided by for fifteen years: I blog on Monday, Wednesday, and Friday, with a video on Thursday.

When it was suggested to me that, “Maybe you don’t need to blog on Monday, Wednesday, and Friday,” I laughed. I actually LOL’d as the saying goes, since the suggestion was comical in nature. It was like a colleague asking on Tuesday at 11:30am, “Hey, we’re going for five-dollar martini’s for lunch at the such-and-such pub, wanna join?” Have we met? Yes, so, ummm….

Call me boring, call me rigid, call me inflexible and stuck in my ways. But I have these rules in life that are certainly born of obsessive-compulsive disorder as well as a need for routine, order, and control (if time permitted, I could detail another dozen rules, but I think you see that the first two were intended to introduce the third), and my rules keep me focused. The routine keeps me normalized.

I hate not writing a blog on a Monday. It pains me to look at my mailed-in, cop-out post about going down to Cambridge, but once in a while it’s a necessity. I used to muse, “Toronto Realty Blog doesn’t take sick days,” but man, is life ever busy.

Those of you with four kids – how do you do it?

I have one, and one more on the way in February, and at times, I feel like I’m upside-down.

My Dad told me his theory on kids: “One is great, and two is amazing, but three is like seven.”

Spoken like a man who had three kids, I suppose.

The days seem so much shorter this time of year too. There are still twenty-four hours in each day; that hasn’t changed. But when it starts getting darker at 4:30pm, it’s like the walls are closing in.

In the world of real estate, things have slowed down, but not as much as they used to.

When I first met my wife in 2010, and when we were living together thereafter from 2011 onwards, we had this way of referring to my occupation at this time of year: “DECEMBER in real estate!” That doesn’t sound very descriptive, but I mean that when things slowed down, and I only had a few hours of work to do each day, with a couple of days to escape for Christmas shopping, followed by two weeks at the end of the month without the phone ringing, it was “DECEMBER in real estate, baby!”

Circa 2013, I used to roll into the office around 10:30am, nurse a large Tim Horton’s coffee, write out a dozen Christmas cards to clients, and ease into the afternoon.

Maybe it’s a function of my business expanding, and maybe it’s the market becoming more complex, but things have really changed in recent years, and I honestly do think that the reason December is so much busier than in years past is because of how frenetic the Toronto market has become. The stakes have never been higher, inventory has seemingly never been lower, prices are rising while demand increases and supply falls, and decisions have to be made much faster. Buyers need to hit the ground running, and that is why so many of us agents are slammed in December: the 2020 buyers are already getting their feet wet.

So let’s see: wife, kids, baby on the way, yet another cold, shorter days, busier December, flying to Cambridge for a course when I thought things would be slow – all reasons why, try as I might, I did miss my self-mandated blog post on Monday.

It’s true, I suffer from Catholic guilt. But I’m not Catholic, so explain that to me…

Before I left for Boston last week, I did get a chance to run over the November TREB numbers and I was surprised by a few things. In fact, “surprise” has been the theme of these now-monthly blog posts on Toronto real estate statistics.

I always say that stats-geeks, whether bears or bulls, have a particular stat they want to look at first, be it sales, or inventory, or a particular ratio like SNLR, or price.

This month, I was primarily interested in price.

I’m not a price-junkie, in fact, I usually care more about inventory or SNLR because it sheds more light on why prices are doing what they’re doing, or even where prices are going. But this month, I was curious to know how prices would drop from October.

And would you look at that: I’m already making a prediction.

I mean, prices must drop from October to November, right?

That’s the pattern, or at least it should be. Prices jump up from August to September, as the slow summer leads to the busy fall market. Then demand continues through October when prices continue to rise, but sales are sluggish in November, usually due to lower inventory, so prices drop ever-so-moderately, if at all.

That’s my view of the fall market.

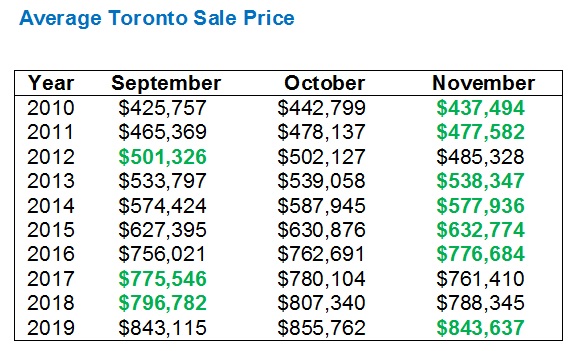

And with the October average home price in Toronto sitting at $852,142, I wondered where this figure would end up in November.

In 2019, we saw the October average home price drop 2.5% to November, from $807,538 to $787,349.

So a similar 2.5% drop in 2019 would result in the average home price dropping from $852,142, which is the highest it’s been since May of 2017, down to $830,838.

An average sale price of $830,838, for what it’s worth, would end up lower than the $843,115 price in September.

In the end, the average Toronto sale price in the month of November came in at $843,637, which is only a 1.0% drop.

This got me wondering about three things:

1) What is the average drop in price from October to November?

2) Have there been months when price does not drop from October to November?

3) How often is November’s price higher than September?

So first, let’s take a look at the average sale prices in October and November for the last decade:

I’ll be honest, I was surprised to see that in two years, 2015 and 2016, the average sale price actually increased from October to November. But then when I thought back to the fall of 2016, which was so insane that it was, looking back on it, one of the major root causes of the crazy spring-2017 market, I’m actually not surprised to see the increased price. As for 2015, call that an outlier, and it’s a rounding error at 0.3% anyways.

Through the ten years, the average change from October to November is -1.1%.

The average drop, for the eight years in which we saw a drop, is -1.6%.

So with the first two questions answered, I wanted to move on to the third.

If I had to guess, I would think that in a ten-year sample, we’d see a fairly even split between years when the November price dips below September, and years where it rises above.

Here’s what I found:

Well, colour me green!

Seven times in ten years has the November sale price risen from September, to October, to November.

In fact, I might have been experiencing a recency-bias, since before 2018 and 2017, in 6 of 7 years, the November price was higher than September. But it just sort of looks that way in my mind’s eye.

So does that mean that sales are higher in November as well?

No, it doesn’t.

Not even close…

Would it surprise you to know that sales, while increasing 10/10 years from September to October, as expected, are actually higher in 8/10 years in September than November?

So price is higher in 7/10 years in November.

But sales are only higher in 2/10 years in November.

What gives?

Well, I suppose we should look at inventory then?

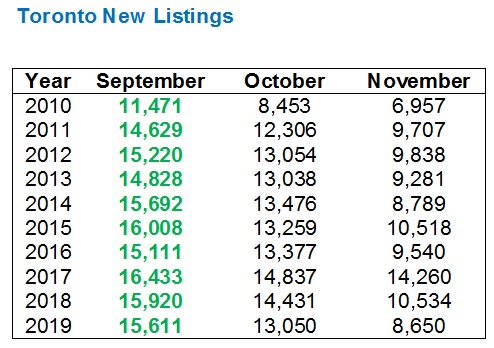

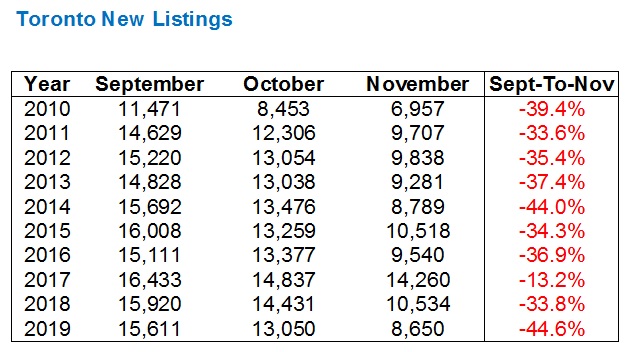

Well, if this isn’t a trend, then I don’t know what is.

Not only do we see new listings trail off from September to October in 10/10 years, but as per the examination between September and November goes, we see 10/10 years here too.

Let’s review:

- Sales increase from September to October in 10/10 years.

- New listings declines from September to October in 10/10 years

- Price increases from September to October in 10/10 years

That logic follows perfectly.

But what then of September vs. November?

- Sales are higher in November than September in 8/10 years.

- Prices are higher in November than September in 7/10 years.

- New listings are higher in November than September in 0/10 years

Again, this logic follows perfectly.

Sometimes, you just feel like pointing out the obvious.

And for anybody out there that still doesn’t believe that supply is lagging well behind demand in the city of Toronto, I challenge you to argue with the above.

Now one final thought on inventory, and this is just mind-blowing to me.

How much lower is inventory in November than in September?

Those numbers are staggering.

For those of you who were buyers in this fall market, I’m guessing you did much better in September than you would have in November.

Not only did you have more choice, but there was less competition, and prices were lower, at least, on average.

The drop in inventory from September to November averages 35.3%, and just look at what happened this fall: inventory dropped 44.6% in two months. And December? Forget about it. December in real estate is a barren wasteland, at least, after this week that is.

Well, that’s it for me, folks.

Good to be back. I prefer snow to rain anyways…

Island Home Owner

at 8:44 am

Our second son arrived in June 2018. As expected, our family has committed to preserving the option of playing man defense, so we are keeping it at a family of 4. VERY pleased with this choice, no matter how cute those other two are …

GinaTO

at 9:44 am

We would have loved to have a third kid, but it didn’t work out that way. Life got sooooo much busier going from one kid to two, though.

Kyle

at 10:34 am

Something i find surprising is that when you look at the historic annual Sales Prices for the months of September, October. You don’t even see the recent market peak, pull back and recovery. In November the pull back barely even registers. It really goes to show just how short and isolated that irregular activity was.

Appraiser

at 10:48 am

Excellent number-crunching once again David. Great insights.

I have to agree that supply is the major issue affecting the GTA housing crisis.

An inadequate level of new housing construction along with a chronic dearth of listing inventory is focusing persistent upward pressure on sale prices. As a direct corollary, rents are also surging.

The need to reverse this trend is immediate. The GTA requires increased supply in all sectors of the housing market including, affordable housing, purpose-built rental apartments, condominiums and low-rise construction.

Please, let’s top wasting time debating the mythical virtues of banning foreign buyers, taxing vacant properties or perhaps trebling the land transfer tax. Such measures are in the end unnecessarily punitive in nature, often cumbersome to administer and perhaps most importantly, ineffective.

Build Baby Build!

Chris

at 11:05 am

“Why You Can’t Afford a Condo in Toronto – One data trend emerges starkly amongst a litany of theories.

Today in Toronto, condos are primarily a way for investors to profit from rising condo prices and rents – pushing average buyers out of the market.

The other risk when investors begin to have an outsized impact is that it makes the housing market more vulnerable to future price declines. We saw this in the US during the financial crisis of 2008, the cities that saw the biggest decline in house prices were largely dominated by investors.

More recently, we saw the effects that a high level of investor demand can have on house prices in the Greater Toronto Area (GTA) – research that I published in early 2017 showed that investors made up a sizeable share of the people buying homes, in particular in York Region. They helped push house prices (mainly for detached homes) higher than they otherwise would have been and when house prices crashed, the Bank of Canada used my investor research to show that the regions in the GTA that had the highest share of investors saw the biggest decline in prices.”

– John Pasalis, Realosophy, Dec. 11, 2019

https://www.movesmartly.com/articles/why-you-cant-afford-a-condo-in-toronto

Appraiser

at 1:37 pm

My research also indicates that the primary reason the stock market is so high is those damn investors.

Chris

at 1:46 pm

“One of the biggest myths pushed by the real estate industry is that without investors, the supply of new condos would plummet. Even @CMHC_ca has pushed this misguided narrative which puts investors ahead of home buyers.

This of course is just a myth. Every pre-construction condo I sold 10 years ago was to an end user. The fact that the vast majority today are bought by investors is because builders and misguided policy makers put the interests of investors ahead of home buyers.

Prioritizing investors crowds out home buyers because investors have been found to bid more aggressively for housing than end users. Not only are home buyers crowded out, our condo market is more vulnerable than it was 10 years ago because its dominated by investors.”

– John Pasalis, Dec. 11, 2019

Appraiser

at 1:51 pm

You need to read more broadly. Perhaps in hopes of attaining deeper insight.

Pasalis only thinks he’s a genius.

Kyle

at 1:57 pm

Appraiser is bang on here. John Pasalis fails to understand, it doesn’t matter whether the owner is an investor who rents it out to someone else to live in or an end user who lives in it him/herself. The actual single and only reason condos are so expensive is because there are more people who want to live in them than there are units available for sale. Full stop.

Chris

at 2:03 pm

“A specialist in real estate data analysis, John’s research focuses on unlocking micro trends in the Greater Toronto Area real estate market. His research has been shared with the IMF and cited by the Bank of Canada and CMHC.

A frequent commentator on the Toronto housing market and real estate consumer and industry issues, John has contributed to the Globe and Mail, CBC, BNN Bloomberg, TVO’s The Agenda, Toronto Star and other media, government and industry organizations. He most recently advised the Government of Dubai on international best practices for the real estate sector.

John holds a B.Sc. in Economics from the University of Toronto and is a candidate in the Doctorate of Business Administration Program at the University of Toronto and Henley Business School (UK).”

https://www.realosophy.com/about

Clearly no genius; he lacks the deeper insights on critical topics like mullets/skullets, that you have.

Chris

at 2:25 pm

“John Pasalis fails to understand, it doesn’t matter whether the owner is an investor”

Then why did it matter in those areas of the GTA that saw the highest investor activity?

“Cities, and even neighbourhoods dominated by investors are more vulnerable to price declines. This chart prepared by the @bankofcanada used my investor research for the GTA to show the neighbourhoods that had the high rate of investors in 2016 saw the biggest decline in prices.” – John Pasalis

https://twitter.com/JohnPasalis/status/1204780647858003969

Appraiser

at 2:29 pm

@Chris regarding Pasalis.

The “analysis” you quoted is in fact largely anecdotal, based on Pasalis’ personal say-so regarding “every pre-construction condo I sold”

Perhaps Pasalis is attempting to projecting himself as a once prolific pre-construction condo salesperson, which I doubt, especially 10 years ago.

In any case, the sample size he’s referring to would amount to a rounding error.

So weak.

Chris

at 2:33 pm

No, appraiser, that is his opinion in response to those who state that, in their opinion, investors are necessary for the pre-construction condo market.

The entirety of his analysis (link shared in my initial comment) is not at all based on his personal experience selling condos 10 years ago. Please read more carefully.

Kyle

at 2:43 pm

Prices in those areas are either near recovered or fully recovered in just a couple of years. So unless you or Pasalis are suggesting that investors drove prices up, then all exited causing prices to fall and then have since all re-piled in restoring prices back to where they were before the correction, then the reality is it didn’t really matter back then either.

Chris

at 3:00 pm

“Prices in those areas are either near recovered or fully recovered”

Sorry, but that seems to be incorrect.

From Pasalis’ prior research, the four regions of the GTA with the greatest investor activity were Richmond Hill, Markham, Newmarket and Aurora.

Richmond Hill:

April 2017 Average Price = 1,401,145 and HPI = 1,180,900

November 2019 Average Price = 1,046,744 and HPI = 976,000

Markham

April 2017 Average Price = 1,204,092 and HPI = 1,089,200

November 2019 Average Price = 1,051,073 and HPI = 911,500

Newmarket

April 2017 Average Price = 1,037,941 and HPI = 846,300

November 2019 Average Price = 824,272 and HPI = 688,400

Aurora

April 2017 Average Price = 1,269,821 and HPI = 957,700

November 2019 Average Price = 928,232 and HPI = 847,500

Kyle

at 5:01 pm

Fair enough, those areas haven’t recovered yet, but there’s also a big difference between condo investors looking for an income property vs a speculator looking to flip at a higher price. There have been high concentrations of condo investors since well before 2016 and there was no correction to condo prices. So comparing one scenario to the other is a false equivalence.

Also his assertion that there wouldn’t be less supply of new condos without investors, is completely unsupported and patently false.

Chris

at 7:27 pm

“there’s also a big difference between condo investors looking for an income property vs a speculator looking to flip at a higher price”

We’ve discussed Pasalis’ methodology before. His research identified investor purchases as those homes that were bought and subsequently listed for rent through MLS within the same calendar year or first two months of the next calendar year. This methodology would not typically capture those looking to flip at a higher price, unless they rented the home while waiting to re-sell it.

“There have been high concentrations of condo investors since well before 2016”

“We can see this by looking at the volume of new rental and for sale listings over the past 10 years. In 2010, rentals made up 37% of all new condo listings, today they account for more than 60%” – John Pasalis

https://twitter.com/JohnPasalis/status/1204780638819278848

“Also his assertion that there wouldn’t be less supply of new condos without investors, is completely unsupported and patently false.”

You’re misquoting Pasalis a bit here. What he actually said was: “One of the biggest myths pushed by the real estate industry is that without investors, the supply of new condos would plummet.” Nowhere does he state supply would remain static with or without investors – there could absolutely be somewhat less supply. Rather, he purports, based on his experience as a real estate agent selling to end users, that newly constructed supply would not plummet.

Kyle

at 8:39 pm

Who cares if they tried to rent those homes? Do you really think those people were buying to opportunize on the hot New Market, Richmond Hill and Markham rental markets? Rational people would conclude their reason for investing was price speculation, not income.

Also who cares if the number of investors are higher now than 2010? You can clearly see on his graph they are virtually the same now as they were in 2015, yet there was no correction to condos when all other housing types were falling. So if high investor concentration = rush to the exits why didn’t condos correct in 2017?

However you want to interpret his quote is moot, he doesn’t provide any support whatsoever for it. Unlike the very well supported logic that says new supply would plummet in the absence of investors.

Kyle

at 8:47 pm

https://twitter.com/JohnPasalis/status/1204780638819278848

If anything, this graph supports what Appraiser and i have been saying all along. The number of units for lease is actually relatively flat since 2015. What this graph actually says is that the number of units for sale has been dwindling since that same time.

Prices are rising because there isn’t enough supply.

Chris

at 9:21 pm

“Rational people would conclude their reason for investing was price speculation, not income.”

Certainly possible, but equally I would label the Toronto condo investors who are renting out cash-flow negative properties (a fairly substantial number, per CIBCs recent research) to be more akin to speculators.

“Also who cares if the number of investors are higher now than 2010?”

Pasalis. Because he believes this increases the vulnerability of a market to a correction, based on his previous research.

“So if high investor concentration = rush to the exits why didn’t condos correct in 2017?”

Personally, I think B20 had a lot to do with it, but that’s just my hunch. Pushed a lot of buyers down the ladder to smaller/cheaper home types, or even down to renting rather than buying. There was a similar result in Vancouver, where SFD homes fell even while condos continued to appreciate.

“However you want to interpret his quote is moot, he doesn’t provide any support whatsoever for it.”

He provides his opinion and his experience in support. You’re countering it with your opinion. And I suppose some of it depends on what exactly one qualifies as “plummeting”.

Appraiser

at 7:43 pm

Hey @ Chris: Your Guru (Pasalis) is going on an extended twitter rant to defend his anecdotes and conjectures. Here’s a beauty quote from his latest thread:

“because we know that investors are willing to pay more than end users for real estate”

Is that so? Mr. Pasalis, how exactly do we “know” that to be true. Please provide data to support this remarkable theory. No more gut feelings, speculation or personal stories OK, thanks.

Chris

at 9:08 pm

“Mr. Pasalis, how exactly do we “know” that to be true. Please provide data to support this remarkable theory.”

The research he conducted before (showing that the areas with the highest investor activity had the most substantial price declines) would seem to imply that investors paid more and drove prices higher, while fostering extrapolative expectations in the market.

Beyond that, in the tweet you quoted, he also included a link to a research paper from the Federal Reserve Bank of New York, which you omitted for some reason. Did you try checking that?

https://twitter.com/JohnPasalis/status/1204919921014165505

Also, are we now pretending that you haven’t cited Pasalis on multiple occasions as well? I tried to warn you that he wasn’t as bullish as you probably hoped. But sure, he’s my guru…and his even-keeled debate on Twitter definitely constitutes a rant…

Kyle

at 8:50 pm

Clearly, the Government should ban investors from the stock market, starting with the foreign ones, than they should go after those that have more than 1 share.

Clifford

at 7:35 am

It’s all about the supply. Supply is dwindldling while demand is increasing. It doesn’t take a genius to figure out why home prices are rising. Also, hard to compare averages since condos make a bigger chunk of the pie. The $ can be misleading.

I’m more speaking to Chris. Johns anecdotes mean nothing. He’s a huge bear. Reminds me of Garth turner the wear bears would cling to his every word.

Government policy over the last few years in an attempt to address the affordability issue made things worse. Now we have even less supply. We need to stop encouraging the government to meddle in the market. Thry just make things worse.

Chris

at 11:48 am

Supply and demand are not static. This was obvious in 2017, when demand fell and supply rose, resulting in price decline. As outlined above, in some areas of the GTA, these declines have yet to be reversed, even when measured in HPI which adjusts for sales composition.

We can debate whether Pasalis is more bearish or bullish; personally, I think he’s quite balanced in his assessments. But no reasonable person would put him on the same page as Garth Turner. That is just patently absurd.

As to government meddling, this has been going on for decades. Would you also be in favour of taxing capital gains on principal residences, abolition of CMHC mortgage default insurance, ending RRSP withdrawals for first-time home buyers, etc.? Or do you support government meddling when it is stimulative in nature, and only take exception to those measures that serve to cool the market?