Without a doubt, the blogs that take me the longest to write are always the “year-end” or those that start a particular market.

The year-end ones are really tough.

I believe I’ve honed these posts over time, and finally found a theme I can replicate every year. My “Top 5 Stories” and “Top 5 Posts” enable me to cover all the ground that’s needed, since I can look at both the blogs that got attention and/or caused a stir, whether the subject matter was notorious or not, and I can look at the stories themselves which helped to shape the preceding twelve months in the world of Toronto real estate.

But narrowing it down to only five posts, for each category, is tough.

I typically spend 3-4 hours looking through posts, re-reading, trolling comments, and then categorizing anything that I think could be in either list.

“Anything” often represents about 60% of blog posts. And from there, I have to make decisions, cutting posts with the same balance of tough-love and business-savvy that a general manager demonstrates when he tells a sixth-string wide receiver that he’s not on the 53-man roster, and a job at Foot Locker is waiting.

When it comes to my Predictions post, I usually write down my ideas, based on my overall thoughts on the market, stories I think will have legs, and anything statistical in nature that I want to explore. Then I go back to the previous two years’ predictions post, and try to avoid repetition.

But what if I told you that essentially none of my ideas are new?

Sure, there’s some variance. But the meat is the same stuff you’ve chewed on in the past.

Here’s how I think the fall will shake out…

1) Average Home Price Will Rise

I can’t make it any simpler than that, although, this needs a LOT more explanation…

There is so much to talk about when it comes to average home price, and there are so many ways in which one can manipulate the numbers to show the market in a better or worse light.

For me, I just want to know what’s going on in the market.

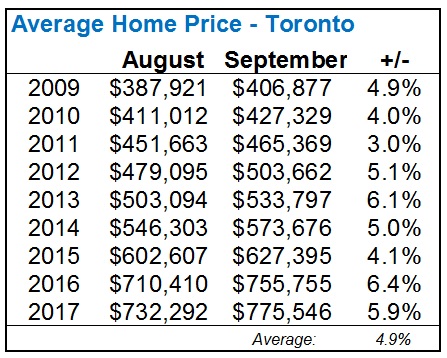

And it starts, at the most basic level, with the average home price in the month of September.

I will provide the first lay-up prediction and tell you that the average home price in Toronto will increase 4-5% from August to September alone.

A lay-up. It truly is.

While that sounds insane, and while a 5% per month jump would represent a 60% annualized return and we know that’s probably not going to happen, we need to wrap our heads around the hot and cold periods of the real estate calendar.

August is slow. No question about it, no arguing, and despite the odd “bidding war in August” story you saw in a newspaper, it’s a very slow month. Buyers are waiting for the “busy fall market, and the sellers are waiting for the buyers. In fact, sellers are taking their houses off the market in August, to put some time in between listings.

And it’s because August is so slow that I feel the average home price, in that month, is actually depressed.

My 4-5% prediction was based on my gut, but having gone back and looked at how the average home price has performed from August to September over the past nine years, it adds evidence to my supposition:

That’s an average of 4.9%, with a low of 3.0% and a high of 6.4%.

Knock out top and bottom, and we’re looking at a 7-year band of 4.0% to 6.1%.

That’s very consistent!

Now the one problem remains: we don’t know what the 2018 August average home price is!

I’m writing this blog on Monday night, and the stats aren’t out yet. I guess TREB has their hands full, I can’t imagine, with what…

In any event, I would imagine that the August, 2018 average home price is slightly below the July price, which was $782,129. So assuming that the price is around $775,000, that means we’re looking at an average price of between $806,000 and $813,750.

Now, some of you might suggest that comparing the September price to August; the comparison of a mighty month to a poor one, is misleading, or at the very least, unfair.

I might be inclined to agree, in part, with one but not two of the above. At the very least, I would prefer another data set.

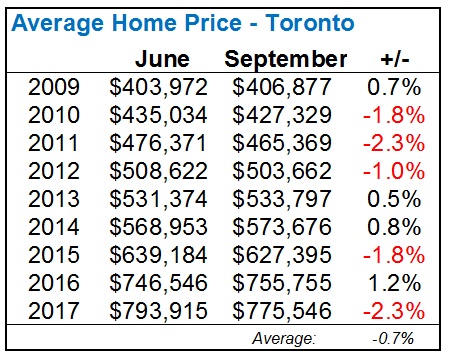

So how about this: since June is typically the “peak,” or at a minimum, the “end” of the spring market, let’s run the above numbers again comparing June to September.

Here’s how things look:

In five of nine years, the average home price decreased from June to September.

The average decrease is 0.7%.

So using that number, and applying it to the $807,971 average home price in June of 2018, we’d come up with an expected average for September of $802,315, which is just on the outside, looking in, of the $806,000 – $813,750 range we predicted above.

Either way, not a bad second opinion on the prediction.

So that’s what I expect in the month of September, and I might even go as far as to predict that the average home price will come in at the higher end of that range, or above. That is based on nothing more than gut feeling, but I sense so much built-up demand, and my phone started to ring today – the first day back in the Fall Market. I think it’s going to be a busy one.

–

2) Sales-to-New-Listings Ratio Will Rise

Another theme so far in the 2018 market has been “slim pickings.”

To be less aloof and more economical, the market has suffered from low inventory.

Now as is often the case, we can pull numbers to show the inventory has been sufficient, whether it’s comparing to last year (when inventory was tragically low, resulting in a 20% gain in four months), or whether we’re looking GTA-wide.

But if you’ll indulge me, let me suggest that 2018 thus far has not seen the flood of new listings that we saw in the fall of 2017, after the slow summer.

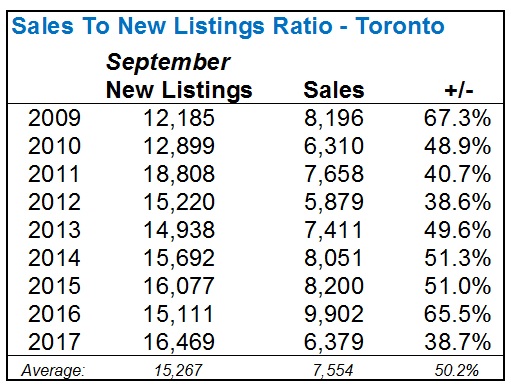

September of 2017 saw a decade-low ratio of sales-to-new-listings, and having said that, the average home price still increased 5.9% from August to September.

The ratio of sales-to-new-listings is not one that is used all that often, but I view it as a measure of how tight the market is. When the ratio is high, obviously prices are rising, properties are selling quickly and in multiple offers (in the core), and the market feels far more erratic.

Here’s how the ratio looks over the past ten years:

The fall of 2016 was a crazy market; not quite like the spring of 2017, but it was, on its own, nuts.

That 65.5% figure makes sense, although I have to say that I’m really, truly surprised by the decade-low being the fall of 2017. Ask any of my clients who bought, or sold, in multiple offers, and they’ll tell you that the market didn’t seem to have an abundance of listings, and/or did it feel like sales weren’t plentiful.

The 6,379 sales that we saw last September wasn’t a decade-low, but it was third-lowest, and barely higher than the second-lowest in 2010. While I don’t think we’ll return to the 9,902 sales we saw in 2016, I think we’ll be over 8,000.

–

3) I Have No Clue What Will Happen With Inventory!

Okay, that’s not a prediction.

I could have said, “inventory will go up, or down,” but that’s even worse.

And I’m being a bit tongue-in-cheek because the chart I’m about to show you can be used to argue either side of the coin.

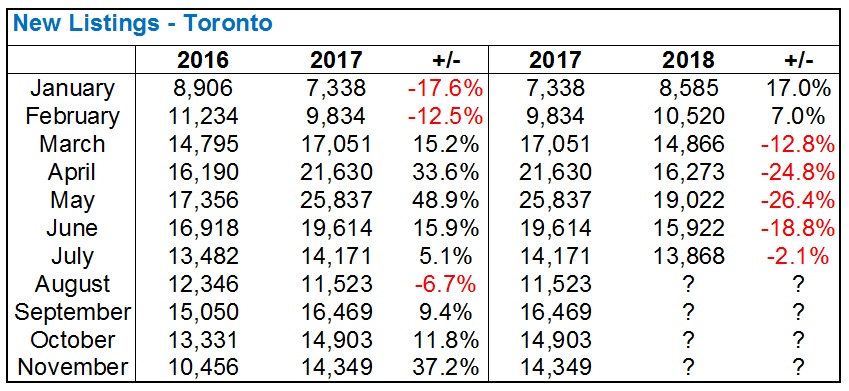

I’ve compared the new listings in 2016 to that of 2017, and then 2017 to what we’ve got in 2018 so far, and the results are interesting.

It would seem that so far, we’ve got the exact opposite of what happened last year:

Note that in January and February of 2017, new listings were down substantially.

This is what caused the rapid acceleration in prices, and that lasted through March, and well into April. It wasn’t until mid-April that things felt a bit “off,” and while it wasn’t felt in the central core until May, the trend had been set.

Note that in 2018, the exact opposite has happened.

Now clearly this is, in part, because the 2017 numbers were so low in January/February, and then so high thereafter.

So if we were to follow the trend so far in 2018, we’d be led to believe that the fall inventory will be higher than last year.

But if we assume that more people listed in the fall of 2017 because the preceding drop in prices put fear into them, then those numbers are inflated, and thus inventory will be lower.

Personally, I’m expecting inventory to be on par with last year. That’s not a “neither here, nor there” argument, but simply I think we’ll see less for sale in the central core, more for sale outside the core, and it’ll even out.

I think we’ll see a lot for sale in the higher price point – over $2,000,000, and a lot less of what “most” buyers want: entry-level condos, and smaller semi-detached houses.

–

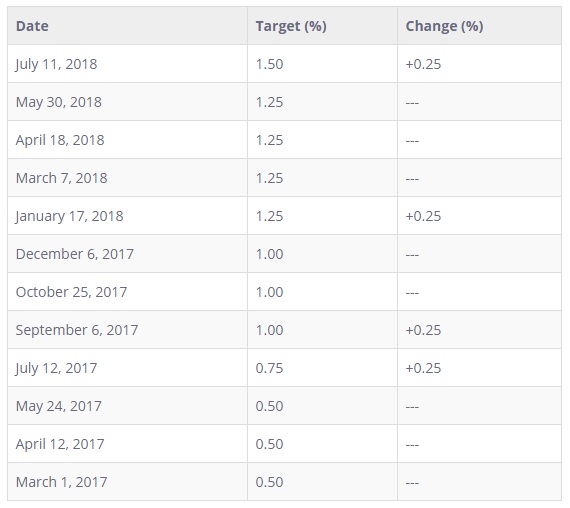

4) The Bank of Canada Will Not Raise Interest Rates

Oh how expected!

A real estate agent predicting that one of the scariest ideas out there among on-the-fence buyers is a falsehood?

Well, call it a hunch.

And this article was also well-timed:

Bank Of Canada Expected To Keep Rates On Hold; But Reasons For A Hike ‘Solid’

The article is a bit of an excuse-maker, essentially saying that rates weren’t raised, however, they would have, could have, should have been, if not for A, B, C, and 1, 2, 3.

But note that the article contains two predictions of its own!

1) The chance of a rate hike on Wednesday is less than 10%.

2) The chance of a rate hike next month is 80%.

I don’t know where they’re getting those numbers. Perhaps they’re just pulling them out of nowhere, kind of like I do, sometimes…

So in the spirit of betting against popular belief, I’ll go on record suggesting I don’t see a rate hike this fall. Call it the Trump effect, call it the fear of a trade war, or call it a gut feeling I have that the Bank of Canada loves this idea that they “could” raise rates, but won’t; either which way, I don’t think it’s happening.

Just as a refresher, here’s where the overnight rate has been during the last 18 months:

5) “Housing” Will Be A Major Theme In Politics

We have a municipal election coming up on October 22nd, and whether we vote for 25 city councilors, or 47 (topic anybody wants to explore??), most of the interest from the general public will be directed at the mayoral election.

I don’t like either candidate, to be honest.

I know we’re not supposed to talk politics in an open forum, but what the heck. John Tory, who ran on the idea of being a “business man to run the city, like a business,” has proved to be a wet noodle that caves to every single politician, constituent, or dog with a cough, at every single opportunity. Jennifer Keesmat is a left-winger, and I tend to take my shots at the net from the right faceoff-circle.

At least Jennifer Keesmat put forth a transit plan that makes sense for the city long-term. $50 Billion is a start. Frankly, I’m waiting for the 50-year, $100 Billion plan that nobody will lay out, since politicians are only in office for four years, and voters don’t care about fifty years.

So alas, we’ll all just stand idly by and watch Toronto continue to cannibalize itself.

That wasn’t my point, but you know me and tangents…

Aside from transit, I have to think that housing is the biggest issue in the city of Toronto. And while the lack of transit trumps the lack of housing, since, as I’ve argued many times before, transit would allow people to live further out of the city, and thus the “problem” wouldn’t be as big, I do have to think that the price of housing is an issue on which more voters will be focused.

As we saw in the Provincial election, it was a race to see “who could promise more stuff.”

I argued that the NDP and Liberal parties were racing to see who could promise more free stuff, but as a blog reader pointed out, the PC’s were running on who could make more cuts, and thus it’s a round-about to the same argument.

As politics goes, we will likely see the same theme play out this year.

I believe that both Jennifer Keesmat and John Tory will spend large portions of their campaigns talking about housing, and while Keesmat will likely make bigger promises, with tangible details, and even put a price on it (whether those plans come to fruition or not, as is often the case), John Tory will, at the very least, make his own watered-down, non-committal, vague promises to “do something” about the cost of housing.

Whether it’s TCHC having a larger role, or building more social/affordable/subsidized housing, or whether it’s talk of helping the “middle-class,” which is always sexy in an election, I have to think that we’ll hear talk of housing over, and over, and over.

What we won’t hear is either candidate talk about “wants versus needs,” and maybe tell little Jimmy that he doesn’t “need” to rent for $2,450 per month at Bay & Bloor, but rather he simply wants to, and should stop complaining about the cost of housing.

Will real estate related taxes come up? More land transfer tax? Higher property tax? Probably not. If anything, raising the land transfer tax on the highest price bracket would be a likely outcome.

No matter what they do, they’ll never be able to trump the single-greatest tax of all time:

The $75 fee the city instituted to pay land transfer tax. Yes, there’s a FEE to pay a tax.

I also think housing will be a major part of the 2019 Federal election as well.

But don’t get me started on that election…

–

So that’s it, folks.

My five predictions, and I saved one more for another day.

The other prediction, or idea, is simply that the notion of “a home as a fundamental right in society today” will gain major, major momentum this fall, and into 2019. In fact, I think it’ll go hand-in-hand with prediction #5, and we’ll see a lot talk about it (mainly from Mr. Trudeau) leading up to the next election.

I’ll come back to this topic next week, as I read more than a few articles about this while I was on vacation, and made a note to bring this up for discussion.

So to the sellers out there: good luck.

And to the buyers out there: well, also, good luck.

The fall market flies by before you know it, so if you’re a buyer, may I suggest that you be diligent. And if you’re a seller, and you ‘need’ to sell, the list, re-list, re-list again strategy never works.

Happy pavement-pounding, everybody!

Ralph Cramdown

at 8:10 am

I’ll take the under on your 8,000 sales prediction (I say 7,600) and the over on your zero rate hikes prediction (I say one, probably in October).

Chris

at 8:59 am

Agreed, on both counts. Probably no interest rate hike today, but with an FOMC hike on Sep 26 a near certainty, I suspect the BoC will move in October.

Additionally, why the use of Sales to New Listings, rather than Sales to Active Listings, and active listings as a way to measure inventory? As Scott Ingram said:

“New listings is a bit of a garbage stat as TREB tracks it. Last year had tons of terminations and relistings, making “new listings” very distorted. I pay way more attention to active listings, which are real.”

TJL

at 8:46 am

I would love to hear more about your unwritten point #6.

Maybe this was one of the articles you’re talking about:

https://globalnews.ca/news/4388059/housing-human-right-canadian-law/

It remains to be seen whether Justin believes “housing” is a roof over one’s head or whether it’s massive subsidies to families who are financially unprepared for the third, fourth, and seventh child that they should not be having, or millennials who lament that they can’t live near their cool friends, or the lower-middle class who insist that home ownership in the central core is a birthright.

daniel b

at 9:41 am

David, the percentage probabilities of a rate increase can be calculated from the pricing of bonds today. If there was a 100% probability that the BOC would raise rates in the future, bond prices would fall today to reflect that guaranteed increase (bond prices and interest rates move in opposite directions). If it’s a 50-50 chance then bond prices would fall, but by less. Using math you can calculate what the market is pricing in as the likelihood of the rate increase based on how bonds are priced today.

m m

at 11:39 am

Hi David, how long is the “fall market” considered to be? Does it include October?

David Fleming

at 12:42 pm

@ m m

The fall would run right through the end of November. I know that’s technically winter, but April, May, and June are summer, and we refer to that market as “spring.”

Carl

at 12:29 pm

It is quite possible that prediction #1 will come true. It is also possible, though not likely, that #4 will come true. But I don’t see any scenario with both #1 (rising RE prices this fall) and #4 (no increase in the BoC target rate this fall). #1 assumes good news on the economy. #4 assumes bad news on the economy.

Housing Bear

at 3:19 pm

Prediction #1 will absolutely come true as it is only comparing average price in august to average price in September. September average should always be higher than August whether the overall trend is up or down (short of some huge economic event happening early on in September). The benchmark average, especially when looked at month over month is not really useful when determining price direction. It is more of an indication of dollar flow and sales mix. Bigger and better properties usually come on the market in the spring or fall. In August you could have 8 condos change hands at 500k a pop and two houses that go for 1m. Total value is 6 million, average is 600k. In September perhaps 12 condos sell at 500k and 8 houses sell for a 1m. Total value is 14 million average is 700k. Sales have doubled, benchmark average is up 16% yet you are still paying the exact same.

Only thing that will stop rates going up in October is a complete disintegration of NAFTA or if the auto tariffs get applied. We are already well behind the last inflation reading.

Carl

at 3:39 pm

The blog post is presented as predictions for the fall market, so I have taken prediction #1 to mean that prices will rise in “the fall”, not just from August to September. But if DF meant just the August-to-September difference then yes, that’s not much of a prediction.

My point is that #4 would only happen if there were serious problems in the economy, NAFTA-related or otherwise, and that would depress housing prices.

Appraiser

at 6:08 am

TREB sales data for August just released: Year over year

Sales up 8.5%

Avg. price up 4.7%

GTA months of listing inventory = 2.6 months.

City of Toronto listing inventory = 1.9 months.

Conditions are ripe for further price gains going forward.

Alexei

at 11:36 am

Hi, so I am new here. Overall it seems that everything is going up, slowly. To me that is a good thing. I guess things will also depend on NAFTA and overall economy, which I hope will improve/stabilize.

I also am reading better dwelling. Is it me, or their articles always try to put a negative spin on the market/conditions. I.e. their newest article does show that sales are up Y/Y but the inventory levels are also increasing, which maybe true (not a huge amount).

Anyways, what are your thoughts on the overall market as it currently stands…

Chris

at 11:49 am

BetterDwelling absolutely takes a negative stance on the Toronto real estate market. I read their commentary, as well as that of more bullish sources, because I feel it helps paint a complete picture. Kyle and appraiser will probably disagree, stating BetterDwelling is misleading, and should be ignored.

Similarly, myself, Ralph, Housingbear are more likely to be pessimistic on the market. Kyle and appraiser, more optimistic. As above, I would recommend you take in all the data and opinions you can, then form your own stance. At the end of the day, nobody knows for sure what the future portends.

Alex

at 12:15 pm

Yeh, David’s blogs are more optimistic.

Overall, I think difficult to predict. My view on the whole market is that for now it is stable. Last year Vancouver market was stabilizing but now, all of a sudden we see that there is a big price drop and a downturn of the market.

I think for Toronto, it will all depend on the overall economy. As long as people can support their mortgage payments, they won’t be rushing to sell at lower prices then what they paid 1,2,3 and 4 years ago. And if people are still paying those prices and there is some movement, then to me it means that prices are fair.

Matt

at 12:46 pm

You may be right that those who bought 1,2,3 years ago won’t sell for a lower price if they can continue supporting mortgage payments. But* they don’t have to sell for the price to go down. A neighbour who bought 35 years ago and has seen 800% gains could sell for lower than the newer buyers purchase price, and that could be used as a comparable and bring all home prices in the area down. Though as Appraiser stated above, prices are slightly up (seems to have stabilized from last spring) and MOI is in traditional sellers territory. 2019 spring market should give us a lot more indication of where we actually stand and where things may be headed. Might be worth keeping an eye on Vancouver as well as Sydney/Melbourne (Australia) markets, as they seem to be 12-18 months ahead.

Kyle

at 1:27 pm

@ Alexei

Based on the comments you’ve made, it is clear you are already quite an astute observer.

Over the long term the market is mostly driven by jobs/incomes, # of households/size of population. If those are increasing(which they are) then real estate prices will increase, if those are decreasing then real estate prices will decrease.

Many other factors come into play but have a weaker or shorter term influence. Be wary of anyone who simply barfs up a bunch of these subordinate factors that support their view, (be that view bullish or bearish). And be particularly wary of click bait outlets masquerading as news, such as Better Dwelling. They have zero credibility and misrepresent data to increase clicks.

Housing Bear

at 4:04 pm

One other major factor I would include is financing. Cost of borrowing and access to credit.

Cost of borrowing

Fraser Institute did a study last year on the impact of falling interest rates on house prices and borrowing capacity. 7% average rate in 2000 vs the 2.7% in 2016, allowed borrowing capacity to grow by 53%. Including the 53% income gain between 2000-2014 would have increased the average households borrowing capacity by 126%. The max mortgage for the average household income was 181k in 2000 – vs 409K in 2014.

https://www.fraserinstitute.org/article/falling-interest-rates-an-often-overlooked-contributor-to-rising-home-prices

Access to Credit – How willing are the banks or alternative lenders to provide credit. Quantitative Easing is unprecedented and has made it much easier for lenders to raise capital to make new loans. Lenders are much more willing to lend during good times.

If the cost of borrowing is increasing and/or access to credit is decreasing than RE sales and values will decrease. If households over leveraged themselves at lower rates expect a huge drop in consumption = bad for economy (potential income/job loss). If they really over leveraged themselves they will have to liquidate/ go bankrupt and if defaults start to pick up lenders will be less willing or able to make new loans = bad for prices. If too much of our economy has concentrated itself in RE and RE related industries, a slowdown would cause jobs/incomes to decrease further and put those losing their jobs/income into a potential default/ liquidation scenario = bad for prices ( as per Kyle’s factor).

These factors can build off of each other into an ugly feedback loop that’s hard to break. Could the Bank of Canada reverse course on rate hikes? Sure but unless the Fed does the same our dollar takes a massive hit, and it may not even do much to mortgage rates as the banks have to raise a lot of their money in the open market and could be upping their spreads due to an origination slowdown/ fear of further loses………… Some other government intervention could also mitigate loses/fallout so I guess we can all sleep easy knowing that we have some of the greatest and most competent economic minds leading this country right now………………..

David Fleming

at 11:43 am

@ Appraiser

You always have the stats before the public does. Even I don’t have an inside source; I just keep “refreshing” the TREB Market Watch page… 🙁

Chris

at 8:06 pm

Active listings also up 8.8% to almost 18,000.

And here’s average price graphed from 2014 to present:

https://financialpostcom.files.wordpress.com/2018/09/toronto-real-estate.png

Oh, and looks like an October interest rate hike is becoming more of a sure thing:

“The speech provided an upbeat assessment of the country’s economic expansion, with Wilkins saying the economy was on “solid footing” with broad-based growth, running close to potential, driven by business investment and exports and households “adjusting well” to higher interest rates.

While the central bank yesterday held off from raising borrowing costs to see what happens with NAFTA negotiations, it indicated in its rate decision that it’s ready to continue hiking interest rates.”

FreeMoney

at 6:58 pm

So David admits that Jennifer Keesmaat (get the spelling right next time) “put forth a transit plan that makes sense for the city long-term” yet he would never consider voting for her because she’s (supposedly) a lefty. So it’s all about labels rather than policy, a sure recipe for crappy (or nonexistent) policy.