I find these year-end, and start-of-the-year blog posts to become somewhat expected.

But having said that, I’m also a sucker for discussion of potential future events. Not necessarily “predictions,” but rather a prudent, yet somewhat speculative, look at issues that lay ahead.

While most media members, financial advisors, and economists simply want to pick a percentage, add it to a DOWN-arrow, and tell us how much the market is going to crash this year, as has been the case every year for a decade, I want to talk about issues that I feel are going to be topics in 2017.

I thought a lot about real estate over the holidays.

I know that’s pathetic, but it’s also unavoidable.

To be quite honest, I’m not really sure how to “relax.”

I feel as though “relaxing” by definition is doing nothing. It’s watching TV, reading a book, swinging in a hammock, etc.

Well, it’s too cold for my outdoor hammock, and channel-surfing between “Con Air” and “Die Hard II” on a Wednesday afternoon during the holidays makes me far more anxious than sitting in my office at 290 Merton Street, taking care of some business.

To me, the ideal “relaxing day” would be sleeping in a little bit, walking out to get my morning Tim Horton’s, driving to the office to tackle maybe 3-4 hours of work, hitting the gym, running a few errands and getting a few items crossed off my “to-do” list, taking the dog for a walk, and spending time with my newborn baby. I know, I left that for last, and it’s questionable. But you don’t really “relax” when you’re trying to soothe a crying baby, so I’m just being honest; but it’s part of the overall day.

I suppose we all have different definitions of “relaxing.”

But I think the underlying theme in “relaxing” is to be without anxiety, without tension, and in your own state of calm. The crying baby doesn’t really get you there, does it? 🙂

I’m loving fatherhood thus far, and trying as it may be, it’s fun to look ahead.

Maybe that’s a running theme of mine – looking ahead.

Because over the holidays, I found myself pondering what 2017 has in store for us on more than one occasion.

I can’t stomach the discussion, or even thoughts of what the USA and Donald Trump are going to show the rest of the world. “I can’t…” seems to be the favourite phrase among those who just don’t want to discuss, or deal, with the reality. My wife has family in Atlanta, and they just keep saying, “…..I can’t…..I just…..let’s talk about something else….I can’t…”

I’ve thought a good amount about what the 2017 Toronto Blue Jays will look like, and while I’m not a pessimist, I am a realist, and I feel this piecemeal squad might contend, but will ultimately disappoint.

And alas, I’ve thought a ton about what the 2017 Toronto real estate market is going to do, what it will prove, and what, if anything, it will provide.

In 2017, as was the case in 2016, it’s hard to look at Toronto without looking at the rest of the country, and a lot of my thoughts on our city’s market will be intertwined with thoughts, or examinations, of what’s going on outside Toronto. Look no further than CMHC policies aimed at Toronto and Vancouver, for the affect they’ve had on other markets.

So as was the case at the end of December, I’ve sat down and come up with a long list of topics I think will make headlines in 2017, and whittled it down to five.

I think a deeper examination of the top-three topics is probably more helpful than a quick mention and no analysis of the top-fifteen topics, so without further adieu, this is what should be on your radar in the year ahead.

1) Toronto Prices

Perhaps I could have left this to last, since nobody really wants to start the year with something so depressing.

But! There’s a but!

If you own your home, and you’re never going to move, then you’re laughing all the way to the bank.

Okay, well, 99.9% of people reading this will move again in their lifetime, so sorry for that.

But there’s no denying that the biggest story in 2016 was the average home price, and that will continue to be the biggest story in 2017, in my opinion.

The December numbers won’t be available until the end of the first week of January, so much of what I write today will be based on the November numbers – just keep that in mind.

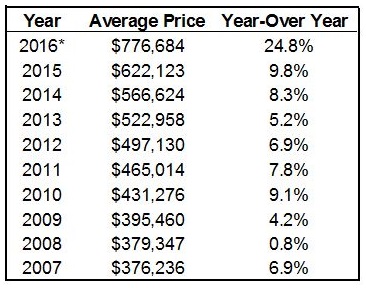

The average home price in 2015 in Toronto was $622,123.

The average home price in November of 2016 was $776,684.

That’s a ridiculous 24.8% annual increase.

Some of you are reading this and thinking, “And the market is only going to move higher.”

Others are looking at this and saying, “See – this is why the market is heading for disaster in 2017!”

Pick your poison.

Bulls versus bears, etc., etc.

I can probably make a case for both: a) the market increasing in 2017, b) the market declining.

But first thing’s first, let’s look at the average sale price and the year-over-year increase in the average sale price in 2016, and put it in perspective when we compare it to each of the past ten years:

Hmmm…

One of these things…..well….it reminds me of Sesame Street…

Except there would be more cookies on that plate.

A 24.8% increase, eh? How ’bout that.

But I fail to see how one could argue this will lead to a decline in the 2017 average home price, simply based on current market activity, demand, and interest rates.

Now just for fun, I’ll provide the bears with this chart, and give them all the ammunition they need to formulate their arguments:

There’s a lot to work with here, folks!

The bears might argue that in 1986, the 27.3% increase led to a downturn.

Of course, the bulls will argue that the 27.3% increase was followed by THREE more years of double-digit increases in average home price.

We should also note that in 37 years, the average home price has only decreased 6 times. Perhaps that’s a sign of an undervalued city?

In any event, the average home price in Toronto hasn’t declined in two decades, and that’s not going to change in 2017.

–

2) Government Response To “Crisis”

This naturally flows from the above, doesn’t it?

In 2016, we saw the government try to “address” the housing crisis.

Crisis. Is it a crisis? Who gets to decide?

Is it a “crisis” when politicians are politicking and need to make a point?

Or is it just “reality” when we sit back and look at a growing population, massive net migration into the largest Canadian cities, and an imbalance between supply and demand?

What we saw out of Vancouver this year would make it look like a true “crisis.”

The provincial and municipal governments spun their wheels as fast as they could to gain favour with residents (ie. voters), and instituted the 15% foreign buyer’s tax, and the vacancy tax.

And they also announced they would “lend” first-time buyers money for their down payments.

There could be more changes on the way in 2017, with a provincial election looking on May 9th. The Liberals have held office since 2001, through four elections. So does that mean they are more, or less likely, to do something drastic to hold office for a 5th consecutive time?

Of course, we here in Ontario know all about politicians struggling to gain favour. Our Premier, Kathleen Wynne, has seen her approval ratings drop to 14%, and as I wrote in my year-end blogs, I think that’s led her to “give back” to Ontarians, looking for votes.

She’s given back $2,000 in land transfer tax to first-time buyers.

What else will she do in 2017 to help her 2018 re-election campaign?

Excuse my cynicism here, folks. If I’m making it sound like I believe that every single decision a politician makes, is politically-motivated, it’s because, well, I do.

Public policy might not be borne out of politicking, but it’s often in response to public outcry, as we saw in Vancouver.

And I think in 2017, both Ontario Premier, Kathleen Wynne, and Toronto Mayor, John Tory, are going to enact a lot of policies in response to the growing frustration among Toronto residents when it comes to home prices.

I can only speculate as to what policies they will enact, or as is often the case, promise to enact.

But I think we’re going to see a lot of talk about “affordable housing,” which should be directed at the lowest-income earners, even though the irony is – everybody in Toronto is looking for something “affordable.”

It might be time to look at the role of TCHC, and determine if what they do, and how they do it, is the most effective use of tax-payers money. I mean, I would suggest that having a family of five live in a $1,000,000 house is not the most efficient use of tax dollars, but that family, who has been living there for free for a decade, might call the Toronto Star and pout in a front-cover photo, so that might not be a boat we want to rock.

For years, we’ve seen the government approve condominium developments – many of them massive in size relative to what’s around them, in exchange for a couple of units earmarked for lower-income families. Maybe the city will grow some stones, and ask for more from developers than they’re already asking? Don’t worry – it’ll only drive up the cost per square foot for investors…

I wrote a blog last year October about developing the Greenbelt. I didn’t really take a side on the issue, but rather posed the question of whether or not it’s time to even consider discussing it. Perhaps 2017 is the year when this idea will gain favour.

I actually had a dream around Christmas-time that the Don Valley Golf Course was turned into a sub-division.

I woke up and laughed about it in the shower, but by the time I got the shampoo out of my hair, I started to wonder whether or not an idea like this could, eventually, make sense.

The Don Valley Golf course isn’t exactly a money-maker for the City of Toronto, and the city, with all of its problems, shouldn’t argue that there’s any responsibility to provide a “public option” for golfers.

The course isn’t a great one either. It’s short, easy, not very scenic, not well-kept, and is frequented by beginners and people looking to drink at 4pm on a weekday.

It’s also only utilized five months per year.

There’s hundreds of acres of land that’s owned by the municipality, and could, in theory, be used to house the city’s residents, at one point or another in the future.

Crazy idea?

Or is this the highest and best use of this public space?

I think as time moves on, our three levels of government will need to get more creative to address our housing “crisis.”

Unless they start to round people up and move them out of Toronto and Vancouver, the city’s populations will continue to swell, and with limited space for new housing, something has to give.

This is going to be a big story in 2017, and it will be interesting to see how the three levels of government respond.

–

3) Rental Market

I’d say that roughly 99% of the blogs I write, and the conversations we have here on TRB are with respect to the purchase and sale of real estate, as opposed to leases. Maybe that’s because leasing isn’t as sexy a topic, but it’s certainly not because 99% of my readership are buyers.

In fact, I get a lot of emails from readers asking for me to write more about the rental market, or even answer specific questions they have.

The truth is, I rarely do leases on the lessee-side.

I lease out a lot of units for my investor clients, but it’s been years since I’ve been pounding the pavement with tenants.

So perhaps I’m desensitized to how tough the rental market is out there for young people trying to secure their first property for lease. But as I wrote a few times last year, I do hear all the stories from young agents in my office – about multiple offers on leases, and how tough the market is.

Recall a blog I wrote back in November called, “What The Heck Is Going On In The Rental Market?”

The company Urbanation shared their statistics with us, and half of their presentation was on the skyrocketing rental market.

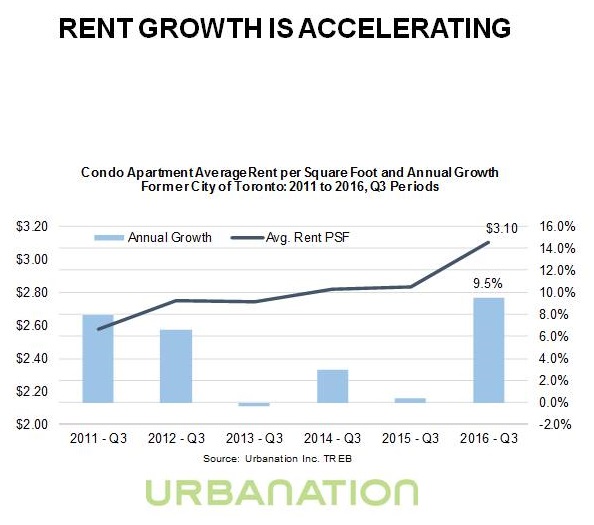

The most interesting statistic, in my opinion, was the massive increase in average rent per square foot in 2016, as shown here:

It’s not just the increase, but the rate at which rents are increasing.

If you look at the chart above, and take increases from 2011, it’s nothing compared to the average house price.

The average house price in 2011 was $465,014, compared to $776,684 in 2016 (November). That’s a 67% increase.

Meanwhile, the average rental per square foot was $2.62 in Q3 of 2011, and $3.10 in Q3 of 2016. That’s an 18% increase.

But if you look specifically at the last year – $2.81 per square foot in Q3 of 2015, compared to $3.10 per square foot in Q3 of 2016, you see a massive 10.3% increase in one year.

We know that the average house price has increased 20-something-percent in the past year, so a 10.3% increase in rents seems insignificant by comparison.

But when you consider that rents have only risen 18% in five years, and 10.3% was in the last year, suddenly the increase is more than significant; it’s crippling to some would-be renters.

For a young person considering a condo at $1,450 per month, only to see that same condo cost $1,600 per month the next year, it can take them right out of the market.

Imagine that.

For folks who wanted to buy, it’s too expensive, so renting is the answer.

And now with rent prices increasing 10% year-over-year, many people can’t even afford that.

With condo prices expected to rise again in 2017, it will be quite interesting to see how closely downtown Toronto condo rentals follow suit.

Perhaps this means that 24-year-olds living at home will have to wait until 26, or 27, to make the move.

–

So there are the “Top Three” stories in my mind, but there are a lot more topics worth discussing.

Why don’t we regroup on Wednesday and take a look at other, smaller, yet important issues for 2017.

Kyle

at 9:52 am

One topic that i think will be discussed much more in 2017 is laneway housing. If the City decided to change zoning to allow for laneway housing, the 250 kilometers of laneway in this City could translate into a lot of highly desired low-rise housing. And it would add density to our neighbourhoods, without having as big an impact to “the character of the street” as say a townhouse complex or multi storey condo.

Unlike the restrictive interventions that the Government has tried to use to cool prices, laneway housing would actually help reduce prices by increasing the type of supply which is most needed (ground-oriented). While also increasing economic activity, jobs, density, property tax base, etc. And because there is an economic incentive for existing home owners to add laneway housing, the increased density won’t be met with the same fierce NIMBYism from other home owners.

TeeGee

at 10:14 pm

Fully built out laneway housing could add 6,000-7,000 units to downtown. Not insignificant, but not enough to really move the needle either.

Kyle

at 9:29 am

Agreed that it won’t be a panacea and it certainly won’t be enough to return ground-oriented housing to affordability, but that is not to say it isn’t worth looking at:

1. “Affordability” is often only looked at only in terms of # of units and avg $/unit, but that doesn’t really capture the true plight of affordability. One of the keys to increasing affordability is actually creating more options for people, not so much about the # of units or avg $/unit (i.e. by simply offering more types of homes and tenureship options, you can increase affordability). For example a family who earns $250K/yr may very often has more trouble finding something they can afford than a single person making only $125K/yr. This is where laneway housing can help. It adds a completely new housing form that doesn’t currently exist in this city.

2. When the city created the laneway survey to get public consultation, one of the ideas that was put forward for feedback, was to expand it beyond laneways, and to include houses with driveways. Basically anywhere a detached garage could exist now could be in scope. This would actually increase the potential well beyond 6000-7000 units.

3. An additional 6000-7000 units may not seem like that much, but it is all relative. When compared to the current number of new ground-oriented infills being created in the core, it is relatively large. And compared to the ground-oriented rental/resale market (where you can live in the whole building and not share the roof) it is absolutely huge:

“In a city of almost three million people, only 537 detached homes were listed for sale on the Toronto Real Estate Board at noon Wednesday.”

http://www.cbc.ca/news/canada/toronto/toronto-detached-homes-demand-1.3914667

Ralph Cramdown

at 11:38 am

From what I can tell, Vancouver’s laneway housing initiative is a rolling disaster. Permits are around $35k (more than a permit for a full sized detached house in Maple Ridge), a covenant goes on title that the lot can’t be severed, making it a multiunit rental property indefinitely, size restrictions make the laneway houses QUITE small, yet builders, who I guess have better things to do, quote outrageously high per-square-foot construction charges. I’ve read that $350-450k all-in isn’t unusual. Factor in that the main house now has that much less yard or parking, and building these things seems pretty nutty. Not that Toronto would need to replicate all these mistakes, but…

Here in Toronto, we don’t have laneways, we have alleys. Graffiti’d, urine soaked alleys lined with tumbledown garages and strewn with windblown garbage. Once a critical mass of housing was built on any given block, I suppose it would gentrify somewhat. But who’d want to move into the first one or two built? What’s the opposite of ‘curb appeal?’

And there will likely be a NIMBY effect — literally! For every progressive on the block who wants to build one to make some cash or help with the mortgage, there’s likely four who don’t want any extra density, or any more windows overlooking their back yards. And a tree blocking the site that’s too big to be cut down…

Maybe I’m being too pessimistic.

Kyle

at 12:56 pm

In Toronto, the current ideas and guiding principals that are being explored seem to be leaning toward:

– Lots not being severable, the laneway house would simply be an accessory building and remain on the same lot and title as the main house and it would be treated like a secondary suite that could be made available for rental.

– The zoning would be changed to allow laneway houses that conform to the new guidelines to be “built as of right”, meaning no COA, no NIMBYs, no OMB.

– The cost to build will be whatever the market bares. But the first floor is to remain as parking, so given that there isn’t a basement foundation, it is unlikely that the price to build a 1000 sq ft laneway house should exceed the cost of building say a 1000 sq ft addition.

– Size restrictions would mainly be due to height. Some of the ideas under consideration by the city allow for 2 storeys above a garage. So it really depends how wide your lot and how big a garage you want.

And personally i would much prefer to live in something like this – http://emergingto.blogspot.ca/2014/12/why-laneway-houses-are-so-perfect-for.html than many a condo or townhouse.

Julia

at 3:43 pm

I tend to agree with Ralph – its a bit of a can of worms… My house does not have an alley but I do have a shared driveway with my neighbour and I would hate it if they decided to build an income property on their side …

jeff316

at 2:35 pm

I hate to admit to coming down on the side of NIMBYs but laneway housing? As a home “owner” with a lane, well, ugh.

Kyle

at 2:59 pm

I get what you guys are saying and have the same concerns, but as our City continues to grow and densify, i don’t think the choice is going to come down to whether to intensify or not, the choice will be more like do you want multi storey apartments on your street, or would you prefer secondary suites like laneway houses. My view is that at least with the laneway houses i could benefit (if i chose to build one) from the increased density whereas with the multi-storey apartment, there is absolutely nothing but downside for me.

jeff316

at 10:00 am

I think the likelihood of multi-storey apartments on most residential streets is pretty low. I’d probably still choose the apartments, although you’re right that won’t benefit me financially.

Daniel

at 1:17 pm

David, what is more likely: a 15% increase in average home price, or a 0% increase? Thx

SaraL

at 2:01 pm

Well that’s two extremes.

Maybe a 3% versus 10% conversation would be more realistic, ie. will the market see a drop off based on last year’s mortgage policy changes and the huge run-up in price, or will the market see another large gain, but one that seems modest compared to 2016.

Kramer

at 2:43 pm

I know you didn’t ask me, but for what it’s worth, my opinion is a 0% increase is more likely than a 15% increase. I base that on seeing more houses sitting for longer at this price level… the houses that are priced near what they are actually worth. Houses priced for Wars draw more hungry buyers and they sell faster… but I have seen more houses sitting I find. Maybe my observation is not representative of the truth.

That being said, I would say a 5% increase is WAY more likely than a 0% increase.

Geoff

at 9:40 pm

I agree with Kramer (Cosmo!). In my neighbourhood, between December 25 – Jan 1st, there were like, no sales man. Not one.

David Fleming

at 10:26 am

@ Daniel

Tough question. I suppose that was the point.

Call me biased, but I would say a 15% increase is more likely, only because a 0% increase is less likely.

Both are incredibly unlikely.

But a 0% increase is more unlikely. It’s impossible.

The market increasing, is a probability, and thus how much it increases is the discussion, and we could all agree that 5%, 7%, or 8% is totally realistic. So I feel the 15% is more likely than the 0%.

Jonathan Mandel

at 4:40 pm

Your calculation for the year over year 2015-2016 calculation is flawed. You did (November 2016 / full year 2015)

Mr. Late

at 5:54 pm

Happy New Year everyone …. I am surprising myself in saying this, but I agree that house prices may actually rise even after last years 26% increase, and despite multiple warnings that we are in a bubble. Having said that, I still think a correction will inevitably take place and buyers today are taking a substantial risk of ending up under water in the future.

Scott Ingram (Realtor)

at 12:02 am

In the 37 year chart, are you using the average price for all transactions over 12 months? I’ve been looking at the last 20 years recently, and using the average prices for December, both 2008 (-11.7% in the meltdown year) and 2000 (-0.5% just before the tech bubble burst) were negative year-over-year. Still 18 out of 20 years positive is a pretty strong sustained run.