You can make numbers say anything you want, right?

Except in my mind, when I publish this monthly feature on TRB, I’m unbiased, and simply translating the data that’s put in print by the Toronto Real Estate Board, while mixing in my two cents based on market experiences.

In some of my readers’ minds, I was anything but unbiased last month when we looked at the number of sales in September.

I read the comments, and they were all fair, and all well-taken, but I still believed it to be a comparative analysis of sales data stacked up against previous years, and previous points in the real estate calendar.

So with disclaimer outlined, let’s take a look at this last month’s data.

Keep in mind, as we get started here, that the part of this blog feature is that the readers always have a chance to offer their say. Whether it’s interpretation of data, opinion, or predictions, it’s all value-add. Please, don’t ever hold back.

The first thing I always look at when the TREB data is published, quite simply, is the average sale price.

And since I really didn’t find the sales and/or listings figures to be all that interesting this month, I want to dedicate this entire blog to price.

This past month, average sale price increased a modest 1.3%, month-over-month, from $796,786 in September to $807,340 in October. But more important, in my mind, was the return to that $800,000 threshold that we saw in April, May, and June, of $804,584, $805,320, and $807,781 respectively.

For some of the readers, this is the very definition of “much ado about nothing.”

I mean, here I am, salivating over the return to a completely arbitrary $800,000 threshold, when the elephant in the room is that this absolutely pales in comparison to the “peak” average sale price of $920,791 achieved in April of 2017.

That’s a 14.1% decline, year-over-year.

And all of a sudden, the $800,000 threshold means absolutely nothing!

That’s a fair argument, but it’s an argument nonetheless.

At the risk of sounding unbiased here yet again, I feel the average Toronto sale price has to be taken into context.

Case in point: is your Leslieville, Leaside, Roncesvalles, Junction, or Beaches home worth 14.% less today than it was last April?

Is your downtown Toronto condo worth 14.1% less today than it was last April?

Didn’t think so.

Looking specifically at the Toronto (416) data, the average sale price in September was $869,870, and the average at the peak of April 2017 was $943,947. That’s still an 8.5% decline, but certainly not the 14.1% that we’re seeing across the whole of the GTA.

Having said all this, do all homeowners out there in the 416 believe that their homes are worth 8.5% less today than in April of last year?

Do all the non-home-owner (cynics read: market bears) assuredly believe that a Davisville semi-detached, or a Lawrence Park red-brick Georgian, is down 8.5%? How about a downtown loft?

The data says one thing, but the voices in the audience might say another.

I would suggest that the houses and condos that make up that on-paper 8.5% drop in average sale price, from this past October over April of 2017, represent a series of increases and decreases, across the board.

Case in point, I took a listing in the spring that I did not feel confident about in the slightest. It was north of Sheppard; a large, detached home, in a very, very weak market, littered with listings. We received one offer on the property, in two months, and it was for 79% of the list price – an offer price I have n-e-v-e-r seen in 14 years in this business.

On the same day that I received that offer, I had seven offers on downtown Toronto condo listing.

In case you’re wondering, the house didn’t sell. It’s off the market, and the sellers may try their “luck” again next year.

So how then do we arrive at this 8.5% decline in the average sale price of a 416 property?

As I said, it’s a combination of increases and decreases, with the latter trumping the former.

The 416 is made up of Central, East, and West TREB districts.

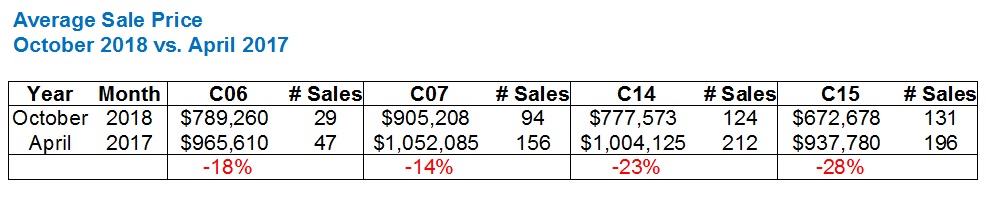

North of Highway 401 lays C06, C07, C14, and C15, and it’s my contention that nowhere in the 416 has there been a bigger drop than in these areas.

So let’s compare the October sales data in each of these TREB districts to April of 2017:

Like I said – these areas have been hit hard.

Now keep in mind, that averages are far from exact. There could be more/less condos than houses, more/less low-end homes than high-end homes, and the data we have – 29 paltry sales in October in C06, doesn’t make for a very good data set!

So let’s add the September sales data to come up with an average for September/October in attempts to smooth out any outliers, but also to gain more data. And just to be fair, we’ll do the same with 2017 – combine March/April.

It’s also worth noting here, that to combine March/April, rather than April/May, will provide for a better look at the “peak.” The average sale price in March of 2017 was $916,567, which is almost identical to the aforementioned $920,791 price in April. May, for what it’s worth, came in at $863,910.

Here’s how the new data set looks:

Two of the four districts look worse, and two look better.

And save for the massive swing in C06, the numbers are all within a few percentage points.

This is, in my opinion, where, why, and how the average home price in the 416 is being dragged down.

It’s merely one area I’ve chosen to look at. We could check out W05 and W10, and I’m sure we’d see the same trend.

But my theory wouldn’t be complete unless we took a look at some of the areas that I don’t feel are well-represented by that 8.5% drop in average home price in the 416.

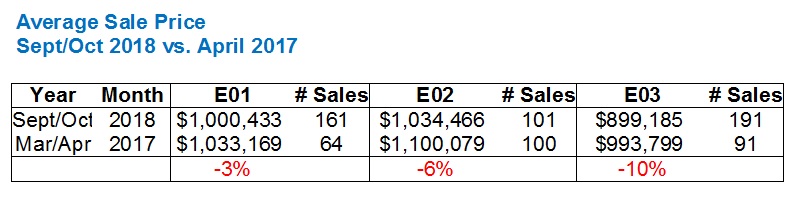

So let’s run the same numbers for the “east side,” ie. E01, E02, E03.

To be honest, I’m actually quite surprised by this.

I figured all three numbers would be between -2% and -6%.

The trend is going to be down no matter what. There are more condos being sold this year than last year (ie. no new houses are ever built, only new condos) and that will always be represented in the data, and the mania of the peak last year has also been cleansed.

But that 10% figure in E03 is shocking to me.

I sold five houses to buyers in E03 between January and April of last year, and not a single one of those houses, in my opinion, would sell for 10% less today, than in March or April of 2017. A few points, sure, that’s the market. But in my opinion, a buyer of a $1,000,000, 3-bedroom semi in March of 2017 would not sell that same home for $900,000 today.

In any event, the 3% and 6% declines, respectively, in E01 and E02 might be more accurate representations of the market.

So where does the average actually get pulled up, you ask?

Condos.

Plain and simple.

Let’s take a deeper look at condo sales and average sale price in the 416, and go back to January of 2017. We’ll look at both the month-over-month increases, as well as year-over-year:

This might come as a surprise to many of you, but condos are up, across the board.

If we did the same thing with these numbers, as we did above, and looked at the March/April average ($564,290), and compared it to the September/October average ($609,368), we’d see that the average condo sale price is actually up 8.0%.

Who could have ever predicted that last year, or the year before?

Now what are the differences between the overall 416 market, and that of the downtown core?

I’m so glad you asked!

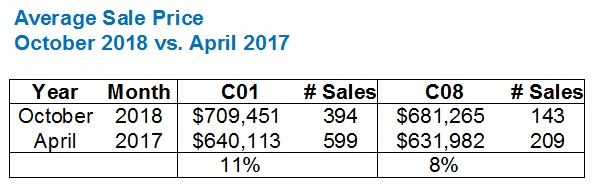

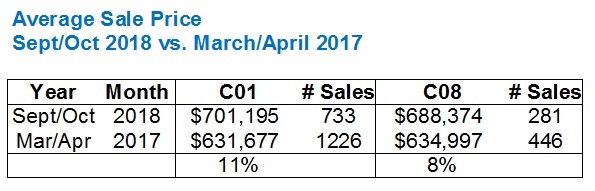

Let’s run the same two charts for C01/C08 condos as we did for the Central and East areas above.

Here’s a simple October-vs-April snapshot:

And just in case we’re concerned about the data size (note that the sales figures are way higher anyways), or the fact that we’re only looking at one month, here’s the second chart:

Only this time, nothing changes!

Still an 11% increase for C01, and an 8% increase for C08.

Those 11% and 8% figures for C01 and C08 respectively don’t exactly blow away the 8.0% average for the whole of 416. Average them out, and we’re talking a 9.5% increase, which compared to an 8.0% increase for the 416, is a modest improvement at best.

I think this speaks to the run-up in condo prices throughout the whole city.

And that speaks to the future of Toronto, where people will live, how condominiums will become the norm, et al. But that is certainly a topic for another day…

Not Harold

at 11:05 am

Lawrence Park red brick georgian? There aren’t many of those left!

All of mid-town from Bloor to the 401, DVP to Bathurst, looks to be seeing a market halt over $2MM.

Lots of spec houses not getting what the spreadsheets called for (it would help if your $5.6MM ask had some landscaping besides some badly lain sod) and people who lived in their house are not getting what they thought they could. Seems like sellers are looking for ~15% above 2017 when the market is 10-20% below 2017. There’s an absurd amount of product above $4MM and above $8MM but not many people who HAVE to do a transaction, so the market can stay uncleared for a long, long time.

Normalish consumers still seem active, but it really helps when you’re able to take a massive chunk of equity from your old house or condo and be close on the monthly payment. That $4MM++ purchase is just much harder to get your head around in market of questionable direction, especially if your kids are already in the right school.

Jack Fanters

at 3:32 pm

Haven’t gandered at this stuff in a while but it looks like Toronto houses finally hit that debt wall and have been sliding down like a wet lougie ever since. I suppose only marginal properties are still seeing gains where people can still pile on some additional debt. I wouldn’t hold out for any meaningful gains for another generation. I will wait until people are disgusted again with the whole idea of buying a rental property and/or urban living and then make my move. Not sure if I will live long enough though at my age.

Derek

at 3:43 pm

I am struggling to identify the takeaway from this analysis today? In conclusion….?

Chris

at 4:09 pm

Agreed. Condos up, houses down seems to be the conclusion of the analysis, but that’s been the case for awhile now.

http://creastats.crea.ca/natl/images/natl_chartC013_xhi-res_en.png

Also, not sure I agree with the assertion that the run-up in condo prices speaks to the future of Toronto. Rather, I suspect it speaks to tightening credit, tougher regulations, and the unaffordability of other home types, all of which are driving buyers to the lower segments of the market (read: condos).

Condodweller

at 10:13 am

@Derek I don’t blame you. See my post below…

@Chris I am going to stick with my prediction that condo prices are going to increase to just below the price of SFHs. If SFH prices continue their recent trend down it will put pressure on condo prices. The only way condo prices might go higher than SFS if condos become more desirable than SFHs, shock and horror. But surely that’s never going to happen, right?

Ed

at 6:58 pm

David the area I continue to watch is in W08, from Kipling to Etobicoke border and from Dundas to Rathburn. In my opinion prices are easily off peak peak by 15- 20 %.

From May 2017 (not peak) to now I am seeing prices down by almost 10 %, so the 8.5 % would be accurate for this area (in my view).

Carl

at 11:12 am

For the big picture, the Teranet/National Bank house price index for October is out today:

https://housepriceindex.ca/

Condodweller

at 10:05 am

David, here is why you come across as biased from my point of view even though you state the opposite….

“And since I really didn’t find the sales and/or listings figures to be all that interesting this month, I want to dedicate this entire blog to price.”

When a perma-bull re agent says something is not interesting and wants to ignore it tells me that’s the place to look for nuanced detail. This is akin to a magician telling you to look at his hand that is doing the misdirection while the other is making things happen.

“Having said all this, do all homeowners out there in the 416 believe that their homes are worth 8.5% less today than in April of last year?”

David, on the house that you received 79% of offer how much were you underpricing it to begin with if any? What percentage of the actual value was the offer? 60-70%? I think you are contradicting yourself when in once sentence you question if a house is really worth 8.5% less and the next you say you can’t sell a house for 20% less. You also accurately point out that the 8.5% is affected by condo date however fail to point out in which dirrection which may not be obvious to the average observer. If the average is being pulled up by condo sales that suggests to me that the average house price would be lower than 8.5%. You have conveniently neglected to isolate the house prices vs condo prices which you have readily done in the past to demonstrate and argue for higher prices. How are prices for SFHs holding up in your area of specialty downtown?

“Who could have ever predicted that last year, or the year before?” I’m not the one to say I told you so but since you asked I will raise my hand.

Now that you are shocked by the lower average prices and there are no last bastion of SFH bucking the trend ( I will assume the omission of downtown SFH analysis is because those are down as well) when will you come to the conclusion that we have turned the corner and prices are heading down?

Credit where credit is due: it’s good to see that you are using the April 2017 highs for comparison and showing that the trend is down. I think if April 2019 average prices are down next spring the trend will be clear with two normal high water mark data points below the April 2017 high. But what do I know, I’m not in RE I just like to follow the market and do some analysis along the way.

gattu

at 11:06 pm

Well-said, Condodweller. This piece had a much higher proportion of cherry-picking than usual.

Also, when analyzing the health of any industry or business, both price and quantity matter. If Apple suddenly sold a lot fewer iPhones, it’s stock price will get hammered, even if the price of an iPhone remained unchanged.