I really don’t want to get political here, but how can I not?

How can you not?

How can anybody not?

As I’ve said before on this blog so many times, politics is in everything we do. Sometimes it’s invisible, but it’s there. It’s everywhere.

There is a federal election looming in a few months, and the parties are starting to get their houses in order.

Did you see the Liberal attack ads during the Raptors game? Er, not the Liberals themselves, but rather an even more liberal think tank called “Engage Canada.”

So without taking the bait that I’ve essentially set out for myself, let me just say that my point is simply we are going to see more and more of this, by all parties. The ads during the Raptors game were just really obvious, whereas a lot of other politicking isn’t as noticeable.

This week, the federal government provided some clarity on the first-time home buyers’ plan that was announced back in March. Recall that we were talking here on TRB about “shared equity mortgages,” and how the government could opt to offer something similar to strapped first-time home buyers. Also recall that their announcement was somewhat lacking in the “details” department. Well, that changed on Monday.

The key points:

- The program will launch in September, which according to the Gregorian calendar is before the federal election. This is something I find very, very interesting.

- The amount the federal government will loan to buyers is 10%, as stated in March.

- Household income must be less than $120,000.

- The total amount of the mortgage plus the CMHC’s contribution must not be greater than $480,000.

- The maximum purchase price is $565,000.

- The loan is interest-free.

- The government would be entitled to share in the up-side and down-side of the potential change in property value, meaning they would, in fact, take a portion of the profits in the event of a sale.

- The government has set aside another $100 Million to fund organizations already offering similar programs.

- The government estimates 100,000 buyers could be helped by the program.

So those are the nuts and bolts of the announcement, and the reaction has been mixed, to say the least.

First, let’s look at a few choice quotes from government officials, shall we?

Jean-Yves Duclos, the Liberal MP and cabinet member in charge of the CMHC said:

“This will mean more money in the pockets of Canadians and will help up to an estimated 100,000 families across Canada.”

I’m sorry, but this reeks of political rhetoric.

“More money in the pockets of Canadians” is hollow, cliché, and without any actual substance. This is a sound-bite, plain and simple. You can take any government initiative and say that it will “put money in the pockets of Canadians,” but in the case where the tax-payers are on the hook, and where these “savings” are actually just deferred payments, I put zero stock in this quote.

I also don’t like how the 100,000 beneficiaries of the program are “families,” in as much as every single goddam politician on the planet panders to “families.” I would say that 100,000 buyers could benefit from this program (although there are mortgage professionals who don’t believe any will – more on that later), and some might be families. But this too is a pet peeve of mine, and all parties do it.

Mr. Duclos was also active on social media. Here’s a great photo-op that actually shows it was a photo-op, since there’s another photographer in the bottom left-hand corner of the picture:

“…by lowering their monthly mortgage payments,” his quote says.

And yet nothing of the notion that this is simply deferring payment of the loan itself, which we will come back to in a bit.

Another quote from Mr. Duclos:

“Even here in Mississauga and Toronto, first-time homebuyers will have many starter home options. The savings will be significant.”

Um, I’m going to call BS on this quote.

I understand from two awful years of watching Donald Trump that you can just say anything you want, truthful or not, and there aren’t really any repercussions anymore. But for Mr. Duclos to suggest that there are “many starter home options” in Toronto is foolish.

With the maximum purchase price at $565,000, what does that really get you?

A townhouse in Ajax, perhaps. See! Ajax is in Toronto! The Greater Toronto Area, silly blog-writer!

Well, maybe Mr. Duclos is right on that one.

But how about this quote:

“If you facilitate the purchase of new homes by young, middle-class Canadians then apartments will be in lower demand and that means the price of rental will also be kept more affordable.”

Make an argument, if you want. Many of you do this for fun every Monday, Wednesday, and Friday.

But this isn’t exactly a Nobel-winning economist speaking. This is a politician simply saying stuff and things that very few people will take the time to read, let alone analyze, let alone call into question.

But my absolute favourite quote from Mr. Duclos, without question, is this one in which he defended the mortgage stress test:

“We need to have a housing market that protects against the risk of downturns,” he said. “If that were to occur it would be disastrous to every Canadian, to every community and to businesses across Canada.”

Oh God, please just shoot me with a shiny, silver bullet.

So on the same day that the federal government announces that they’re jumping into bed with first-time home-buyers who are reaching for the bottom rung of the housing ladder, they are talking about “protecting against the risk of downturns” with respect to the mortgage stress test.

Again, defend away if you’d like. Tell me how this is so different.

But what I see here is nothing but vote-buying, and I’m not alone on this.

But before I get to that, one more quote….

Interestingly enough, the Canadian Real Estate Association, apparently, supports the idea.

I mean, I don’t. And I’m part of CREA. Most of my colleagues don’t, and they’re part of CREA. But as we know from years of following stories about the Toronto Real Estate Board, these organizations don’t really listen to their members, but rather just rely on the thoughts and opinions of a few demigods.

Michael Bourque, CEO of the Canadian Real Estate Association, dug really deep and provided this piece of insight:

“We think it will help and we think that it’s a good initiative because it’s going to help people get into a home where otherwise they wouldn’t be able to.”

No sh!t, Michael?

Tell us something else that’s completely useless and without any substance!

His comment is only one meagre step up from: “It’s really good, because good stuff is great, and helping is nice, and nice is good, and if you can’t afford a house but then you can afford it, then you can buy it, unlike before.”

The response from most people outside of politics has been negative, which is to be expected. As is the response from your average Canadian tax-payer.

The first comment I saw on the CBC.ca article posted Monday:

Make no mistake, this 10% gift from the government isn’t coming from nowhere. It’s coming from tax-payers.

And that’s one of the things that I believe most of the uninformed, naive, and/or willfully ignorant members of society don’t understand about the concept of government. Those who cheer every announcement for “free” benefits in the midst of an election campaign act as though “the government” is God, rather than an extension of the people, and that the government simply prints more money, when in fact, they take more money from, and on behalf of, the people they are making promises to.

I feel bad for anybody over 50-years-old who is in their “forever home,” has paid taxes for 30 years, and now has to continue to pay taxes and watch as the government panders to voters in an election year by putting even more strain on the CMHC, which most onlookers would argue are already well past their expiry date. The goal of the CMHC when it was created in the 1940’s was never this.

Those in the mortgage and finance industries are also slamming the government’s new housing plan.

How about a quote from James Laird, president of Toronto-based mortgage brokerage firm CanWise Financial?

“The only logical conclusion is that this program was designed to not be used, which is logical if their goal was to be able to tell the public they are taking some steps to help first-time home buyers, but they really were concerned about pouring any fuel on the housing market.”

Mr. Laird provided even more insight in the CBC.ca article which you can read HERE.

Let me take a sample from the article which contains his insights but the first paragraph is paraphrased, and the second is quoted:

James Laird, president of mortgage brokerage Canwise Financial, said the government program could actually reduce a would-be buyer’s purchasing power in some cases. Eligibility is capped, where the amount being borrowed must be no more than four times the person’s annual income, but standard mortgage stress test rules allow for borrowers to get between 4.5 and 4.7 times their income.

“Those who would be attracted to the program would be Canadians who are trying to purchase at their maximum qualification,” Laird said. “However, because the program diminishes how much you can qualify for, it doesn’t serve the needs of the group it is targeted at. Canadians can get a larger loan by not participating in the program.”

Oh, how ironic!

More “unintended consequences;” a phenomenon the government should be quite familiar with by now, since every policy enacted since 2017 (both provincial and federal) has backfired in one way or another.

My favourite quote is from Rob McLister, founder of www.ratespy.com. Mr. McLister is reguarly-quoted, and doesn’t hold back – which you know I like!

“Basically the government is building a bridge to nowhere for first-time buyers. I don’t think anyone needs it and very few will want it. To me, this is vote candy. … Basically they are doing a little but trying to appear like they are doing a lot.”

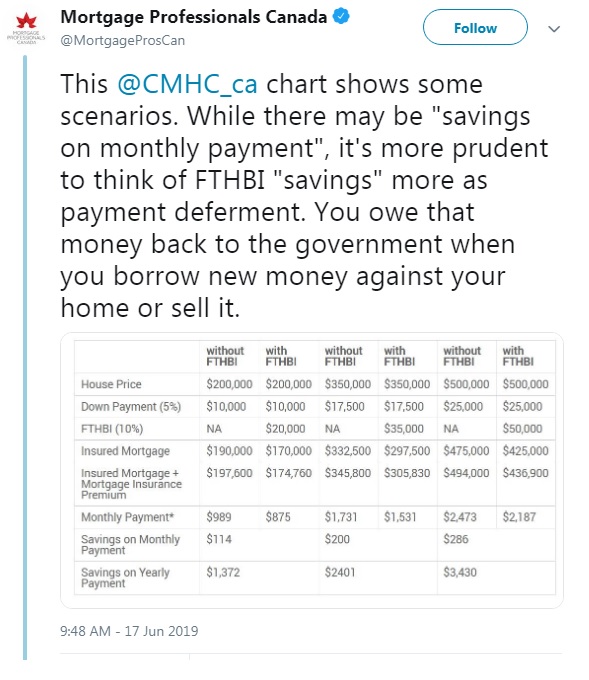

Mortgage Professionals Canada provided us with this Tweet on Tuesday:

But again, are people really listening?

I mean, all that closely.

I have no doubt that voters are hearing “savings” with respect to mortgages, and they’re eating up the idea that the government is going to help them buy a home, but are they listening to what comes after “savings,” ie., that it’s about saving on your monthly payment?

I don’t know that they are!

In fact, I think many people are oblivious to the fact that this loan has to be paid back, and that a percentage of profits has to be as well.

In case it wasn’t obvious by now, I don’t like the government’s plan, and I’m not saying this as a real estate agent who might actually benefit from more Canadians buying homes, but rather as a tax-payer, and a voter.

But it’s election season!

So get used to more promises – from every party out there…

Anthony

at 10:01 am

I agree with James Laird and Robert McLister that few will use this program. My question is: will the government publish stats on how many Canadians are using it? How far off of their 100,000 person estimate within three years will reality be? Hmm!

Another David

at 10:04 am

When you sell your house, how do they assess their shared gain or loss? Is it based on the selling price or appraisal value?

If say economy turns and I am underwater and sold at a loss. I mean a big loss, like buying a home priced at 500,000 and selling for 250,000 while remaining mortgage is like say 300,000. Does that mean I don’t have to pay back the government?

Carl

at 11:58 am

@AnotherDavid There is no shared gain or loss. It’s simply an interest-free loan. Just like a mortgage, but with zero interest. You owe what you owe. When you sell, the gain or loss is yours.

M

at 12:30 pm

It’s a shared equity loan, at 0%. The government is in on the potential gains and losses. Would almost defiantly have to be based on multiple appraisals, at the homeowners expense. The main question that begets is why renovate your kitchen, etc.. when the government puts nothing in but gets 10% of any increase in value back?

Chris

at 12:31 pm

From the CBC article:

“But the government says in exchange for its stake, the CMHC would get to participate “in the upside and downside of the change in the property value” — which means they would be entitled to any corresponding increase in the value of a home when the buyer eventually sells. On the flip side, the government would also on the hook for any share of the loss if the property depreciates.

On a home costing $500,000, if the borrower puts up $25,000 and the CMHC puts up the same amount, the CMHC would then own five per cent of that home. So if, down the line, the house appreciates to $600,000 and the borrower wants to sell, they would have to give the CMHC five per cent of the sale price — $30,000 in this example — not the $25,000 the CMHC put down in the first place.”

Carl

at 12:48 pm

Sorry, I was wrong. I see the CMHC really does plan to operate it as shared equity, not a simple loan.

M

at 12:21 pm

“Make no mistake, this 10% gift from the government isn’t coming from nowhere. It’s coming from tax-payers.

And that’s one of the things that I believe most of the uninformed, naive, and/or willfully ignorant members of society don’t understand about the concept of government.”

Serious question, does it come from taxpayers? Or does the government decide it needs $100m and get the BoC to create that money into existence?

That aside, from what I’ve read this policy appears to have had little thought out into it, and most industry experts think it will have little to no effect on the GTA market. Pure politricking no doubt, but better than a policy with negative consequences.

Carl

at 12:40 pm

Yes, it is a typical election year announcement, accompanied by misleading rhetoric. Apart of that, I don’t understand objections from real estate professionals. If, as some say, it will not be used, why worry?

And if it is used, the hit to the government finances (a.k.a. the proverbial “tax-payer”) will be minimal. The federal goverment will simply borrow money at low interest (currently around 1.5%) and lend it to a certain class of home buyers at zero interest. That means more money going into real estate, and prices going up. RE bulls should be happy.

Carl

at 1:04 pm

And the government shares in the equity. If, as most of us expect, the RE prices continue to increase at a rate higher than the interest on Gov of Canada bonds, the net for the government finances will be a gain, not a loss to be covered by “tax-payers”.

Not Harold

at 3:02 pm

We all benefit from good and honest policy.

But that’s frequently bad politics.

Harper’s tax credits for child sports were great politics, horrible policy, but honest. Harper’s tax credits for transit were good politics, policy, and honest.

Trudeau’s mortgage announcement is GREAT politics, horrible policy, and dishonest. The quality of the policy improves as the honesty decreases and the more it is an exercise of calculated cynicism.

The problem with the Trudeau Liberals is that even the “pros” running the joint – Gerry Butts and Katie Telford before Gerry got turfed – aren’t very good at policy. They’re damn good at comms, at least as a campaigning exercise, and malevolently cynical in that field. Both competed in debate at an international level, which breeds excellence and cynicism in comms. But they’re not really serious about policy like the people tha Chretien and Martin surrounded themselves with. Gerry is a granola munching hippy and he was replaced as head of WWF Canada by David Miller, which shows the lack of seriousness of that role.

So we can’t give them credit for designing a program that no one can use as a cure for the understood negative policy implications. We should instead see that it was cynically intended to have less impact than the campaign would claim but that they’re dumb and inept enough to accidentally make it completely unusable so that they won’t have any actual photogenic beneficiaries.

Much like declaring a climate emergency <24 hours before approving a brand new transcontinental pipeline.

Izzy Bedibida

at 2:33 pm

I would go for it if I had my current GTA salary and lived in Halifax or equivalent city. Lots available in the covered price range, and I would have extra spending money in my pocket.

But living in the GTA, Vancouver, or Montreal, this program is worthless and will not help anyone as intended.

Not Harold

at 3:04 pm

You can’t rent your own apartment in the GTA without going over their income limits!!!

Kyle

at 10:27 pm

@Izzy

I didn’t say you had to use it for your Principal residence. You could rent in the City, and use this loan to buy a cottage, which you rent out when you’re not using, such that it basically pays for itself. 25 years later the cottage mortgage will be paid off, and you’ll have to pay back the loan based on whatever the equity is at the time, but it should be easy enough to get a HELOC on the value of your cottage to pay off the 5%, which again any cottage rent you receive will quickly be able to extinguish. Once the HELOC is paid off, you basically have a free cottage that you can enjoy and that continues to pay you cash when you’re not using it.

Kyle

at 10:29 pm

Oops typo, s/b “It didn’t say….” instead of “I didn’t say…”

Jason H

at 7:37 am

I will vote for anyone who abolishes the CMHC, period.

Susan

at 10:01 am

Thank you for your marvelous honesty. As a 15 year mortgage professional this program is the biggest bunch of nonsense i have ever come across. Since when is deferring debt payment sound advice?

Maha

at 10:56 am

Hasn’t the non-profit developer “Options for Homes” been using this same method of taking an equity stake while providing a down payment loan for years? It seems to have worked for them, although they also build the actual buildings too (including the earliest condos in the Distillery and buildings in the Junction & Danforth Village). IMO assuming prices rise over the long term and the program doesn’t become overburdened with excessive administrative costs, I can see this being a profitable venture for the Feds . On a more cynical note, it’s also easy to imagine that further down the line when people start selling at those higher prices and only get 90% of their equity, we’ll start hearing some outrage from participants about how the government is “stealing” 10% of their profits.

Kyle

at 5:12 pm

The Options for Homes model makes a lot of sense to me. They’ve been really good at identifying up and coming neighbourhoods and i presume because they own a percentage of the buildings they build, that they don’t skimp on quality. Seems like a win-win for them and the purchasers.

Aayushi Verma

at 12:17 am

Thanks for sharing the blog with us. I want to know more about the latest properties in Bhopal at affordable prices.