This is one of those blogs where the readers get very passionate with their responses.

There are a lot of sharp minds who opine on matters such as the one being discussed today, and whether they agree or disagree, the passion doesn’t waver.

I’ve often said that real estate “fundamentals” are no longer, well, fundamental, since they are somewhat flawed.

For example, the idea that “price growth vs. wage growth” is relevant in 2019, in the Toronto market, is foolish.

I know, I know; I’m a salesman. I have a vested interest in the real estate market going up, and I’m going to shape my narrative to my desires. I’ve heard it before.

It’s also been close to two decades since I studied economics in university. But it’s not like “fundamentals” change over time, right?

The idea behind “price growth vs. wage growth” is basic, and in theory, iron clad.

If wages are increasing by 5%, and the price of real estate is increasing by 10%, then prices will rise way too fast for buyers to keep up. And either debt piles up, or the market will eventually reset. Or both.

Basic, and iron-clad. In theory.

But as I’ve mentioned so many times before, and as market bears hate to admit happens, much of Toronto’s house-buying activity is propped up by this wonderful thing we have called “redistribution of income.”

Yes, this happens, with as much certainty as the cycle of life continuing to spin on.

People work, make money, get older, have more money, then redistribute. And repeat.

And the biggest redistribution of income ever happened when the Baby Boomers approached retirement, and decided to help out their kids. Now fast-forward a decade, and the money continues to flow, whether it’s from the Boomers as they glide into their 70’s, or whether it’s from the 50 and 60-somethings who realize that their kids will never own real estate in Toronto without a helping hand.

I can’t tell you how many of my clients, even those into their early-40’s, are getting financial assistance from their family. I would estimate more than half.

Argue against the act itself, but don’t deny its existence, or its effect on the market.

And then tell me once again why “price growth vs. wage growth” should continue to be the fundamental that we use to evaluate market strength and weakness.

I would make the same argument when it comes to another very well-known, and much relied-upon “fundamental,” which is debt-to-income ratio.

I know, I know; it’s happening again. The shill salesperson is getting ready to sell snake-oil.

But simply put: poor people don’t buy houses.

There aren’t a lot of folks making $120,000 per year who are carrying balances on their VISA at 29% interest. Give me an anecdote, or copy and paste a link, and I’ll tell you that it happens. But for the most part, this 171% debt-to-income ratio is not applicable to a person making $120,000 per year who has $205,200 in consumer debt, and is more likely applicable to the folks on the lower rung of the ladder who will not be looking for a detached house in the Beaches any time soon.

I’ve always had a problem with those two “economic fundamentals” for the two reasons which I just described, and having just read an article in Better Dwelling about the International Monetary Fund calling our real estate market, “over-priced,” I can’t help but think similar thoughts about their “fundamentals” as well.

Here’s the article in Better Dwelling, which is worth bookmarking if you’re not a regular reader:

“The IMF Crunched Numbers On Canadian Real Estate. Here’s How Overpriced It Is”

On Sunday alone, three readers sent me this article, so it’s making the rounds.

As the article explains, the IMF looked to compare average home prices with “attainable” prices, which the IMF defined based on a static borrowing capacity model that takes income, interest rate, and debt into consideration.

There is subjectivity in any analysis, and this one is no different. You can use different averages or indexes for the “observed” price, as the IMF titles it, as well as a mix of many different fundamentals for the “attainable” price. But for now, let’s give the IMF a little credit and assume they know what they’re doing.

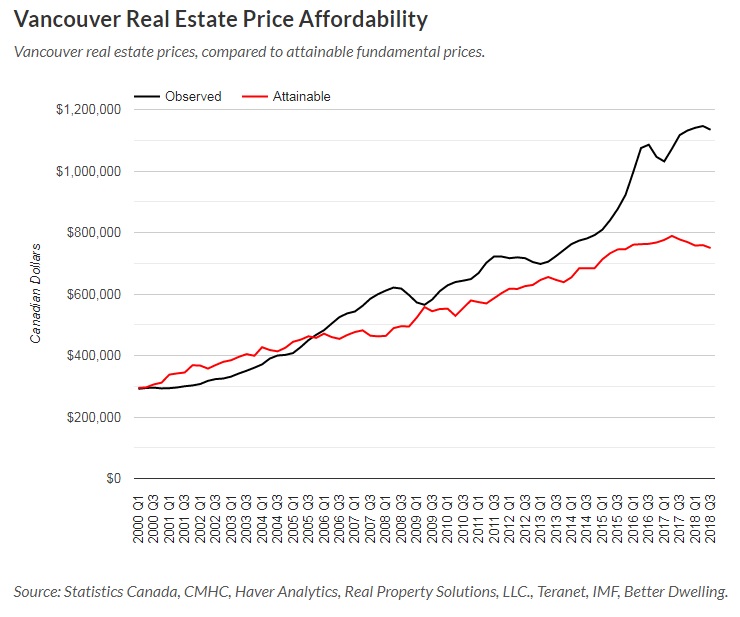

According to the IMF, the “observed” price is 54.7% higher than the attainable price in the city of Toronto:

–

Now if you showed me this chart, and didn’t tell me what the black and red lines were, I would have probably figured out that this had something to do with the real estate market.

And once we see the labels on each axis, and the definition of the lines, this starts to make sense. Especially as you see the decline in the black line in 2017.

But my gut-feel on the market and affordability wouldn’t have shown a disconnect starting in 2009. It’s really only been in the past two years that my buyers have started to feel the pinch, and again, I think this is because of how statistics can tell a different story than in-the-trenches experiences.

According to the IMF study, Toronto had the second-highest “disconnect” between observed housing prices and attainable housing prices.

Hamilton was #1 on the list with a 57.1% gap.

Vancouver finished a distant third with a mere 51.3%:

–

Now it’s not so much the charts, the stats, or the opinions therein that interest me.

For example, the author of the Better Dwelling article refers to the SBC model as “the price the broad market can support,” but I might argue with that conclusion. The author mocks the age-old real estate theory and saying, “the price someone pays, is the price of a home.” I get it, I do. But for everybody that had predicted a market crash in 2003, or 2007, or 2012, or 2016, I would ask, “How are the fundamentals stacking up against what’s actually going on in the market?”

So I went to the IMF website and found one of their “working papers” called:

“Assessing House Prices With Prudential And Valuation Valuation Measures”

In the paper, the authors describe how they come up with the Static Borrowing Capacity, and here’s where I might lose some of you, but I also might make some new friends!

This is from the paper:

The borrowing capacity approach should sound familiar. Inspired by the behavior of prospective home buyers, it indicates how much housing households can attain. It derives the maximum size of the mortgage loan that a household can safely borrow, given their income level, market interest rates, and a share of household income to be allocated for the mortgage payments. We assume the average household is credit constrained. Together with their available down payment, the mortgage loan indicates how much housing the households can afford.

This simple calculation is the way many households determine the size of an attainable mortgage, using a simple calculator on the internet. We assume that each household will reach for the maximum housing they can afford given their income level, the market interest rates and their down payment. All that while respecting the limits on loan-to-value (LTV) and debt service-to-income (DSTI) ratios set by the regulators. Available data for many countries, including the Czech Republic, show the distribution of LTV and DSTI ratios bunching around the prudential limits set by the authorities.

Borrowing capacity analysis is not a valuation approach but a prudential, liquidity-constrained approach. Its application can be particularly useful to macro-prudential authorities for deeper exploration of house price dynamics, or as a tool for counterfactual scenario analysis, and a communication vehicle. Within a macro-prudential context, an analogy can be made to road speed limits. Surely, a small violation of the speed limit rarely results in an accident, similarly as driving below the limit by no means guarantees full safety. Nevertheless, setting road speed limits represents a generally accepted prudential measure. Similarly, borrowing capacity approach provides a reasonable macro-prudential level of house prices that are consistent with sustainable household borrowing, low mortgage delinquency, and resilient financial sector. Regular communication of such a metric and its transparency may help anchor expectations of relevant market participants (banks and households) about the future course of macro-prudential policy.

It’s interesting that in this explanation of Static Borrowing Capacity, they as much as admit that it’s not necessarily accurate.

The “speed limit” analogy is a perfect one. They’re essentially saying that what will eventually become the “attainable house price” doesn’t serve as a point at which extending further will automatically harm the borrower.

Later in the paper, the authors put their tools to use in analyzing the real estate market in Prague in the early 2000’s, but ultimately conclude that what their research shows should have happened does not add up with what actually happened in that market.

Here’s a note from the paper:

In our experience, applying simple time-series regression model to Czech housing market does not lead to satisfactory answers. The estimated coefficients are often at odds with theory

(wrong signs) and they are unstable, which causes frequent revisions of view about overvaluation.

I smirked when I read this, to be quite honest, because it makes me think of every single market bear in Toronto in the past ten years.

“Does not lead to satisfactory answers.”

Yes, said by every market bear in the last decade.

It must be frustrating, right?

To be so smart, and know so much, and have so many statistics and fundamentals that point to this catastrophic real estate market collapse, only to see it continue to rise?

The end of the paper gives us this piece of insight into why prices and fundamentals might diverge:

Reasons frequently associated with the observed prices moving away from fundamentals are the factors causing severe demand-supply mismatch. Factors ranging from demographics to local zoning rules, not-in-my-back-yardism, and supply constraints. Although a closer inspection of insufficient supply and supply-side constraints goes beyond the scope of this paper, we note that such analysis warrants some caution. In particular, the comparison of change in the number dwelling completions and households will not necessarily provide a clear proof of supply imbalance. This is because the observed data can suffer from reverse causality. Only the households who find and purchase a dwelling settle in and register in the city, thus entering the population statistics. This can make the completed dwellings and change in households co-move together, while the market tightness remains. This has clear implications for the modelling framework and input variables used therein.

The IMF publishes all kinds of working papers and notes that these papers aren’t the opinion of the IMF, but rather their publication is to promote discussion.

I find all of this fascinating, maybe because I’m surprised that the way the world is going in 2019, the authors of this paper weren’t busy watching The Kardashians, but also because it sort of felt like two guys trying to reach a conclusion based on their own assumptions, only to have the data tell them something different.

Like I said above, it’s similar to the story of the Toronto real estate market.

And while the Better Dwelling article refers to Canadian real estate as “overpriced,” and the IMF provided the data to come to this conclusion, I really, truly believe that “overpriced” is a term based on opinion, and that the market pulling away from so-called “fundamentals” does not necessarily mean that market is overpriced.

Can fundamentals change over time?

Can some fundamentals become obsolete?

The Toronto real estate market might suggest as much…

Appraiser

at 9:05 am

Here’s a similar article from the IMF from 2012:

https://www.businessinsider.com/imf-sees-a-bubble-in-the-canadian-housing-market-2012-1

Here’s another from 2014: https://www.cbc.ca/news/business/td-bank-imf-say-canadian-real-estate-10-overvalued-1.2521476

Heres one from 2015: https://globalnews.ca/news/1873881/imf-warns-over-canadas-overvalued-housing-market-again/

And yet another headline from from 2017: “The IMF warns of significant risks from Canadian housing market” Globe and Mail (no link, subscribers only)

Seems like the IMF has the same mentality as the bears out there – just keep dancing until it rains.

Frank

at 9:28 am

Interesting topic today.

I would agree that most academics spend their whole lives writing papers and doing studies and never enter the real world. This example of two think-tankers trying to apply their hypothesis to PAST market dynamics, and coming up incorrect, demonstrates why so many accepted theories are flawed.

I would also agree that it’s far more accurate to look at what the Toronto market has done rather than what it should have been doing all along. That’s a no brainer. Although it would seem market bears didn’t get the memo.

Kyle

at 9:42 am

Benjamin Tal, aptly described this type of Analysis as “Mickey Mouse”. Looking at the relationship between two variables over time is basically useless for predicting or explaining what’s going on in the real world. It is however really great for helping people convince themselves that reality is wrong rather than their beliefs.

Libertarian

at 9:54 am

Just goes to show you that sometimes, too much education is a bad thing. These people spend their entire lives in academia trying to figure out stuff. Here is Canada, what a waste of taxpayer dollars!!! Too bad education reform isn’t on the ballot in today’s election.

Professional Shanker

at 12:37 pm

I think largely most economists have underestimated the yield curve and return to higher borrowing costs which haven’t happened over the past decade. This is what their underlying models are based no?

Libertarian

at 4:43 pm

Not sure whether your comment was meant for me. I’m not challenging their models. These people are a lot smarter than I am. I just think all this analysis is a waste of time because, as David says, there is theory and then there is reality.

Toronto real estate is expensive for a whole whack of reasons. Unless all of those change, it’ll remain expensive. We don’t need economists with PhDs to tell us that. But hey, they get paid a lot of money, so they can afford to buy here in Toronto. University tuition goes up, OSAP loans go up, the unions go on strike for more pay, etc., etc., all so we can have more useless analysis and more English Lit and Art History grads complaining they can’t find a job or afford a house in Toronto.

J

at 9:56 am

“If wages are increasing by 5%, and the price of real estate is increasing by 10%”

There is a big difference between saying “the market will forever be valued X% higher than what fundamentals suggest” and the “the market will forever rise 5% faster than fundamentals every year.” I think most people could accept some possibility of the former even if they deem it unlikely, but the latter is just ludicrous. The latter is suggesting that prices will keep getting exponentially more and more detached from fundamentals over time.

“much of Toronto’s house-buying activity is propped up by this wonderful thing we have called “redistribution of income.””

By “redistribution of income” I think you mean “redistribution of wealth.” Wealth is another kind of fundamental, so I’m not sure this is really an argument against real estate being driven by fundamentals. But in any case, this raises the question of the origin of the funds being redistributed to the next generation, and whether it’s really wealth. If the funds truly originate from accumulated wealth that is one thing, but if the funds are from a HELOC, deferring retirement or making other sacrifices, then it resembles a ponzi scheme. No doubt it’s a combination of both.

Mike

at 10:05 am

Good point about where the “wealth” is coming from. Is this cash sitting in the bank account of a Baby Boomer? Or is it an equity takeout on a primary residence to help little Johnny or Janie? Is live to see data on this. Or if David can speak from experience?

Appraiser

at 11:44 am

Early wealth distribution is nothing new. Many boomers (self-included) think it makes a great deal of sense to help their kids when they are relatively young, instead of waiting for inheritance.

Professional Shanker

at 12:32 pm

If it is nothing new, then am I correct that you do not believe that the rate and amount of early wealth distribution has increased in recent years?

Appraiser

at 1:05 pm

Of course it’s more prevalent due to the abundance of boomers. You know – the pig in the python, statistically speaking.

Kyle

at 10:30 am

Excellent Comment J.

Obviously there are fundamentals that underpin the market, but the question is whether the particular set of simplistic bi-variate fundamentals oft-trotted out and held above all else by the bears are good representations of what those true fundamentals are. Given their correlation with reality i would say, no. I think the way to interpret those simplistic bi-variate relationships is that there is a theoretical upper bound to which things can diverge, but most bears consider these historic bivariate relationships to be the actual driving force behind the market. I’ve even heard some bears refer to it with the same certainty as gravity, which is clearly wrong.

On the income vs wealth redistribution, it is a very interesting point. Wealth is being leveraged to create more wealth, like a ponzi scheme. However what causes ponzi schemes to break down, is when there aren’t enough people to prop up those who came before. I think even the bulls would agree, if Toronto’s population/number of households shrank, or the number of people who could afford to buy homes dropped, prices would then follow. But as long as the population and number of households are growing, and the number of jobs is growing, then that creates immediate demand and that’s what drives the market in real time (unlike those bivariate relationships which don’t actually drive anything).

Professional Shanker

at 10:41 am

J – The bulls on here do believe in the possibility that “the (Toronto core) market will forever rise 5% faster than fundamentals every year.”

If the majority of the recent price increases have been supported by expedited wealth transfer, lower borrowing costs, foreign capital, etc (name the driver) what other factors remain to ensure price increases will be greater than “fundamentals” so to speak? Just because?

This type of rationalization is typical when we are about to enter a downturn/recession, will reductions in borrowing rates be enough, history says no but perhaps new normal will exist….

Appraiser

at 11:37 am

Still clinging to the “recession-gonna-come” last hope eh?

Of course, that’s when it rains!

Professional Shanker

at 12:34 pm

Trying to paint me as a doomsayer, nice try but I am far from it, just a RE bear living in a QE world!

Appraiser

at 1:25 pm

Only a deeply biased orientation or clinical depression can invoke the risk of recession when all of the important economic indicators in Canada are positive or on target.

You know like: employment, wage growth, GDP growth, inflation…

Professional Shanker

at 2:00 pm

What is your guess then?

You don’t follow metrics like yield curves do you?

Appraiser

at 3:29 pm

Voodoo “metrics” such as inverted yield curves do not cause recessions. Real world issues like massive plant closures, layoffs and skyrocketing interest rates on the other hand…

Correlation is not causation.

Professional Shanker

at 3:34 pm

You are correct, an inverted yield curve does not cause a recession, it only predicts it.

Verbal Kint

at 12:23 pm

$120,000/year income *IS* poor people.

Appraiser

at 1:43 pm

Two teachers / cops / paramedics / nurses with 10 years experience make about $200,000 / year.

A married couple working full-time at the Chrysler plant in Brampton easily brings in $160,000+ / year, without overtime or weekends.

$120,000 / year is certainly not rich in the GTA.

Izzy Bedibida

at 3:40 pm

That’s true. Many years ago I bought a condo in Woodbridge at 4x my $60K/yr earnings. This year I finally hit $100 K/yr and that same condo is now 6x my earnings. Some of the detached houses in my area of Woodbridge are 10x my current wage.

The government considers me well off and taxes me accordingly, but I couldn’t afford to buy back my current condo.

Tudval

at 3:43 pm

Respectfully if I may, I would like to point out that after ‘many years’ getting from 60k to 100 k is not all that remarkable. Many career oriented people more than double their salary in 15 years (i think 15 or more is about what most would think as “many”)

Classical Economist

at 4:11 pm

Real estate is not governed by classical economics of supply and demand.

If there are 4 houses for sale and 15 potential purchasers, the market doesn’t create 11 new houses to clear the market at the median price.

This means the market is made on the margins.

So those rich foreigners? They get the house.

Bay street banked on $450,00 a year? He gets the house

Law firm partner on $600,000 a year? She gets the house

Couple making average but gifted $900,000 by their parents? They get the house

Say it with me: Average. Has. Nothing. To. Do. With. It.

The “marginal” bidder wins.

Is it shitty? Yeah. Can you do anything about it? No.

Kyle

at 10:23 am

“Say it with me: Average. Has. Nothing. To. Do. With. It.”

This is so bang on and explains Appraisers first comment about how the IMF has been wrongly calling Toronto’s “over-valuation” for half a decade. Bottom line – their “fundamentals” are garbage. Median income earners can’t buy real estate in large cities, so stop using them as the benchmark for what pricing should be.

And anyone who keeps buying into these articles should be asking themselves why they keep believing in something that has no relation to reality. I think a lot of the belief perseverance in these articles comes down to an inability for many to accept your last sentence.

Professional Shanker

at 12:10 pm

“Real estate is not governed by classical economics of supply and demand” Economic theory includes the concept of a marginal buyer.

As most people have correctly pointed out, wage increases can be supplemented by other sources (wealth transfers, income outside the domestic economy, etc.) for a SPECIFIC PERIOD OF TIME, not forever. Is it your believe that the marginal buyers are infinite and will only come to Toronto/urban cities to purchase real estate?

Appraiser

at 1:03 pm

There is no time limit on wealth transfer. It will slow down only when the boomers are done, which could be a while yet; and continue at a slower pace thereafter.

Nothing new.

Joel

at 1:32 pm

Very well put.

condodweller

at 12:26 am

David, I’d be curious to know if you are putting your money where your mouth is. You have stated in the past that in 50 years no one is going to be able to own their own home due to continuous RE appreciation and now you are saying that fundamentals should be ignored as they can’t be relied upon as prices will continue to increase into the future.

Based on your statements and beliefs you should be buying RE hand over fist whenever you can. As a successful RE agents it should be possible for you to acquire several new properties, in the least, per year.

I have met many RE agents who have stated as much and have been buying RE over the years, though I’m not sure if they are still continue to buy these years. I recall the old big city broker show with Brad Lamb where back then he and his team were buying condos which they only sold when they needed the cash to purchase more units. I wonder if they are still doing this.

So, without disclosing exact numbers would you care to share with your readers to what extent have you, and are you still investing in RE? Perhaps in % of your disposable income or whatever metric you feel comfortable sharing.

I have great respect for those who make bold calls and back them up with action.

David Fleming

at 10:15 am

@ Condodweller

Wow, that’s a very personal question! I don’t know if you can get any more personal than that, but in a compeltely unrelated story, I didn’t lose my virginity until I was 19-years-old…

I have my money in real estate, but not in the form you are referring to.

I invest my money in private mortgages, mainly second mortgages at 11.75%. I’m aware that cynics will point to the “risk” but if I happen to work with an extended family member, with 30-years experience, who maxes out at 70% LTV,, buys out the 1st mortgage from the bank in every case of default, etc, etc, etc, this isn’t the same house of cards as you read about in business school.

My primary residence is not my only piece of physical real estate, but unfortunately I do not have the time or the desire to manage a dozen downtown condos like the agents you describe above. I choose to take a lower rate of return (at least in bull real estate years) but one that requires no effort on my part, and is still double what a “great” return would be considered if acheived in perpetuity.

Any real estate I own will be held long-term in a family trust (thank you Trudeau/Morneau for keeping that door open for your hypocritical, self-serving needs…), since I am incredibly bullish about the long-term prospects of Toronto’s market. Yes, I do believe that a “crappy” 1-bed, 1-bath condo that’s worth $500,000 will cost $1.5M when my kids are 20-years-old, and so they won’t be able to afford it on their own.

condodweller

at 12:39 pm

Thank you for you honesty David. Money is personal but I was simply curious about the philosophy and general asset allocation of a bullish RE agent, I wasn’t asking for your net worth.

I was expecting that you’d own more RE based on your bullishness but I can’t say I’m surprised.

That’s quite a dig at the Liberals, I can’t wait to read your first post re the election results.

I truly hope you are wrong about 1 bed condos being worth 1.5 million in 20 years for the sake of the general population.

David Fleming

at 1:14 pm

@ condodweller

I don’t really want to delve into politics today, but am I wrong about Justin Trudeau and Bill Morneau? They are both exceptionally rich, top 1% of 1% of 1%, and have closed every door to keeping wealth save for ONE, which they both utilize. That’s not a dig, but a fact. My calling them “hypocricial” is based on their continued attempts to redistribute income, while salting away their own.

I’m not going to blog about the election. Yes, I’m a Conservative, and I’m not happy today. I don’t like Andrew Scheer at all, but I dislike Justin Trudeau more. If this is what Canada wants, then so be it. Let’s see who is better off in four years, because I honestly don’t believe the “average” person will be.

Condodweller

at 9:01 pm

I didn’t say you were wrong, I just said it was quite the dig. Perhaps I need to look up the definition of dig, but I wasn’t disagreeing, or agreeing with you. Now I sound like a politician 🙂

Dan

at 11:04 pm

Can you clarify what tax benefit they’ve kept open?

Dan

at 12:25 am

Due to inflation, wage increases, low interest rates, as well as the ease that wealth is able to move countries, yes property values have and will most likely over time. But $1.5mil in 20-30 years? At least at current condo property values can be rented at high prices, but the increases have been slowing down. Also.. doesn’t Toronto have a ton of room for density and further development? I’d feel more comfortable owning a house long-term.

condodweller

at 1:29 am

I happen to be one who believes in fundamentals. I suggest that fundamentals haven’t changed they simply have been delayed by other significant factors such as the wealth transfer/wealthy immigrants/high income earners.

When David states that fundamentals are broken and they are no longer relevant he is basically saying the that IMF’s attainable price is too low, i.e. the population is getting money from sources the IMF hasn’t calculated in (I haven’t read the article and assume they have not factored in the wealth transfer factor which I agree has an effect).

I suggest that it’s not the fundamentals that are broken but the way they are calculated. If the normal formula uses income/debt/assets to calculate the maximum price the population can afford, or at least the marginal population which could afford current prices then that price should be the limit. The question becomes how much extra funding are these marginal people obtaining through the wealth transfer and how much is the actual attainable price. There is a disconnect between the theoretical attainable price and the actual attainable price. Basic logic would suggest that the actual attainable price is the current observed price, would it not? I mean we wouldn’t have the current price unless someone has actually paid it.

The million dollar question to me is to what extent is the wealth transfer propping up observed prices and the two million dollar question is how long can it support it??

I mean the higher the observed price goes, the greater the wealth transfer amount has to be and assuming the amount wealth available to be transferred is finite there has to be a limit. I again suggest that the observed price will have to reach a max at some point after which it can only decline. I don’t know when it will happen, but in my mind it’s a mathematical certainty. It’s 1:25 in the morning. Am I missing something obvious?

Batalha

at 3:10 pm

“I again suggest that the observed price will have to reach a max at some point after which it can only decline.”

Or it could simply plateau. Again, speculation on all sides.

Condodweller

at 8:47 pm

Incorrect, when the funds run out, the then current prices could not be sustained therefore it will decline.

Jimbo

at 7:01 pm

The attainable price is Amount – Down payment + Mortgage.

There may be a limit but if you are only borrowing 5% of your property value to loan your child it is feasible that it could go on indefinitely. 5% of 2 Million is $100k, not much of a mortgage for the parent and it gets your child in the door for a $500k property that always goes up in value.

Even if it declined who cares, the loaned amount is a small payment and you have the equity to be safe.

Condodweller

at 9:06 pm

I agree, it can go on for a long time, but I don’t think it can go on forever. Note that by the time people have paid off their mortgage and are established enough to support their kids the kids are old enough that they may not need the support. I think often it’s the Grandkids that are supported, and there can be many of them…

Jimbo

at 1:16 am

I would tend to agree with that thought process, but 40 year olds are getting help from their parents to get in the market as David said.

My guess is the rental stock will grow in time and provide a better spot for people to move to.

My time in the states I was always blown away by the number of new rental properties available with all amenities including AC. If Toronto fails at the policy needed to encourage rental property growth then the city will be a bigger traffic nightmare than it is and growth will be hampered.

Batalha

at 3:42 pm

David, why does it matter whether or not you “like” Justin or Andrew or Jagmeet or Elizabeth or any other party leader? If you prefer Conservative policies to Liberal (or, needless to say, NDP) policies, which you apparently do, why does it matter whether or not you “like” that party’s leader, or your local candidate, for that matter? And what does “like” even mean? Feeling you could have a beer with him/her? Who gives a damn?

Please excuse my somewhat exasperated tone, but I’ve simply never understood the seemingly near-universal obsession with “the leader” as opposed to the policies of his/her party, i.e. what will they do if they gain power? Leaders pass away, policies often (usually?) live on. Which matters more in the long run would seem to be obvious, however the real world of voters tells us a different story.

Jimbo

at 7:03 pm

Not all leaders apply policy the same, not all leaders can gain the support need to ever get a majority. I can see where people dislike the leader.

Condodweller

at 9:12 pm

I’m always amazed at how many people don’t vote for some one simply because they don’t like them. By “like” I mean superficial things like the way they look/speak and their mannerisms. Yes you wouldn’t want to have a beer with them could be a good test. These people don’t even have any idea of what their platform/policy is.

IT Consulting

at 10:55 am

Hello everyone, it’s my first pay a visit at this web page, and paragraph is actually fruitful in support of

me, keep up posting such content. https://www.mrfeudalsnews.com/2017/03/31/lets-play-stonehearth-ep3/

Brian

at 1:44 am

Real estate prices in many markets worldwide (including GTA’s) have also been enhanced, directly or indirectly, by the various Quantitative Easing measures (in all shapes and sizes) adopted by various countries and regions, more notable ones being the USA, China, Japan, EU etc., among other factors. When fiat money becomes ‘cheap’, people seek assets, real estate included. Many boomers have gained financially in the process and are thus able to help the younger generations via ‘redistributing’ their wealth.