I assure you, I take no pleasure in this blog post.

I’m not gloating.

I’m not going to be happy if the condo market goes up 20% in 2020.

I’m just reporting on what I’m seeing out there, alright?

There’s so much anger about the Toronto real estate market right now, I can’t believe it. I can understand it, if that makes sense. I understand the frustration, and to some extent, the resentment, but I never believed that this day would come.

Look at the front cover of Toronto Life this month, or online. It’s a 6-part series about people moving out of Toronto due to high real estate prices.

These stories, the headlines, wow:

Wow, a $350,000 budget.

My first-ever real estate sale was for $295,000 back in 2004.

It was in an older building – a 1,500 square foot condo at Gerrard and Church.

And in 2020?

Well, in 2020, we’re seeing things we never thought we’d see.

We’re seeing, in my opinion, a return to the 2017 market.

There isn’t enough inventory, and thus not enough sales, in the freehold market, to come to any sort of conclusions just yet. But from we’ve been witnessing in the 1-bedroom condo market, there is just no price too high for some buyers.

This is where the bears jump in and talk about how bad the crash is going to be! “People will be walking out the front door, and handing their keys to the bank!”

Can we skip that part, please?

Through Friday of last week, we had seen 205 firm sales of condominiums in the downtown core (C01 & C08) since January 1st.

Of these 205 sales, 109 were listed as “one bedroom.”

What constitutes a “bedroom” is certainly getting grayer and grayer by the day, but let’s just use this data as it was provided to us.

To look at the smaller or entry-level units, let’s refine the search to only include 1-bathroom units as well.

That leaves us with 99 listings, and keep in mind, this doesn’t include those listed as zero-bedroom, or bachelors.

Of the 99 listings, 63 sold for over the list price. That’s 64%.

Of course, if we eliminate the 33 sales that were listed in 2019, and only look at properties listed in 2020 and sold in 2020, we have 52 of 66 selling over the list price. That’s 79%.

Most condos in Toronto are deliberately under-listed, no question about it.

But there are then two conversations to have here:

1) How 1-bedroom condos are being sold in 2020.

2) What they are selling for.

I want to draw your attention to the following sales, which caught my eye, but which are also being talked about in real estate circles.

Because of TREB’s archaic stance on sold data, and because I actually fear they would have no second-thoughts about taking away my MLS access sometime between breakfast and lunch, I’m going to have to black out the addresses. I wish this wasn’t the case, and I’m sorry.

Are you reading this, TREB? I sure hope so. I can’t wait for “change” at the appropriate levels. It’s coming.

–

Sale #1: Liberty Village

Last May, a client of mine purchased a home and we set out to sell his condo.

The same model five floors below him sold for $522,000 in March.

In June, we sold for $580,000.

A huge pat on the back, if I do say so myself. We painted the condo, staged it, and the clients moved out for a week. The table was set for a big number, and we got it.

Fast-forward to January of 2020, and the same unit two floors up came out for sale at $549,800.

Identical layout, although I think my listing had moderately better finishes, but I digress.

Did the market notice?

Nope. Couldn’t have cared less, it seems…

That’s $50,000 more than my then-record sale in a little over seven months.

8.6% in those six months, or an annualized return of about 17%.

I wasn’t kidding when I said the condo market could go up 20%. You thought that was an exaggeration for effect, right?

This model sold for $522,000 in March of 2019, and then $630,000 in January of 2020.

You draw the conclusions…

–

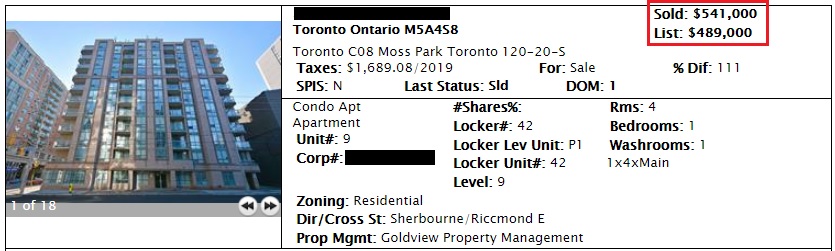

Sale #2: Adelaide & Sherbourne

This listing came onto the market with no offer date, and I sent it to my investors.

The building is small, and it’s plain. It’s unsexy, boring, and not the most appealing from the outside. But’s a value building, or, at least it used to be.

The unit was priced at $499,000, again with offers any time.

The identical unit two floors down sold for $445,000 in April of 2019.

The identical unit, in between these two, sold for $465,000 in September of 2019.

The unit up for sale had a parking space, which in this building is probably only worth $30,000. Maybe less.

Add the parking to the last sale, and we’re at $495,000. So the $489,000 list price was reasonable.

But this was an estate sale, so the unit wasn’t in the best shape, and there’s the risk that the probate doesn’t clear in time for closing.

Would that affect the sale price?

Nope.

This unit is 489 square feet.

We’re now at $1,106 per square foot for a “value building.”

Take $30,000 off the $541,000 sale price for that parking space, and we’re at $511,000. The last sale – for a better unit, was $465,000 in September. That’s a $46,000 increase in four months, or 9.9%. Annually? That’s almost 30%.

I never thought I’d see the day…

–

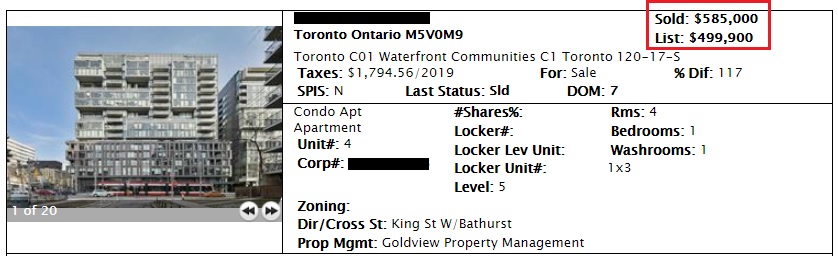

Sale #3: King & Bathurst

This was all the talk last week after the property received seventeen offers on offer night.

Decent building, extremely popular location, and this property was always going to do well.

But how well? You tell me…

The unit was 508 square feet, priced at $499,900.

The same model sold for $540,000 in October of 2019.

How do you think this one fared?

Well, how about $1,152 per square foot:

This is $45,000 more than the previous sale in October, or 8.3% in three months.

Annually, this is over 30% once again.

Want more?

–

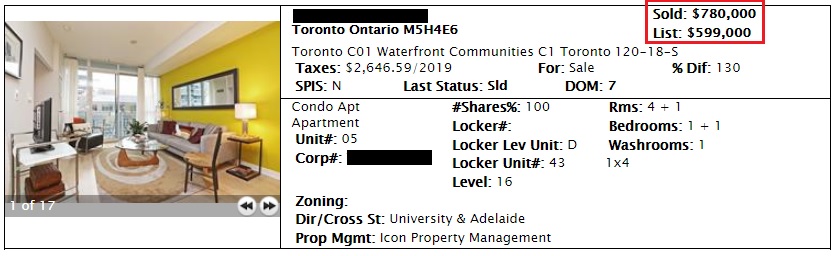

Sale #4: University

Did you ever go to the nightclub Money back in the early-2000’s?

I did. Lineups around the block, and in the end, it was the same as every other nightclub.

There was parking galore back then! In fact, everything surrounding this nightclub was parking lots. Today, they’re all condos.

I’ve been in this building many, many times, but never sold in it.

Last week, a 1-bed-plus-den, with parking, measuring 644 square feet, hit the market at $599,000

Once upon a time, 644 square feet was small. Today, that’s a massive living space.

What strikes me about this sale is not necessarily the price per square foot (even though it’s massive, as you’ll see), but rather that in the past two years, units would routinely sit on the market in this building. They were a tough sale.

That was then, and this is now.

And in 2020, these units, apparently, get 20+ offers.

How did the unit fare?

That’s $1,126 per square foot. With parking, yes. But still. I mean, just…..wow.

–

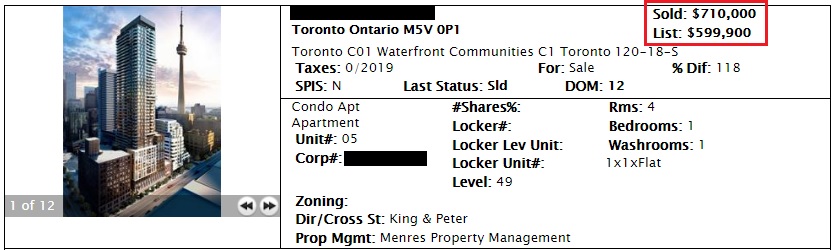

Sale #5: King & Peter

There’s really no “before and after” with this one, folks.

Previous sales are all nuts.

I just can’t believe somebody paid $710,000 for a 1-bedroom condo, no parking, no locker, measuring only 554 square feet:

That’s $1,282 per square foot.

Is this real?

–

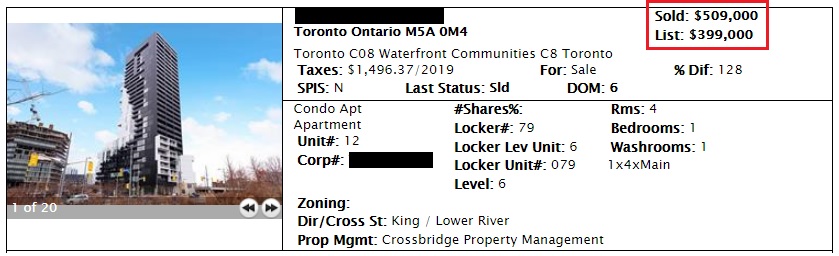

Sale #6: Canary District

Some people call this area “King East,” some call it “Corktown,” and then there’s the made-up “Canary District” moniker.

Call if what you’d like; this area remains red-hot.

When these buildings started to pop up 2-3 years ago, the prices were just outrageous. Considering that you’re not on King Street, at Sherbourne, with the streetcar outside your front door and a Starbucks across the street, I failed to understand the pricing.

I soon realized that pricing didn’t need to make sense. It only matters what people are willing to pay, and it seems that “new” sells.

Last week, a 391 square foot, 1-bedroom condo hit the market for $399,000.

That number – $399,000, is the magic number……for stupid people.

Mean? Yes.

Fair? Absolutely.

You cannot purchase a condo for $400,000 in downtown Toronto. It’s impossible. And yet I routinely have people emailing me asking if I will assist them with their property search, and help them come in under their budget of $400,000. Of course, many of them go on to detail their “must haves,” as though they have any right to be choosey.

Nevertheless, any property listed at $399,000 is going to attract at least a dozen stink-bids, and this property was no different.

There were seventeen offers on this condo. All 391 square feet of it.

The result?

That’s $1,3,02 per square foot.

In the Canary District.

How long have I been asleep?

–

There are units with higher sale-to-list ratios, but we already know how units are being sold in 2020, ie. under-listed, with offer dates to follow.

But in terms of for how much they’re being sold? I’m beyond shocked. I’m actually out of superlatives, and if I weren’t, I still think terms like “jaw-dropping” would cease to have an effect on a desensitized buyer pool.

Are you desensitized? Or are you surprised?

In my opinion, more and more people are starting to believe that there really is no limit to the Toronto market, and that includes a handful of market bears who deny the logic, reason, and fundamentals, but accept that market is going to continue to rise.

When the TREB stats are releawsed next week, I think it’s going to show a dramatic increase in not only the 416 condo price, but the GTA home price as well. I wouldn’t be surprised to see the latter come in higher than the busy month of November.

Francesca

at 6:53 am

David, I am 6 years older than you and I used to go to Money too back then and remember how easy it was to park above ground back then. So much has changed in 20 years in downtown Toronto and in many other areas of the city.

In 2003 I bought my first condo in North York for 185,000 which I thought was a ton of money at the time. I then sold it to a colleague privately for a mere $190,000 in 2006. That shows you how little one bedroom condos appreciated back then. Yes I know it wasn’t a downtown condo but I’m pretty sure that my exact same condo would fetch around 450-550 nowadays if I had only held on to it and rented it out! My husband owned a condo a king and Bathurst, so right downtown, bought it for $180 k in 2002 and sold for a mere $185 k in 2005!

Back then there was already a surplus of one bedrooms on the market and since one plus den and two bedrooms weren’t so much more expensive people would buy the larger units if they could afford it. Now it seems many people are even priced out of the two bedroom condo market so the one bedroom market is all that’s left to enter the market to make some equity. I do wonder though whether these crazy over asking prices are reflecting more investors buying purely to rent out to flip in a few years or actual move in buyers who will squeeze themselves into a small unit just to get into the market somehow. As someone in my mid 40 s I have to say I sympathize with younger generations if this all they can get for so much money now in Toronto. No wonder so many are choosing to stay at home with their parents, rent or leave Toronto like the Toronto life article you reference. We are already worried that our 12 year old daughter will end up living with us forever if prices keep rising like this!

Pragma

at 12:12 pm

Can anyone look at this and say this is a healthy functional market? The people who are jumping in at this point, can you possibly call them “investors”? Will these “investments” ever be cash flow positive? This is what you call a blow off top in markets. I didn’t really have any conviction on where the market was going, but this has made me a bear. I love it.

Appraiser

at 1:29 pm

You must be confused with the stock market.

J G

at 8:09 am

US stock market advanced 25% in the last 12 months, and increased by four-fold since 2009. Sure, keep convincing young people RE is the only way to invest.

I have been telling young couples – just max out your RRSPs, TSFAs,, and RESPs with US index funds. After that, do whatever you want. Funny enough, not many have chosen to invest in a condo even though I know some still have the means.

Appraiser

at 8:35 am

Why not invest in both real estate and equities ? It’s not either or.

And your one-size-fits-all financial wizardry as noted above, appears to be based solely on one magical set of index funds?

PS I see the Dow Jones is in negative territory for the year.

Just ‘sayin.

Chris

at 8:52 am

“PS I see the Dow Jones is in negative territory for the year.”

You must have meant to say the Year-To-Date, a.k.a. the past 17 trading days. Because for the trailing twelve months, it is +14.1%, excluding dividends.

Professional Shanker

at 9:12 am

Investing in US equity funds right now is like buying a pre-con condo today, I was overweight US equities until 2019, perhaps we have more room to run in both.

J G

at 10:14 am

I’m sorry I don’t fudge number.

S&P Jan 28, 2019 – 2640

S&P Jan 28, 2020 – 3265

23.7% increase excluding dividends.

S&P 2009 low – well below 750. Today over 3200.

There are Canadian ETFs that track the S&P like XUS and XSP.

Mxyzptlk

at 11:46 am

The S&P 500 index bottomed out at 676.53 on 9 March 2009 and is now around 3,250 (an increase of about 380% in the last eleven years). But let’s not forget that it hit 1,527.46 on 24 March 2000, meaning it had fallen about 56% over the preceding nine years. Another way of looking at it is that in the two decades from March 2000 to January 2020 the S&P 500 has doubled plus a little, rising a modest 113% which works out to less than 4% per year so far this century. One terrible decade, one great decade.

J G

at 12:13 pm

We can go back another decade. S&P was 250 in 1988. From 250 to 3250 is 8.3% gain compounded annually for the past 32 years.

If I’m about to retire, I would certainly be happy with the portfolio performance.

Mxyzptlk

at 2:32 pm

@ J G

“If I’m about to retire, I would certainly be happy with the portfolio performance.”

I retired in 2006, just a couple of years before the Lehman/Bear Stearns-precipitated market crash. Thank goodness I hung onto my equity (and bond) investments when millions of people were bailing out! And I’m certainly not dumping them now, despite historic highs in most equity markets (although my equity exposure is less than it was in 2006). Diversity diversity diversity.

Alex

at 8:08 pm

This stock market is going up thanks to QE4. Once the music stops playing try to find that last chair…

James G.

at 9:05 pm

Don’t let an out of control Fed backstopping the stock market and suppressing interest rates globally get in the way of a real estate bubble.

Chris

at 3:45 pm

For those of you who aren’t subscribers to The Economist, and thus couldn’t read the previously discussed Special Report on Home Ownership, they have released a 12 minute video that succinctly summarizes the eight articles:

https://www.youtube.com/watch?v=kkVEt5tC2xU

Jimbo

at 7:49 pm

I don’t think I’m surprised at this. I need to look back at the articles and blogs but it seems like $600k is the magic number. It was $600k for a nice house until they hit a million and the CMHC million dollar rule came into force. Then everything at $600k exploded,”rougher” detached and semis, climbed from $600k to 850+. Then smaller semis and larger condos came in at $600k. Then came the stress test and buying slowed a little. Now that it is picking back up and 1 bedroom condos is where people can enter the market and get financing, they are going up. By the end of the year studio apartments will be up there. My question is, what then? This is the point where saturation hits and wee see how well people can move up the property ladder with or without a sale to a new buyer.

If the demographic is new, young freshly graduated or single professionals moving in then the market will thrive.

I’m not saying crash but what happens when the only supply at $600k is a 300-400 sq ft studio?

condodweller

at 8:56 pm

It’s simple, people will live in 300-400sqft condos, which is what they can afford. I commented about this a while ago saying that each type of housing seems to hit a level where people refuse to pay more and less expensive types will be pushed up towards that limit. The limit seems to be that just below 1 million level where SFHs hit and subsequently semis hit. What I suggested was that small condos will be pushed up towards that limit which seems to be playing out. I just wonder how close the prices will be for various types of housing.

Christopher

at 8:27 pm

I can confirm that exact same thing is happening in Mississauga. Have condo investors lost their minds?

condodweller

at 9:00 pm

I don’t think so. This feels like FOMO all over again like it was with houses in 2017 but it’s condos now. I’m really curious how long this momentum can keep up.

Appraiser

at 8:59 am

Momentum at the bottom propels sales in the higher brackets, eventually.

The lucky sellers of these condos, as described in the Toronto Life article, are either investors taking profits (congrats!) or owner-occupiers, some of which are looking to upgrade their living quarters.

P.S. FOMO is so last decade.

Alex

at 10:10 pm

It is not 2017. People are buying properties on borrowed money and banks under stress test rules are willing to lend only minimum. Pretty much all borrowers are squeezed and able to buy only cheapest condos available. Anything above 1.5 mln need to find its buyer and can sit for days and months. This market is artificial and unsustainable unless government starts to tinker with stress test ( hopefully in the right direction ). The biggest problem is not availability of 1 BR apartment, but the way all new buyers are qualified to purchase and borrow under the stress test and squeezed into one bracket.

Pragma

at 8:48 am

Right on. There is no analysis on the merits of the investment. Cash flow projections, cost of ownership, debt to income. Nothing. It’s pure FOMO. It’s literally “I’ve been approved for $600k mortgage, I just need to buy anything I can get for $600k”. Canada leads the world in debt right now. Debt to income of 170%+. If you think the market is going to continue like this then you think Canadians will just go further into debt. What’s the target, 200%, 220%? It is self defeating. The more people’s paycheques go to service debt, the less they consume and invest, the more fragile our economy becomes. You can already see the cracks. Car sales are plummeting. Retail sales are weak. GDP growth of 1% while population grew at 1.5%( which implies NEGATIVE productivity growth). The next recession in Canada will be brutal. We have no cushion, we’ll be starting at sea level.

Clifford

at 4:21 am

Bingo. I like many others had predicted the stress test would do this. People who could Just afford a townhouse or semi got pushed back into condo territory. What it did is create huge demand for 1 beds when there wasn’t as much before as there were less purchasers and hence less demand. So what happens when the couple who was looking at 900k semi pre stress test gets pushed down to 700k along with the townhouse buyer? Well, they’re going to look at a condo and spend to that max so condos start to go for more than thry should be.

Not t mention the horrendous commute whether by car or transit just forcing people downtown. Lack of product, huge demand. That lack of product also partly due to double LTT which was supposed to be temporary. Remember that?

Complete fail from policy makers

Appraiser

at 8:42 am

“Fear of the unknown has shaved 1/4 point off Canada’s 5-year bond yield in just five days. (The 5-year yield leads fixed mortgage rates.) If this downtrend persists, we could very well see widely available fixed-5 rates in the 2.50%-range by next month.” ~ Rob McLister https://www.ratespy.com/sars-2-0-hits-rates-the-dud-first-time-buyers-program-more-012711688

Fuel to the fire, just as the spring market starts to build.

More upward prize pressure on the way?

Anyone?

Bueller ?

Chris

at 8:52 am

Nothing like “Fear of the unknown” to spur people into taking on a jumbo mortgage.

Appraiser

at 9:08 am

Fear has held the bears back for well over a decade now, while real estate continues to boom in the GTA.

P.S. Buying a house and taking on the responsibility of a mortgage has always been risky. Unemployment being the biggest threat. There are no guarantees.

Professional Shanker

at 9:37 am

Buying a pre-con condo using the your HELOC with no intention of renting or owning the condo…..now that is risky! But somehow this would be considered “safer” than investing in a 3 times levered ETF on margin.

Appraiser

at 12:00 pm

Yet another straw man argument.

Appraiser

at 9:02 am

@ Shanker

OK let’s call it a “what-about-ism”.

Still a fallacy. https://en.wikipedia.org/wiki/Fallacy

Chris

at 9:39 am

“Fear has held the bears back for well over a decade now”

Nope. I first became bearish on TO RE and started posting here around early 2017.

Appraiser

at 11:55 am

Congratulations…only wrong for 3 years running.

Chris

at 2:09 pm

Nope.

https://creastats.crea.ca/static/6418057bdd76c52bdd8513081df8e518/ee604/natl_chartC014_xhi-res_en.png

Condos have continued to appreciate since I began posting. SFD jumped up, then fell, and have since more or less moved sideways. But you already knew that.

Appraiser

at 9:04 am

“Condos have continued to appreciate since I began posting.”

Simply posting that you were wrong would have sufficed.

Chris

at 11:17 am

Nah. I’ve had mixed results. Unlike your call on the stock market which was 100% wrong.

Appraiser

at 9:12 am

“Dow posts worst day since October and turns negative for the year as coronavirus fears grow”

https://www.cnbc.com/2020/01/27/dow-futures-as-coronavirus-cases-rise.html

Chris

at 9:46 am

““The Russell 2000 index of small-cap stocks plunged into a bear market on Monday, reflecting a 20% decline since hitting a record high in late August.”

“The Dow declined 508 points on Monday, leaving it down about 12% from the record set in early October.”

https://www.cnn.com/2018/12/17/investing/russell-2000-bear-market-stocks/index.htm

Latest TREB data for November shows sale prices are higher year over year for 6 months in a row.

The stock market is actually crashing in real time, while all you bear-clowns keep praying for a real estate crash that never materializes..but is perpetually “just around the corner, you’ll see.”

Hilarious.

l

!”

– Appraiser, December 17, 2018

https://torontorealtyblog.com/blog/top-five-blog-posts-of-2018/#comment-97086

From your declaration of the stock market “actually crashing in real time” to today:

Russel 2000 +25.73%

Dow Jones +23.99%

S&P 500 +30.95%

NASDAQ +39.55%

J G

at 1:22 am

Hahaha, Appraiser thinks all stock investors are morons. Yes, we all get scared and sell when markets crashes, and then jump in when there is irrational exuberance.

In fact, the word “stocks” itself already has negative connotations.

J G

at 1:24 am

Btw, thanks for bringing that up! He definitely deserves it for all the non sense he spreads to young investors.

I’m just too busy to go back and find them 🙂

Chris

at 11:23 am

No worries, he posts this kind of rubbish so often, it’s easy enough to find!

J G

at 10:32 am

LOL

S&P 25% in the past 12 months, four-fold since 2009.

MortgageJake

at 11:33 am

When the DOW takes a DUMP you BUY more DOW.

Simple as that.

Unless you’re about to retire. Then you should be in bonds. Which also took a dump.

Speaking of bonds. The 5 year is down HUGE and guess what?

Here

Come

The

Rate

Drops

Chris

at 11:39 am

Jake, when you say bonds took a dump, what are you referring to? Yields or prices? Because most bond prices seem to be doing just fine, and these typically move in the opposite direction as yields.

As an example, BMO’s aggregate bond index ETF (ZAG.TO) is up 5.6% over the past twelve months.

MortgageJake

at 4:00 pm

The yield is down from 1.54% to 1.38%. I expect the rates on fixed-terms 5 year to follow suit by 15-25bps over course of next short while.

Chris

at 4:25 pm

Ok, but anyone who owned bonds in their portfolio saw their prices increase as yields declined. ZAG.TO, as a component of the Canadian Couch Potato portfolios, would be held by a fairly good number of passive investors, and climbed a decent amount as I outlined above.

As you’re a mortgage broker, I suspect you’re focusing primarily on bond yields (I would guess specifically the 5 Year Government of Canada bond), when you talk about them “taking a dump”. After all, borrowing rates would be a pretty important aspect of your business.

But for the average investor, bond yields falling over the past year would have resulted in their portfolio appreciating.

MortgageJake

at 8:03 pm

YES I am 100% focused on yields because it drives the rates and that drives my business.

Chris

at 9:35 pm

Right, I get why you’re focused on bond yields. But my initial point was that when you say something like:

“Unless you’re about to retire. Then you should be in bonds. Which also took a dump.”

It seems to imply that people who invested in bonds have suffered a loss to their portfolio. Which they have not. Bond yields have fallen, resulting in bond prices climbing, which has caused an appreciation to most investors’ bond holdings.

MortgageJake

at 11:23 am

The biggest problem that investors have today is – at 20% down *EVERYTHING* is cash-flow negative. However, with capital appreciation going the way it is, old-school “gotta have me some yield” arguments are being replaced with “my cap appreciation is so much higher than my cash-flow loss that I want as many condos as possible”.

If/when that cap appreciation stops (when? IF!?), we’ll have a lot of people paying out of pocket to feed these alligators.

Until then the party rolls on.

Appraiser

at 11:59 am

Not sure I get the logic Jake. If cash flow is negative, capital appreciation or lack thereof does not alter that fact.

Unless you are implying that investors are borrowing from the appreciation / equity to pay the monthly bills?

Pat_A

at 1:21 pm

No what MortgageJake said was quite clear and makes sense of whats happening in the market. Smart investors never breach the first principle of “Yield” first and capital appreciation is secondary and not the other way around. Investors are now driven to buy on cap appreciation over yield and when the tides dry you will see who was swimming naked.

MortgageJake

at 4:01 pm

Exactly.

Say I’m $500/m short on my condo “investment”. That’s $6000/year.

Say my $600,000 condo went up 2%. That’s $12,000.

I’m “up” $6000.

I know, I know, SO MANY other variables, but this is what the majority of my investor clients are doing, saying, and are comfortable with.

*and the sad part is – it has WORKED*. Condo prices have simply gone nuts last 2 years due to stress-test primarily.

Derek

at 4:12 pm

Instead of paying full pop of say, $2,500 per month, they pay $500 and own the condo eventually? Some might find it easier to force save $500 toward the condo mortgage than to an RRSP, psychologically.

Appraiser

at 4:23 pm

You are only up $6,000 on paper and haven’t deducted the expenses involved in divesting of the asset, ie. legals and real estate commission etc.

I’m not sure your theory holds much water Jake.

Appraiser

at 9:11 am

@MortgageJake

Generally speaking, I calculate that a property has to rise in value by at least 10% before you can sell it, just to break even.

That is after accounting for 5% real estate commission, legal fees and other expenses, land transfer tax, mortgage breakage penalty et. al.

Appraiser

at 4:21 pm

Please no more hackneyed cliches.

MortgageJake

at 5:21 pm

I didn’t say the theory should make sense. I said this is what’s happening *in reality*. How else would you explain so many people putting down 20% (from their HELOCs no less) on cash-flow negative condos? Because they feel like it?

@appraiser

Professional Shanker

at 6:06 pm

Appraiser, Thought using your HELOC to invest is a straw man argument? A mortgage broker is confirming this is happening….

MortgageJake

at 8:02 pm

Where ELSE would people get 20%… from “savings”?

ha.

haha.

hahahah! Please. No way.

The equity IS the savings, man!

Appraiser

at 8:56 am

@MortgageJake:

Perhaps like me, they are long-term investors. That’s why ?

MortgageJake

at 10:34 am

I am a long-term investor also. I funded three purchases using HELOC funds *but* I am not cash-flow negative because they are all cash-flow + freehold properties.

MOST (a huge overwhelming majority) of my clients go through this cycle:

Buy for 5-20% down 10 years ago (or longer)

Now have HUGE equity – 50%+.

REFI and add a HELOC.

Use the HELOC as the 20% down on the cash-flow negative condo.

Wait for condo to appreciate.

We are now in the “wait” stage of these people’s investment cycles.

This is my experience (keep in mind I’ve funded over a billion in mortgages in my lifetime so it’s not pick-and-choose)

Libertarian

at 12:35 pm

So let me get this straight….people borrow money on a HELOC, so they have to pay interest on that.

Then they use that money to buy a condo with a mortgage, so they pay that interest as well.

And on top of double interest payments, they have to find tenants and deal with all the headaches of being a landlord?

Then eventually pay commissions, lawyers, and the rest.

So complicated.

Unless of course you don’t declare any of the income and are a despicable citizen of this city, province, and country.

MortgageJake

at 12:38 pm

@Liberitarian

LOL

“Despicable”

Yes you have all of that right and yes some people don’t show this on taxes but that ruins their chances of future financing.

And yes it’s worked out very well for most people who have done this between the last 5+ years.

Kyle

at 2:22 pm

Seems every few years Toronto Life puts out an article on packing up and moving out of Toronto. Such as:

https://torontolife.com/city/exodus-to-the-burbs-why-diehard-downtowners-are-giving-up-on-the-city/

https://torontolife.com/real-estate/the-new-hamiltonians/

Overall i have no issue with these. If people can make it work, i say more power to them. Just one word of warning though, while the idea of cashing out and moving somewhere else to get more bang for your real estate dollar is tempting, it will most likely be an irreversible move. Just look at the people from these articles…Sold their home in the Beach to buy in Port Hope back in 2011. Good luck if they ever want to move back.

MortgageJake

at 11:13 pm

Why would they want to move back if they are cashing out? I’d say most people don’t need/want to move back and/or are downsizing.

For sure it’s an irreversible move. Getting out of the market in general could be seen to be irreversible. But most of these people are just leaving because this city is too expensive for most avg people who didn’t have rich parents (rich in housin or rich in cash or both)

Kyle

at 6:18 am

Sometimes people make the decision, based on their current situation. For example someone whose employer allows them a lot of flexibility. But what happens if you have to change jobs to an employer who isn’t as flexible and your industry is one of those that cluster in the City, like Law, Finance, or IT? Then you’re forced to either change careers so that you can find something closer to home or face a long commute, because moving back really isn’t going to be an option.

I’m just saying, be aware that once you move there’s pretty much no looking back.

Appraiser

at 8:51 am

Yes Kyle, for the most part there is no looking back, especially if you are young, unless you get the BIG promotion.

There are also a set of other transplants – retiring boomers as young as 55 moving to small town southern Ontario and elsewhere, with no intention of owning again in the big smoke.

Others may even keep a condo in Toronto as a pied-à-terre, or to rent out rather than selling it; however the upcoming vacany tax may impinge on that construct in the near future.

Kyle

at 9:19 am

I agree 100%.

If you are young (early to mid in your career), the move can be very limiting to your future opportunities, not to mention the effect it will likely have on your terminal wealth value when you do eventually retire.

If you are nearing retirement/downsizing, i think this can be a great strategy to use that principal res exemption and to set yourself up for a partial or full retirement lifestyle.

Appraiser

at 8:39 am

Dow Futures Fight Back But Two Trigger Words Threaten a Stock Market Crash

If the World Health Organization declares the coronavirus a “global emergency,”…https://www.ccn.com/dow-futures-fight-back-two-trigger-words-threaten-a-stock-market-crash/

Black Swan Event ?

Or time to buy on the dips ?

Chris

at 11:27 am

Maybe this time the stock market will actually crash after it fooled you with that head fake in Dec. 2018!

Fred Guy

at 10:12 pm

To step back from all of this is to see the silliness. Canada does not have a shortage of land. The older generation of tax payers have simply chosen to explode the population and get rich from real estate without paying for the needed infrastructure. Young people and new Canadians are paying the price for them.

The most disturbing thing is to ask how will these people burdened with $2500 per month rental apartments and million dollar 30 year mortgages pay for the mess we left behind?

Pat_A

at 12:01 pm

Ummmmm this is misinformation. People have choice to spread and move as far or as near to infrastructure as they wish. The ugly truth is human beings like to cluster where the opportunity and vibrancy exist. Some will rebel against it and move elsewhere and some just suck it up and live with it and make something out of it. The choice is yours always…nothing to hypothesis on what the decision makers are contriving to benefit from here.

BTW there is no country in the world you can find where empty “buildable” land doesnt exist, no matter what the population is. Its a beautiful thing to own or rent, you pick your choice…The choice you dont have is the price that you pay…which is determined by the market. This applies to ANYTHING and not just Real Estate.