Perhaps I got a wee bit carried away with my first two predictions on Monday, but they were the most important points.

Today, I’ll go through five more points, also in not-so-brief form, and give you my two cents on a number of issues I think will be big in 2018.

With no new listings to speak of through the first few days in 2018, our time is better-spent speculating on things we can’t control, am I right?

3) The “stress-test” will have a short-term effect, but no medium-term effect.

God, what you all must think!

I make my living selling real estate, and I’m so damn positive, all the time. I know how it looks, and if I were you, I’d be cynical; probably more than you are right now.

But I write what I think, and I predict what I believe to be evident.

And while I think the new “stress-test” will have an effect, I don’t think it’s going to be nearly the effect that some people are predicting, nor do I think the “effect” will last longer than three months.

Three months? That’s it? Yes. And let me tell you why.

Can we agree that people still need to live somewhere? Yes.

Can we agree that the market speculators, and investors, have deep enough pockets to avoid being affected by the new rules? I don’t see why not.

So people will still transact in real estate.

The way I see it, there are only two questions that need to be asked of the new rules:

i) How many people will not purchase real estate at all this year, as a result of the new rules?

ii) How many people will buy for a lower amount than they would have in 2017?

We’ll address question #1 first.

We’ve seen “estimates” on how many people will be affected by the new mortgage rules, from a slew of pundits. I’ve seen anywhere from 5% to 20% of “all insured mortgage buyers.”

But as I asked above in question #1, how many people will not purchase at all, as a result?

I can’t answer that question for you, and if I were to hazard a guess, I’d say I’d be doing no better, or worse, than every other pundit online and in newspapers.

Consider that the new mortgage rules only apply to those with more than a 20% down payment.

Robert McLister wrote in his blog (dated, but the only stats I could find) that 63% of first-time buyers have less than a 20% down payment. And I would think that number has increased substantially in the past year or two.

So assuming that 70-75% of first-time buyers have less than a 20% down payment, then how many buyers are really affected by the new mortgage rules?

As a result, how many buyers will not purchase as a result?

Not a whole lot, in my opinion.

I currently have twelve buyer-clients on the roster, and not one of them has told me they don’t intend to purchase as a result of the changes.

In fact, not one of them have changed their criteria, which leads me to point #2.

How many people will buy for a lower amount than they would have in 2017?

A good number, I would think.

While I believe that very few buyers at all will shelve their purchase plans, I do believe that buyers will have to settle for less.

How many?

Perhaps 5%. Perhaps 10%. Again, these are educated guesses.

So then what happens to the market? Is there a true “trickle-down” effect? Will we see lower prices as a result?

I don’t think enough buyers will be affected to have that trickle-down that market bears are hoping for, and would-be buyers desire.

Consider two points:

i) Most of my buyers do not purchase to the maximum of their pre-approval.

I always ask my clients a series of questions regarding financing when we start the search

“What’s your approximate acquisition cost target?”

“Have you been pre-approved for a mortgage?”

“How much was the pre-approval?”

More often than not, the first and third questions are answered together, with something like, “We’re looking to spend about $1.2 Million. The bank approved us for $1.6 Million, but that’s crazy!”

Then often they add something like, “How do they think we can afford that?”

Well, perhaps you are a bit more conservative with your personal finances than the banks are with lending. But banks are in business to lend money, and lend, they shall!

So with an overwhelming majority of my clients not spending to their max pre-approval, it means many of them who “will be affected” by the new mortgage rules, really won’t, in the end.

My buyer-clients who usually do spend to their max pre-approval are the ones at the low-end of the totem pole. It’s those buyers who I think will be greatly affected, and those who I think might have to drop out of the race.

But in terms of how this affects pricing, there’s still so much demand for low-end, sub-$400,000 condos in the downtown core, that even losing, say, 10% of the buyer pool, won’t cause prices to go down. They just won’t go up some 20% like last year.

ii) Buyers can take out 30-year amortizations

Let’s not forget that the 30-year amortization is still in play!

For these uninsured mortgages that are now stress-tested, buyers can opt to take a 30-year amortization instead of the standard 25-year.

So for the buyer with 20% down, looking at a $400,000 purchase at 2.99%, the $1,512.74 per month mortgage payment payable with a 25-year amortization can be reduced to $1,344.23 with a 30-year amortization.

And using the “stress-tested” rate of 4.99%, those numbers are $1,859.31 and $1,705.90 respectively.

Yes, you pay more interest as the ratio of principal to interest goes down.

But the entire point here is: buyers want to buy.

I feel terrible for the buyer who saved up 20% down and can no longer buy, who says, “Screw this, I should have bought with 5% down two years ago!”

So while I think that it’s going to take a month or two for the proverbial dust to settle, I think by March, this will be old news, and the market will have moved well past any impacts of the stress-test.

–

4) Banks will change their lending criteria.

What did I say above?

“Banks are in business to lend money, and lend, they shall.”

And what’s that old line I’m thinking of from The Simpsons? Something like, “I didn’t get rich by writing a lot of cheques.”

Folks, the banks want to lend, and they’re going to lend.

There’s no way that the Big-5 banks will sit idly by and watch a chunk of their business fall by the wayside.

It’s not a huge chunk, as I suggested above. How many buyers will fall out of the market? Not a lot. But how many buyers will purchase for less than they would have, could have, should have? That’s a larger number! So add those two numbers together, and you can see what the banks see: they’re lending less money.

And while banks clearly make money nickel-and-diming us for monthly paper-statements, withdrawal fees, overdraft protection, Interac transfer fees, and just about anything else they can think of, their big money comes from lending.

Don’t be surprised to see the banks get creative this year!

I’ve heard that the 35-year amortization is “technically still legal,” although I’m sure there are a slew of ifs, ands, & buts.

We’re now in the safest lending space that banks have ever been in, so perhaps they bring back the stated income programs for self-employed individuals, non-permanent residents, et al.

Perhaps a higher loan-to-value is coming for refinancing.

Who knows, get creative!

But there’s just absolutely no way the banks will cave and accept lower revenues in 2018 and moving forward. They’re smarter than the Federal government, and dare I say they have more clout too.

–

5) The spring market will provide the reverse chronology of 2017.

This is what I call a “slam dunk.”

As I’ve written before many times, the market typically starts a new year slowly, and builds momentum.

January is cold, dark, and miserable, and while many buyers choose this time to start their searches, many need to learn, educate themselves, see a few properties, and don’t end up buying until February, March, or April.

Having just sat down and tried to find five properties for my weekly “Pick5” video segment, and failed due to lack of new listings (I’ll still have a video out on Thursday afternoon, but it’s an odd one!), I can personally attest to the fact that there are very few new listings on the market so far through the first week of January.

A slow January usually leads to a busier February, and then a March that is the first “big” month of the calendar year. The Easter and Passover weekends, along with various Spring Breaks for the public, private, and separate schools, effectively break the spring market into two halves: Jan/Feb/Mar, then Apr/May/June.

By the time Easter, Passover, and Spring Breaks are all over, the weather gets nicer, Daylight Savings Time provides for more light at night in which to view properties, and historically, May and June are the hottest and busiest months of the real estate calendar.

2017, however, did not follow suit.

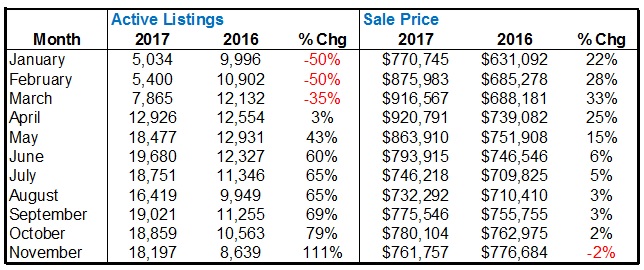

Take a look at this chart of active listings and sale prices; 2017 pitted against 2016 for each month up to November:

We started the year with a dearth of listings, and that trend continued through to the start of April.

As a result, prices skyrocketed.

I wrote in Tuesday’s blog that the “Fair Housing Plan” absolutely killed the market in April, but also note the number of listings, and the incredible increase we saw!

Now this is typical of a spring market. We usually do see far more listings in April, May, and June than we do in January, February, and March.

But after the FHP was announced, buyers cooled off.

Sales dropped, and as you can see on the right-hand side of the graphic, so too did prices.

This year, I expect the exact opposite to transpire.

I see the market starting slowly, and building up toward April and what is typically a very strong market.

–

6) The government is finished meddling in the real estate market.

They just can’t possibly do anything else, can they?

There was an awesome article in the National Post on Tuesday entitled, “Politicians act like they’re ‘solving’ Canada’s housing problems while continually making them worse.”

Folks, it makes me so angry.

I’ll talk more about politics in prediction #7, so I’ll try to curb it here.

But honestly, I don’t understand the Federal Liberals.

They make so many promises, and have so many agendas, and so many of them contradict each other, or can’t co-exist.

Here’s an excerpt from the National Post article:

The Trudeau government’s National Housing Strategy puts the same misplaced faith in bureaucrats to know the “right” type of housing. For example, according to the federal government’s plan, “housing investments should support Canada’s climate change agenda.” That’s why the policy “includes ambitious targets to reduce greenhouse gas emissions” — which is obviously a demand coming from Liberal politicians and not from those Canadians struggling to pay for housing.

So we need to address the “housing crisis,” but we’re gong to ensure that we address yet another difficult objective with respect to climate change in the process?

For the life of me, I just can’t see any more changes coming to the Canadian housing market.

Back in 2008, when the United States experienced their housing crisis, a buyer of Canadian real estate, often with stated income, could obtain 107% financing, and/or via a 40-year amortization.

Times change.

Since 2008, the Canadian government has taken extraordinary measures to ensure that our market does not suffer the same fate. They’ve tightened lending rules, and forced buyers to put up more equity, take on less debt, and pay it off faster. We now have the safest lending space in modern Canadian history.

But with this last round of changes, I think they’ve gone way too far.

The idea itself? “We’d like buyers to be able to afford to pay their mortgage if the rate were to change,” that’s a nice one. But it’s not what buyers want. It’s not what Canadians want. And I don’t believe the government implemented this policy to reign in debt (when they’ve done nothing about unsecured debt like credit cards, lines of credit, etc), but rather to be seen as “doing something about the housing market.”

We’ve already beat that horse to death, so let’s look forward.

In 2018, I don’t foresee a single policy change in the mortgage market from the federal government.

Knock on wood, but there’s simply nothing left that they can do.

–

7) Kathleen Wynne will Wynne another Premiership, and that’s scary for home-owners, and home-buyers.

In March of 2017, Kathleen Wynne’s approval rating reached a low of 12%.

Twelve percent.

Like, out of a hundred, folks!

I’ve been closely following politics since I turned eighteen and gained the right to vote, and I don’t believe I have ever seen a number anywhere close to that!

A 12% approval rating makes Donald Trump look like Jesus/The Beatles at the same time.

When the above article and associated approval rating first came out in March, I remember sending my sister an email saying, “She’ll still win.”

What I received in response, from somebody who reads a hundred newspaper articles a day and knows politics inside and out, was simply, “Yup.”

What more can you say?

Voters just can’t stop themselves. We saw this in 2014.

All the provincial Conservatives needed in order to obtain a landslide victory was continuously shout, “ORNGE scandal! Power plants! McGuinty! Budget!” over and over. But instead, we got this insane promise to cut 100,000 public sector jobs, as though those 100,000 people, and their families, don’t vote.

I don’t expect things to be different this time around.

I’ve never seen a politician who’s implemented more bad policy than Kathleen Wynne, and no, I don’t want to list them here.

But she’s going to win again, because voters are stupid. If Donald Trump can win the Presidency, then Kathleen Wynne can come back from a 12% approval rating.

And what happens when she wins?

It’s more war against the have’s, to provide for the have-not’s.

If you can think of it, she can implement it.

I know I’m letting my political views shape this entire argument, but I just don’t see Kathleen Wynne doing anything to help home-buyers, and she sure as hell isn’t going to do anything to help home-owners.

Higher taxes, more government revenue, more expenditures on more things that nobody really asked for. And as real estate has always been, and remains, the golden goose of the Golden Horseshoe economy, I think it’s the first place the Liberals will look during their next round of making-up-new-taxes to provide them with the revenue they need to keep the engine moving.

–

Phew, so that’s it, folks!

As you probably might have assumed, I had a couple other points in the queue, but I’m sitting here in the office at 10:15pm and even the cleaners have already gone home, so I’m outtie.

Time will tell how these predictions, and these hot-button issues, will play out.

Next week, I want to talk a little more about debt, and while I know we’ve covered the new mortgage rules all week, simply put – I just have a lot more to say…

ed

at 9:18 am

What I forecast is a slow start in the New Year somewhat due to the new stress test for those with 20% down and the notion that many of those who would have been affected ended up buying at the end of 2017.

Come April we will have headlines that prices are down 25-30% from March 2017 to March 2018, not to say that prices will be down from Jan 2018 but they will not compare to last years blockbuster numbers. Having said that many will be afraid to jump in with such negative headlines out there.

I also see a strong possibility of a rate hike in the spring, also a negative for the market.

So my guess is prices will be flat from Jan 2018 until June 2018 and after that? Who knows?

McBloggert

at 9:50 am

I am inclined to agree with your view. I think so much of real estate is market psychology, if people get scared or cautious, they just sit. When people are in a frenzy things get nutty – last spring people were terrified of missing out – being priced out forever…

There is also just a huge run up on all asset classes – which is generally a troubling thing. Stocks, gold, bitcoin – all up massively right now. Then you start seeing even more speculative or dubious assets start getting bubbley – classic cars are skyrocketing, certain new Rolex’s are jumping 20%. It all harkens back to the 80s.

Again I am not a bear – I think prices will likely do a 2%-4% increase – BUT – if NAFTA gets cancelled, our dollar drops 10%, minimum wage results in higher unemployment and our economy stalls. I would be prepared to hold onto what you’ve got because we could see a pretty swift decline….

Ralph Cramdown

at 10:33 am

“Can we agree that the market speculators, and investors, have deep enough pockets to avoid being affected by the new rules?”

You are living in a city full of pretenders. Deep pockets — twice a year, a man in a van comes to your house and changes the snow tires on your luxury vehicle, right in your driveway. Pretender — you drive around all year on all season tires, or worse yet, nearly bald all season tires on your luxury vehicle. I see a lot more of the latter than the former. And I’m not talking about the C Class bourgeoisie.

The real deep-pocketed people don’t spend their time building portfolios of condos and SFH. That’s the domain of people who attend real estate seminars and watch HGTV. Besides, taking out the marginal buyer affects prices regardless of whether other buyers have deeper pockets.

Want to know what I’d like to hear about? Pent-up supply. How many sellers took a look at the fall market and said “let’s wait ’till spring”? 416 detached active listings, December 2016: 488. 2017: 1,467 +201%

McBloggert

at 12:06 pm

Why on earth would anyone with a luxury car use a man in a van to change snow tires? The dealer picks up your car and stores your tires and drops it off…I get the analogy but I think the reason you don’t see much of that is well…that would be a super niche market already covered by a dealer.

Ralph Cramdown

at 1:21 pm

Either/or. Point being much of the high end stuff I see is leased by people who don’t see the value in winter tires at all, and a surprising fraction are driving around on tires bald enough that they were certainly informed of it at their last service, and ignored it. Are these people not as rich as they appear, or just really stupid? It can be hard to discern whether a stranger is rich or just cash flowing. In times of yore, having worn-out shoes (“down at the heel”) was a telltale. These days, I glance at tires.

Condodweller

at 2:32 pm

Ralph I would refer you to the book The Millionaire Next Door to help you spot the wealthy. I like the saying in Texas “All hat, no cattle”

Ralph Cramdown

at 4:30 pm

Millionaires who aren’t flashy are hard to spot, but their fraction of the population is probably relatively constant through time, or at least changes slowly. The proportion of po’ folk who want the bling probably stays somewhat constant, too. But as the credit cycle turns, the number of po’ who can get the bling goes up and down dramatically. David sees what appears to be a lot of deep pockets, but only their bankers know for sure.

McBloggert

at 2:44 pm

Hmmm interesting – I never thought to look at tires! I always look at whether or not a car had a “dealer” license plate cover vs. a used car dealer or none at all.

This has been my go to way to thin slice someone as a pretender rolling around in a 4 year old Range Rover or Mercedes. It isn’t a definitive test – but I doubt you’re going to find too many well off folks buying used Range Rovers at the Yorkdale Auto Barn…

But I am going to start looking at tires now too!

larryK

at 3:27 pm

Why do any of you care how many “deep-pocketed” people (and pretenders to such) there are in your city or town or neighbourhood?

Condodweller

at 1:35 am

@larryK

Because “pretenders” who can’t afford tires for their luxury vehicles likely are the serial refinancers of their home to support their living beyond their means. Once house prices stall and they can’t refinance due to no more equity in their house or due to new rules we may start seeing people forced to sell their homes/defaults which may trigger further price declines if there are enough of them. Couple this with increasing rates which BTW also affect HELOC payments in addition to mortgage payments and we could be in for a quite a ride.

JCM

at 2:28 pm

There are lots of pretenders out there for sure. How many speculators are leveraged to the hilt, and used HELOCs as down-payments to buy more and more new properties? Lots and lots. Leverage is nasty on the way down.

Sophisticated, deep pocketed investors are not touching residential real estate in the GTA.

FreeMoney

at 3:17 pm

“How many speculators are leveraged to the hilt, and used HELOCs as down-payments to buy more and more new properties? Lots and lots.”

Proof, please.

Kyle

at 9:10 am

Pretenders?

What i find pretentious is when people presume to know others’ financial situations, and portfolio holdings based on naive cues and then consider themselves the arbiter of whether someone is deep pocketed enough to meet their bar for being “deep-pocketed”.

First off, David is saying that there will be some with “deep enough pockets to avoid being affected by the new rules”, he’s not saying there are a bunch of deep-pocketed Billionaires waiting to become condo landlords. Two very different contexts.

Second, with the exception of those who inherited or hit the proverbial lottery, every “deep-pocketed” person out there had to build up their wealth, which is done by accumulating appreciating assets or assets that generate income. There is nothing wrong or pretend-y about building up your balance sheet.

McBloggert

at 9:45 am

I think the comment was more in reaction to the suggestion that “Can we agree that the market speculators, and investors, have deep enough pockets to avoid being affected by the new rules?”.

While there may be some hyperbole in Ralph’s comment; I do think the premise is correct that there are a lot of speculators or would-be HGTV developers who are in over their heads. I know Dave can point to a bunch of examples, which he won’t as a professional curtsy, of amateur flippers who currently getting crunched.

On the flip side – I know of a number of people who declared bankruptcy during economic downturns, but built their business and wealth back up. Such is the life of an entrepreneur – it is not without risk.

Kyle

at 10:12 am

Fair enough, real estate, as any other asset class is not without risks. Even in hot markets, people who don’t know what they’re doing can get burned, but that is no different than an amateur day trader with a margin account.

My point is simply people in glass houses should not cast stones. Real estate has enabled a lot of everyday people to build up wealth, far moreso than financial markets have for those that don’t hold any real estate. You can see this whenever they show these graphs of Canadians net worth and breakdown the sources. Or articles like this one: https://www.theglobeandmail.com/news/national/renters-lose-ground-to-homeowners/article4151353/ And those just show the difference from home equity, not even talking about net worth of people who actually invest in real estate.

To me it just seems rather rich (and bitter) for those who don’t hold real estate (and likely under-performed those that do) to be throwing around meme-y disparaging remarks (which quite frankly are wrong) against them. Warren buffet famously drives a five year old entry level Cadillac, and often buys his cars used.

I strongly encourage anyone out there who is gradually building up their balance sheet to ignore the haters and not worry whether you’ve reached someone else’s definition of “deep-pocketed”. Agreed with your earlier point that they should know what they’re doing (this blog is very helpful in that regard) and not bite off more than they can chew.

McBloggert

at 11:18 am

Re: Cars.

My parents never cease to tell me about the times they saw the late Ken Thompson at Lawrence Park Motors getting his Volvo 240 station wagon serviced. They also loved to tell me about seeing him shop at the Sears for a vacuum cleaner.

I do find it grating when people, especially on the internet are cheering for others to fail so they can be right. The internet can be a megaphone for negativity.

Kyle

at 11:49 am

Very well said!

At the end of the day, some people are flashy while others are not, some people are wealthy while others are not, and some hold real estate while others do not. Let’s not conflate these things to make a point.

Andyy

at 10:37 am

Are all your posts going to approach 3,000 words now? Don’t get me wrong I love it! I need a full seven minutes to kill in the bathroom every morning at 10:30am.

Sardonic Lizard

at 1:11 pm

David.

Stop.

Writing.

Every.

Sentence.

On.

A.

New.

Line.

Please.

Remember.

Grammar.

School.

Paragraphs.

Are.

Your.

Friend.

David Fleming

at 6:37 pm

@ Sardonic Lizard

Some aspects of my writing style are borne of necessity, rather than desire.

Mobile users represent over 50% of my readership.

They don’t like large paragraphs.

It’s tough to read.

They like white space.

They like to scroll.

They like to skim.

Large, block paragraphs are too hard to see, too hard to read, and…wait…

….new line…that one was getting too long…

…I also love elipses…

jeff316

at 11:21 am

Exactly. If you wrote properly, no one would read it.

Frances

at 1:11 am

And maybe this is the place to say that you don’t “reign” in something, you “rein” it in. The Queen reigns over England and she reins in her horse (and I gather she still rides – at 91!).

Brandon

at 1:43 pm

Are condos going up?

Condodweller

at 2:23 pm

A big question we need to ask is how many sales have been brought forward by the “if you don’t buy today, you will not be able to afford to buy tomorrow” scare tactic and how many people will actually delay buying once they get the sense that prices have stalled out and they can, in fact, wait and save to buy later.

JCM

at 2:32 pm

And the corollary question — how many listings have been pushed back by rising prices, but will be brought forward when the market prints a 15% year over year decline in March?

Dave

at 2:41 pm

Wynne has done everything she can…create a wedge issue (minimum wage) that effectively cuts out 30% of the voters. Granted, they are the least likely to vote Conservative, but she can now count on those people who want their raise to $15 per hour in the new year. That plus OHIP+ makes her the prime candidate for younger voters, people without healthcare plans (who tend to have the lower-wage jobs). She also has the big unions in her pocket who will flood the media with Anti-Brown ads.

Brown missed his chance to make a stand that the raise was too much, too quickly. By vowing to reduce minimum wage he would have won small-business owners, plus guaranteed people who are in $14 per hour jobs that they wouldn’t leave (because they would be applying to jobs that were <$14…reducing job vacancies).

His battle now is to get the centre-right voters to actually come out and vote for him versus staying at home.

I am shuddering to think of another 4 Wynne-tastic years.

paul

at 3:03 pm

thanks for this informative post. hope may and jun will be a strong one this year

Alexander

at 3:57 pm

I do not see any 2018 substantial price increase for detached GTA segment market at all and possibility of 5-8% increase in prices of GTA condo markets only if there will be no more interest rate increases / bank tightenings in first half of the year and no more government intervention on any scale. Also I do not see share of detached houses going up at all, it will be going down in fact. First 3 months will be dead with headlines screaming 20-30% drop in sales, prices, etc and if no major negative events blow up the market in the first half of the year, in the fall it will start recovering – a little bit though. I think David’s forecast are too optimistic.

Muhammad

at 4:33 pm

Not as Optimistic as David (in the short term) but i do agree that things will improve in the long run. DEMAND & SUPPLY will always prevail. Land prices have way gone up. Detached pre-construction homes are limited in supply & prices are high. Base prices for all types of properties have way gone up even out west in KW, Niagara region.

FLAT MARKET in terms of prices but do not expect a CRASH (as some would-be buyers are hoping)

MARKET PSYCHOLOGY will be Big this year and it will be interesting to see if the activity picks up by May/June.

FEDS may not have much left but i do see them changing the CAPITAL GAINS rate to 100% inclusion (from 50%) to curb local speculation as the data suggests it wasn’t the foreign buyers in detached segment.

Will be interesting to see how condos does this yr. And if they still keep going up – there is no reason why detached would not follow eventually since they will be undervalued.

Joel

at 5:55 pm

I think that the stress test is going to increase the amount of properties on the market. So many people have too much consumer debt and rely on their homes equity to balance them out. When these people no longer qualify we are going to see many of them selling to downsize or rent.

I also believe that the 1-2 million market is going to see a decrease. The lenders have really tightened up on stated income programs (as governments have told them they need to). So many self employed people make great income, but don’t declare it on their taxes which will not allow them to qualify for the mortgage they want. It is going to take years before these people start declaring their incomes high enough to qualify for the homes that they want.

If (when) Wynne wins the election it will show that the laws have had a net positive impact on the general population. The people of Ontario aren’t worried about the ability of a couple in Toronto that makes 200K a year and whether they can get their dream house. Ontarions want to make sure that everyone has a living wage and access to medical care. What the Conservatives need in order to win is empathy for the average person and an understanding that the majority of Canadians will give up some of their money for the benefit of the Canadians that are less fortunate.

Chris

at 12:37 pm

An article today (by BetterDwelling, yes I know Kyle, you’re rolling your eyes), discusses Bank of Canada statistics showing that “More than 40% of mortgage borrowers pushed their personal limits to buy a home”.

This data runs counter to David’s anecdote-backed assertion that the stress test will have a minimal impact because his clients don’t usually buy the maximum they can afford.

https://betterdwelling.com/new-mortgage-distribution-data-from-the-boc-shows-stress-testing-is-a-huge-deal/

Chris

at 12:44 pm

As an aside, the extremely positive jobs report published today has basically guaranteed the Bank of Canada raises rates in March, if not sooner (later this month). Add that to the stress test and the effective qualifying rate has climbed 3% in pretty short order.

Kramer

at 1:17 pm

Classic… an extremely positive jobs report comes out:

– Bears see rates going up – headwinds.

– Bulls see a strong economy – tailwinds.

Not attacking you Chris… just a fantastic example of taking a data point and making it work for whatever one’s perspective is, and why everyone needs to constantly reframe and look at things from perspectives of all stakeholders.

Chris

at 2:32 pm

Oh it definitely has a tailwind aspect to it, in that a stronger economy with more income is good news for real estate.

It just depends on which factor you perceive as the stronger: a robust economy with more jobs or higher interest rates weighing on record levels of household debt.

From my standpoint, the headwind outweighs the tailwind. But that’s just my opinion.

Kramer

at 7:52 pm

In terms of long-term health/strength of the real estate market, a strengthening economy and interest rates in the still historical “low-range” are pretty tasty ingredients. And strong long-term prospects are a tasty ingredient for the short and medium term.

Chris

at 11:25 pm

As I’ve said before, I’m more optimistic on the long term. Short term, less so.

While interest rates are at historically low levels, the rate in the 1980’s is not all that relevant for households with very high levels of debt, watching their interest rates climb by a percentage point or two.

Juan

at 2:05 pm

Just wait until Vancouver implements some new RE curbing policies and Wynne’s options are either to match them, or let all the investor money flow back to Toronto.

larryK

at 3:26 pm

When David (or anyone else) talks about 2018 prices rising or falling by X%, what are they taking as the “base” price: the 2017 average of $822,681 or the December 2017 average of $735,021? This didn’t much matter a year ago (or in most recent years), since the 2016 full-year average price ($729,837) was virtually identical to the December 2016 average price ($730,124). But this time around, we’re talking about an $87,000 difference.

Kramer

at 11:46 pm

2018 could be the year of condo owners trying to cash in on their gains/equity to try to get into the SFH market.

Like every other year before it.

Only this year they are sitting on abnormal 2017 gains.

Might fix this shrinking spread between condos and SFH which makes no sense and has to correct one way (as above) or another (condo values dropping).

lui

at 7:03 am

Kramer I agree.I seen condos in my location go up 30% in value in 2017 and right now there is zero sellers.I hope I’m wrong for the sake of my savings account though.I won’t complain if I see another double digit rise I’m planning to move on from condo living.

Condodweller

at 1:16 pm

I just read a Warren Buffet piece where he referenced a Barton Biggs observation which is a great quote that applies to our re market : “A bull market is like sex. It feels best just before it ends.”

ami

at 5:45 pm

what a country!!! even a place called home is just a business shelter..driving people crazy about the non sense prices and insecurities…

lui

at 6:59 am

Try finding a decent one bedroom condo in Toronto for less than $400,000 that is not listed in City Place near TTC.Selections are few.