A reader challenged me last week, and today, I’m going to answer that challenge.

I received an email that read: “Must be getting hard to keep putting a positive spin on this market huh? Then again, you’d never post anything negative.”

I didn’t think that was fair, nor do I like when it’s insinuated that I cheerlead the market.

So today, I’m going to post the single most negative thing on the Toronto real estate market that I can possibly find. Sound fair?

I think there’s a difference between being bullish, and cheerleading.

I’ve seen real estate cheerleaders. Many of them, in fact.

I see them every single day.

They’re everywhere.

I was in a house on the weekend that was overtop of the subway, and as train rolled by, and the house began to buzz, I turned to my clients and said, “This is an absolute deal-breaker.”

A couple minutes later, another agent walked into the master bedroom with her clients and told them, “It’s probably not as bad as you’d think, and it’s the sort of thing you’d get used to over time. Are you guys sound-sleepers?”

I started Toronto Realty Blog in 2007 with the idea of being different from the old-guard of real estate. I wanted to be honest and opinionated, but those two things, when combined, in this industry, equal controversy.

I suddenly had this label of being “controversial.”

Well, I suppose when the average age in the industry is 61-years-old, and everybody loves every house, and never says a bad word about it, then yes – being honest is controversial.

The industry has changed a lot in ten years, and I’ve found a lot of like-minded colleagues, as the old-guard in real estate has begun to break down.

I’ve always sought to provide insight and entertainment on TRB; a very tough combination, as we’re all entertained by different subject matter, and some of us are more or less insightful than others.

“Photos of the Week” is many people’s favourite feature, and others’ most hated.

Blogs that break down statistics bore the hell out of some people, while others get out their abacus and play along at home.

And I’d like to think that, while my outlook on Toronto real estate is bullish, people understand that I try to provide my opinion on the real estate market as I see it, while remaining open to contrarian viewpoints.

So I was a bit perturbed last week when I got that email suggesting that I’m cherry-picking topics, articles, or insight that spin the market in a positive way. And don’t get me wrong – I’ve developed a very thick skin over ten years of blogging, but I did pause for a moment and ask, “Is this person a troll, or is there some truth to what he’s saying?”

Right or wrong, I figured, what the heck. I’ll post the most negative story I can possibly find on real estate, and open the topic for discussion.

UBS is a global financial services company, operating out of Switzerland.

They are probably one of the best-known financial services companies in the world, and to many of you, they need no introduction.

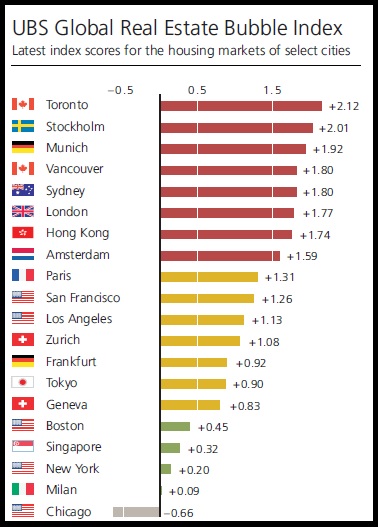

Last month, they published a report called “UBS Global Real Estate Bubble Index,” and guess which city was ranked #1 on their list?

Toronto.

Download the entire 24-page report HERE.

I encourage you all to read the report, and draw your own conclusions.

But since many of you are simply scrolling or killing time on the TTC, let me give you the Coles Notes.

First, here is the Editorial that opens the report:

–

Dear reader,

In Munich, Toronto, Amsterdam, Sydney and Hong Kong, prices rose more than 10% in the last year alone. Annual price-increase rates of 10% correspond to a doubling of house prices every seven years, which is not sustainable. Nevertheless, the fear of missing out on further appreciation predominates among home buyers. After all, the price increases appear rational, for three reasons.

First, financing conditions in many cities are now more attractive than ever before. Second, the global increase in wealthy households seemingly creates constant demand for the most attractive residential areas. Third, building activity cannot keep pace with this demand.

Expectations tend to be prone to exaggerations in boom phases. The optimistic projections of the trends outlined above create ever-greater price fantasies. However, should sentiment change or interest rates increase, a correction is practically inevitable. In the past, rising interest rates almost always triggered a crash in housing markets. In addition, the dependence of prices on international flows of capital represents an incalculable risk. Plus, once demand fell, even the low growth in supply would no longer provide an anchor.

Vastly overvalued housing markets, as measured by the UBS Global Real Estate Bubble Index, have historically been associated with a significantly heightened probability of correction and greater downside than housing markets whose prices developed more in line with the local economy. This year’s UBS Global Real Estate Bubble Index publication reveals the cities in which caution is required when buying a house and the places in which valuations still seem fair.

In this edition, Los Angeles and Toronto have been added to the selection of financial centers.

We hope you have an engaging read.

–

Fair points, to open up with.

I would agree that to see house prices double every seven years is not sustainable, for the most part. But can you paint every city in the world with the same brush? I don’t think so. There are, and always will be, exceptions to the rule.

In any event, here’s the lead graphic from the report, which shows Toronto at the top:

And frankly, I’m surprised that this is the first time I’m seeing it.

Consider that when the Toronto real estate market is booming, the evening news is chalk full of human interest stories, with reporters attending open houses, trying to get would-be buyers to say something on camera about how they’re scared to be priced out of the market.

So now that the sentiments in the media have turned, I’m shocked that we haven’t heard more about this UBS report.

There’s a lot of fine print at the bottom of the report, which might explain why they chose these cities, and omitted hundreds of others that you might expect to see.

I find it interesting that only one city on the list is “under-valued,” according to the report, which of course leads me to believe that the findings of the report, as is so often the case, are theoretical, and don’t or won’t play out in practice.

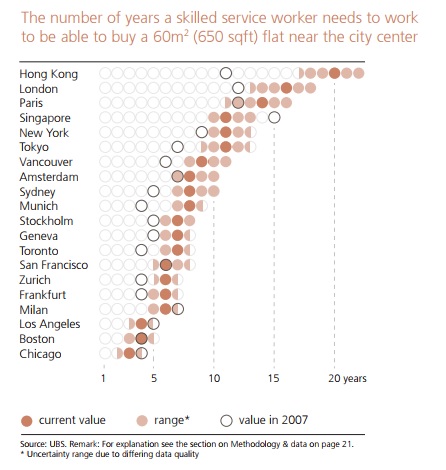

Another feature in the report was a look at the number of years a person must work in order to be be able to afford a 650 square foot condo or apartment.

You would think that perhaps there’s a correlation between the “over-valued/bubble” findings and the following. But note that here, Toronto is 13th out of 20:

I’m not sure we know how to interpret this graph, since, again, it’s theoretical. It’s merely a snapshot, and doesn’t account for inflation, appreciation/depreciation, changes in the interest rate, etc. It basically could be called “average price of a 650 sqft condo divided by average salary of average ‘skilled service worker.'”

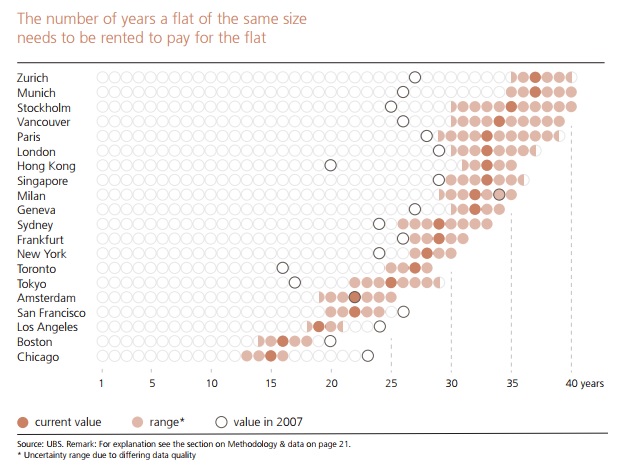

Another feature of the report was a ratio of price-to-rent, which they call “the number of years a flat of the same size needs to be rented to pay for the flat.”

I’m thinking perhaps “price-to-rent” seems more appropriate?

It almost feels as if they titles were something you’d see in Toronto Life to catch eyes.

Have a look:

Here, Toronto is 14th out of the 20 cities.

Even though Toronto was ranked #1 on the bubble list, the UBS report didn’t spend much time analyzing the city.

London, Hong Kong, Zurich, Singapore, and New York each got their own feature page.

Toronto was included on a page called “select cities.”

So what conclusions did I personally draw from this 24-page report?

I guess the first thing I would ask is: How many cities did they analyze?

Did they choose these 20 cities, then analyze them?

Or did they rank 300 cities, and then choose 20 that had appeal?

Either way, I feel like to only feature 20 cities doesn’t give the findings enough context, especially when only one of the cities is “under-valued.”

The second thing I would ask is simply: what was the criteria for overvaluation/undervaluation?

It doesn’t really specify, although perhaps that’s like giving away the “secret sauce” recipe at Kentucky Fried Chicken…

It seems to me that appreciation is most of, or all of, the evaluation criteria. And while I understand the “what goes up, must come down” theory, I don’t think it’s any way to draw a conclusion about where a given market is headed, especially Toronto.

My theory about Toronto has always been a very simple one, and it’s something that this UBS report, and every other like it for the last decade, has ignored: Toronto was drastically undervalued for so long, that only after an unparalleled period of appreciation, have current values caught up.

I can’t say it any simpler than that.

Toronto doesn’t have the history of some of these European cities listed in the UBS report.

Toronto, relatively speaking, is the new kid on the block. In fact, it was only this year that UBS added Toronto to their annual “Bubble Index.”

Call me a homer, or call me biased, but I think Toronto is a different animal.

Toronto isn’t the tulip-bulb version of a city, where a run-up in buying activity – a mania, leads to overvaluation.

There’s no more room to build houses in Toronto, and we’re now starting to run out of room to build condos. The same can’t be said for most cities that have seen real estate speculation bubbles burst.

What makes real estate unique in terms of the relationship between supply and demand, as with any market of buyers and sellers, is that you can break the supply down even further. There’s the actual supply, ie. the number of homes available for sale, and then there’s the actual quantity of the product, ie. how many houses and condos are in existence.

On a go-forward basis, the number of housing completions in the central core is likely to diminish as we’ve run out of room to build.

And yet when I read reports as I have for the last decade on the impending market correction in Toronto, all we seem to look at is the past appreciation.

The fact that 19/20 cities in the UBS report had “positive” bubble scores, once again demonstrates that what exists in theory, or on paper, doesn’t always play out in practice. That’s been the story of the Toronto real estate market as it has continued to defy all the doubters, and I’ll be curious to see where Toronto ranks in the UBS report in 2018, that is, if they choose to include it in their 20 cities…

kd

at 9:02 am

The UBS report is written for the international investor who will never care about Saskatoon or Milwaukee. Even 20 cities will likely be a stretch for most of them. A quarter of the UBS cities are also defined as either “fair valued” or “under-valued”, which on the surface seems about right given the global tendency to congregate in a relatively small number of big name places.

The “bubble index” itself isn’t terribly complicated. It includes two national measures (changes in mortgages outstanding and construction to GDP), two city measures (price to income and rent) and one hybrid ratio (city price vs country price). While the actual weighting is kept secret, it’s pretty obvious that national performance – good or bad – weighs heavily on the index. So Toronto’s over-the-top showing partly damns the entire country.

Most people won’t care about this report and those that do will pluck out the pieces that support their preconceptions and ignore the rest.

However since UBS is internationally renown and the index has been around for 35 years or so, the fact that TO is the bubbliest place they could come up with does matter. At the very least it should cause a few of the global elite to pause before throwing their money down.

J

at 10:35 am

My definition of “real estate cheerleader” is a little different. I don’t consider a real estate agent who sugar coats a negative attribute of a particular house to be a real estate cheerleader. That’s a salesperson hungry for a quick commission. In my mind a real estate cheerleader is someone who evangelizes the general notion of homeownership to anyone and everyone, without any regard to potential risks, current market conditions, opportunity costs, or personal circumstances.

Ralph Cramdown

at 10:52 am

It’s OK that you’re a cheerleader. I believe that a good salesman has to believe in himself, and he has to believe in his product. Expecting a real estate agent to sometimes be bearish on his home market’s prospects is expecting him to fail. The cognitive dissonance of selling a young couple a small home for a huge debt would be soul crushing if he believed he was likely selling them into ruin. How many agents can afford to tell more than a few clients “you should wait a year or two to buy?”

UBS is aiming at UHNW and the assets they are likely to consider investing in. Knight Frank produces similar. Then look at what the IMF and the BIS and the BoC publish, and note the occasional sniping from the Economist. I don’t think any of these institutions have a particular axe to grind with Toronto or Canada. If I were to question the UBS city selection, I’d wonder why Munich was included, and Dubai and Rome excluded.

This is the raging bubble feeling — when international wealth management puts you at the top of the lists and you say that they just don’t get it (N.B. don’t think of tulip bulbs), and when the hot driveway upgrade is an AMG. Anyone living through this real estate market will remember it for the rest of their lives.

Kyle

at 1:34 pm

How many agents can afford to tell more than a few clients “you should wait a year or two to buy?”

In the last 20 years, there hasn’t been a case where this advice has yet turned out to be useful. In fact over the last 20 years, that would have been absolute dog sh1t advice to most of his buyer clients. So i’m not sure how, not telling his clients to wait makes him a cheerleader…

As well if and when such time that waiting a year makes more sense, how do you know he won’t be advising clients to wait?

jeff316

at 9:40 am

You would think that, in this market with its high prices and significant compensation, agents actually have the most leeway to tell people not to buy when the numbers don’t add. I wouldn’t be surprised if this is the time in modern Toronto real estate history that we’ve heard the most agents saying that compared to other times. If they have, though, the advice has been awful – as you identify.

BJA

at 1:49 pm

“How many agents can afford to tell more than a few clients ‘you should wait a year or two to buy?’”

But why should an agent proffer this (or similar, or contradictory) advice to a client? Shouldn’t the agent treat the client as an adult who has made up his/her mind about whether or not to purchase whatever he/she wants to purchase? And what if the advice (as it would have been for quite a while now) turns out to be wrong?

You’re also assuming that David (and by implication every other agent in the world) never says anything along these lines to any of his clients. How do you know this? Why do you claim to know anything at all about what agents talk about with their clients? Even if you’re an agent, you have virtually no insight into the millions of agent/client relationships in this world, so spare us your half-baked opinions masquerading as insight.

steve

at 9:47 pm

“Anyone living through this real estate market will remember it for the rest of their lives”

I suspect so … people are over-extended and pinched, and now the government is introducing legislation (stress test) to protect lenders, not to mention US rates may be rising over then next year or two. Something has to give, and I doubt sellers will see 2017 spring prices again for years. It’s best never to regard your home as an “investment”, rather, best to place it in the liability side of the ledger.

Condodweller

at 10:53 am

“I received an email that read: “Must be getting hard to keep putting a positive spin on this market huh? Then again, you’d never post anything negative.”

So today, I’m going to post the single most negative thing on the Toronto real estate market that I can possibly find. Sound fair?”

David, I don’t want put words into someone else’s mouth, but I think the person who sent you this may have meant to post your negative opinion by posting something negative. You have linked a negative article, sure, then you proceeded to dispute it by saying none of their data and analysis applies, completely dismissing their thesis. You have proven your reader’s case by establishing yourself as a bull/cheerleader. There is nothing wrong with being one of course just don’t try to pretend that you are not.

Geoff

at 12:14 pm

except a cheerleader wouldn’t promote the negative evidence in the first place, no? At the end of the day what people believe is up to them.

Condodweller

at 12:43 pm

He is not promoting negative evidence. That was my point.

Not only does he not promote negative views, he doesn’t even promote neutral views. What could be a more extreme bull view than to say nobody but the elite will be able to afford a house in Toronto in 50 years?

Perhaps he should speak with his colleague Marisha Robinsky. I wonder what he thinks about this article below. Take a look at that inflation adjusted price graph and tell me now is a great time to buy real estate.

http://www.torontohomes-for-sale.com/Toronto-average-real-estate-property-prices.html#Price change graph

Geoff

at 4:52 pm

I wouldn’t have known about the study except for David posting it. Tell me again how that’s not promoting it?

Condodweller

at 5:07 pm

@Geoff It’s not promoting it because he is disagreeing with it. That’s the opposite of promoting it. Was that a rhetorical question? I thought I’d respond as for a second I thought you were serious. If you were being sarcastic I take it back.

If I linked an article about how smoking is bad for you and then I went on to discredit most of its points would I be promoting non-smoking?

Geoff

at 9:01 am

I still wouldn’t have known about the study had it not been shared, the definition of promoting something. I’ll also say that I’m not a robot, I can read the report for myself and judge for myself. But only if I know about it.

Marina

at 10:55 am

Just came back from a trip to Paris, and because I had some time while the kids were napping, I did some virtual real estate shopping. What you can get in Paris for $500,000 is basically a broom closet in a dodgy area.

Now Toronto is not Paris, and I would be the last person to call them comparable, but what would be a reasonable discount for moving from Paris to Toronto? 30%? 50%? we are at about 50% I think, which I would not call overvalued at all. To me, that’s a reasonable price difference. So I totally buy that Toronto was undervalued for years and now is catching up.

That said, I’m sure at some point there will be a price correction and the bears will claim they told us so. But here’s the thing. We bought our house in 2010 and everyone told us we were crazy. The market bubble was going to pop and we would be under water. Well our house has gone up by over 100%. So the market would have to fall by more than 50% for us to lose out. Does anyone really think we are in for a 50% price correction? If so I would love to hear about it!

Condodweller

at 1:37 pm

When you are buying a home to live in you have to drown out the noise of bulls/bears and make a decision that’s right for you. If you look at the inflation-adjusted home price chart in the link I posted in my other comment you will see that house prices in 2010 were about fully valued which means you paid a fair price. You can tell by the average price line crossing the trend line in 2010. All anyone buying a home should care about is if they can reasonably maintain their mortgage payments for the next 25 years because even after a correction, long term house prices should always be higher once we recover from the said correction. And I say should because there can always be a black swan event which could have a disastrous effect on house prices such as earthquakes or a meltdown of a nuclear plant next door. Chances are low, but it could happen. In the case of the latter, I would expect real estate prices to be depressed for a few thousand years.

As for a likelihood of a market correction take a look at how far has the average price deviated from the trendline. Eyeballing the graph I calculate about 29% in 89 and 30% today. In 74 it corrected after about 23%. To put things into perspective we are now more overvalued than at any point in recent history going back to 53 on that graph. According to the article, which I don’t have a reason to doubt, previous busts have been preceded by rising interest rates. Now consider that we have had all time record low interest rates for about a decade and now there is increasing talk about starting to raise rates, which both Canada and the US has started.

I hate to tell you but a 50% correction is certainly possible, not overnight though, however that would bring prices back to what you paid, therefore, it is nothing you should worry about as long as you are not planning a move to Paris and need to sell your home to help with a purchase in Paris.

Kramer

at 2:46 pm

A 50% correction is possible.

A 50% increase is also possible.

You just showed another bias… it’s called “FRAMING BIAS”… you framed your response/analysis only in terms of potential negative results, without acknowledging the possibility of future increase in value.

You are like the most biased guy I know man.

Condodweller

at 4:50 pm

“You just showed another bias… it’s called “FRAMING BIAS”… you framed your response/analysis only in terms of potential negative results, without acknowledging the possibility of future increase in value.”

Again, I was familiar with the concept but I have to admit I did not know the psychological term for it and had to look it up. I learned two things from it: 1. how wrong you are. 2. how my mind works.

1. Framing bias is when you are more likely to make one decision vs. another based on how the problem is presented to you i.e. how it is framed. To use real estate as an example, you would be more likely to invest in real estate if I told you you had 50% chance of doubling your money vs. if I told you that you have 50% chance of losing your money. Also, paying attention to details helps. I suggested that a 50% correction was possible. I didn’t know what the actual chances of it happening was. What I did allude to is that the greatest the deviation is from the trend the higher the chance of a correction.

2. This one caught me by surprise. Here is a quote from wikipedia:

“However, the framing effect seems to disappear when encountering it in a second language. One explanation of this disappearance is that a second language provides greater cognitive and emotional distance than one’s native tongue. A foreign language is also processed less automatically than a native tongue. This leads to more deliberation, which can affect decision making, resulting in decisions that are more systematic.”

I found this extremely interesting as English is my second language. See, someone can be wrong and you can still learn from them. Thanks.

“You are like the most biased guy I know man.”

Apparently, I am less biased than most people. Who would have thunk..

Kramer

at 5:54 pm

Semantics.

Do you think there is a possibility that house prices could go up 50% from here over the next 10 years?

I want to hear you say yes or no. In either case you contradict yourself. Either you’re biased, or an article wielding fear monger.

Condodweller

at 8:25 pm

“Do you think there is a possibility that house prices could go up 50% from here over the next 10 years?”

Sure anything is possible. It’s more possible than you admitting that you are throwing around psychological terms accusing me of being wrong without you yourself knowing what they mean. How’s that for an answer?

“I want to hear you say yes or no. In either case you contradict yourself. Either you’re biased, or an article wielding fear monger.”

I don’t follow your logic. How am I a fear mongerer when I reassured the OP that she should be just fine? It sounds to me that you may have made a recent purchase that you are uneasy about and want me to ease your mind by telling you you made the right decision and it will be up the next 10 years.

If you believe I am biased and a fear mongerer why do you care what I think?

Kramer

at 8:48 pm

You’re a fear monger because even though you admit there is a possibility that the market could go either way, all you do is preach the downside risk from today’s prices.

Just like when an article says “Goldman Sachs says there is a 30% chance of a Canadian Housing Market Crash”… they don’t discuss 70% chance of no crash, or the other probabilities within that 70% of the market continuing to go up. That is called fear mongering.

And to make it worse you dump an article on Marina and others and haphazardly attempt to value the real estate market by year based on an adjusted price graph and trend line… shameful, and I’m calling you out on it.

Condodweller

at 9:32 pm

Ok, I think I know what the problem is here. What I am about to say will sound condescending but trust me it’s not meant to be. You have a basic issue with percentages. You seem to be upset when someone says there is a 40% chance of something they don’t specify there is 60% chance of the opposite. You see percentages are ratios. When someone says 20% of the apples are red, that automatically means the other 80% are not red. When Goldman says there is a 30% chance of a correction that also means there is 70% chance of no correction without them having to spell it out. The irony here is that it is you who is the victim of framing bias. If Goldman stated that there is 70% chance of the market going up you would be happy with that because it’s framed positively even though it means the exact same thing and the likelihood of the market going up is actually more than twice as likely.

Tell me, do you shake your fist at the weatherman when he tells you there is 20% chance of rain and when you look outside you see nothing but sunshine? The weather is also a good example of framing bias. I wonder if people would be happier and go out more of weather reports framed it positively and reported the chance of sunshine vs. rain.

You also need to realize that when you misunderstood me saying there’s a chance of a 50% correction as there is a 50% chance of a correction that is completely meaningless. 50% of something happening is equal to the chance of it not happening. If someone told you there is 50% chance of something happening you should take that as an insult to your intelligence.

So, to put your mind at ease, I think there is a 20% chance of prices continuing to increase going forward.

jeff316

at 9:42 am

I’ve followed this board a long time and Kramer is no real estate cheerleader.

He is not guilty of the bias you find yourself subject to.

That you had to frame him that way to get out of the corner you painted yourself into is dishonest in the extreme.

Kramer

at 11:44 am

much obliged, Jeff

Condodweller

at 12:59 pm

“I’ve followed this board a long time and Kramer is no real estate cheerleader.”

I never called him a cheerleader, you have come to that conclusion on your own.

“He is not guilty of the bias you find yourself subject to.”

I don’t find myself subject to a bias, therefore, he cannot be subject to what I’m not subject to. That’s logic 101.

“That you had to frame him that way to get out of the corner you painted yourself into is dishonest in the extreme.”

I fail to see what corner I painted myself into. Kramer on the other hand kind of shot himself in the foot by misinterpreting/misreading my comment and follows it up with a silly accusation of me being biased which according to his misinterpretation cannot be a bias by definition as there is an equal chance of each outcome. He doesn’t even know what the bias is that he is accusing me of.

“A 50% correction is possible.

A 50% increase is also possible.”

He accuses me of being wrong for drawing conclusions based on historical data and goes as far as complaining about the graph being inflation adjusted to put things into proper perspective. He then throws out his sound counter argument that nothing in the past will be repeated, in fact it will never happen again because the exact opposite will happen:

“Meanwhile, the world is extremely different than before, and whatever happens (up or down), the only certainty is that it will not happen BECAUSE it happened before.”

This sentence again makes no sense at all. So because whatever happened/happens (up or down) will not happen where does that leave us? The market will stay where it is forever? Because it has gone both up and down in the past. Unless of course, he is going to claim that the graph is fake news or it’s just semantics.

Then to top it off you come into the conversation and accuse me of being dishonest! I am sorry but that is just plain laughable. You should take the time and read the thread before you comment.

Kyle

at 11:24 am

IMO, when someone makes a call, supports it and ends up being right that’s simple called “being right”. Cheerleading is rooting for the same team (or thing to happen) year after year, regardless how hopeless the cause…

Geoff

at 12:10 pm

I have to say that I do think you provide a reasonably balanced approach. What people often forget is everyone has some bias – just any educated person should understand that as a realtor, you will have a *certain* amount of pro-real estate bias, by definition. What separates you from the other agent is that you’re aware of it, and try to manage it. That poster who said you’re just a cheerleader is also biased, though most likely far less self-aware. Plus what you post on is up to you’; whether I keep reading it (like I have since 2007) or not is up to me 😉

Condodweller

at 1:04 pm

Please explain to me how I am biased. In fact, I am a realist and more selfaware than you’d think.

It’s funny you should mention selfawareness as I find it is one of my strengths. I always take in as much information as I can from a variety of sources and compare and contrast them to my knowledge and views to continually form my opinions going forward. I don’t pretend to know it all, therefore, I am always open to other’s opinions because it can be based on information/knowledge that I don’t currently have.

Kramer

at 1:11 pm

Being a realist is not the opposite of being biased.

Everyone is biased to one degree or another… cognitively or emotionally.

If you truly believe that you are completely without bias, then you just revealed a few of your biases.

Condodweller

at 1:53 pm

“Being a realist is not the opposite of being biased.”

That is your conclusion, not mine.

“Everyone is biased to one degree or another… cognitively or emotionally.”

I am not qualified to say.

“If you truly believe that you are completely without bias, then you just revealed a few of your biases.”

Again, your conclusion and I never indicated I was “completely without bias”. I am unbiased when it comes to discussing real estate. I don’t sell real estate and I don’t have anything to gain by either being a bull or a bear. That’s what bias means, correct? I have always considered my self to be neither. I don’t like extremes. I would put myself closer to the bearish side along the continuum at this time, for obvious reasons, yet I own real estate.

Kramer

at 2:26 pm

“I don’t sell real estate and I don’t have anything to gain by either being a bull or a bear. That’s what bias means, correct?”

No… That smells more like having a conflict of interest. A conflict of interest is binary… either there is one, or there isn’t.

Bias is not so simple… bias is behavioural, psychological…

Here’s an example of a “behavioural bias” in finance… it’s called “TREND-CHASING BIAS”… it means that when you look at historical charts, you expect that history will repeat itself.

Just like the chart you keep dishing out in posts below.

Meanwhile, the world is extremely different than before, and whatever happens (up or down), the only certainty is that it will not happen BECAUSE it happened before.

So I would put that chart away, it’s a dead giveaway of just how biased you are.

… Or at the very least involve the fact that the world’s central banks injected $9 TRILLION in stimulus over the last 10 years and that rates are still at historical lows… you say you take in as much information as you can… start by showing that you know it’s not currently the year 1989.

jeff316

at 9:45 am

Well put. Conflict of interest and bias are very different concepts.

Condodweller

at 12:08 pm

@Jeff316 Actually they are not that different as a conflict of interest is a form of bias. Bias is when you favour one argument over another for personal reasons/views, where a conflict of interest is when you favour an argument due to financial or other forms of incentive. But as Kramer likes to deal with it let’s call it semantics shall we as it is irrelevant to the discussion.

Kramer

at 8:03 pm

Condodweller, I’m sure that if I said water is wet you would talk yourself into an explanation for why it is not. You should regroup on how you process interactions with other people or you’re not gonna progress much in this world. Google won’t save you. Good luck.

Condodweller

at 9:28 am

“Meanwhile, the world is extremely different than before, and whatever happens (up or down), the only certainty is that it will not happen BECAUSE it happened before.”

I don’t need to say anything. You have already contradicted yourself.

I have already progressed far enough in life and I am not planning on stopping. I don’t rely on luck, but good luck to you.

Jack

at 1:50 pm

If you really think there is no more room to build houses and now even condos in Toronto, you should get out more often. York, North York, Scarborough — empty parcels of land everywhere. In the old city of Toronto, avenues are lined with rows of two-storey buildings that are waiting to be torn down and replaced by midrises, with the encouragement of the city official plan.

Kyle

at 2:09 pm

LOL, just cause there are low rises or empty lots, doesn’t mean you can just go and build on them.

First you have to assemble/buy the land, then it takes like 4-5 years to change the zonings and get the approvals to turn one of those lots into a condo. So yeah more condos can be built, but practically speaking the pace at which supply can be turned out is going to be severely crimped, hence: “There’s no more room to build houses in Toronto, and we’re now starting to run out of room to build condos.”

steve

at 9:30 pm

this is absolutely true

steve

at 9:32 pm

the land to build is there … and the zoning can change over night (remember Barbra Hall and King West)

Kyle

at 9:14 am

…Except zoning did change overnight recently, to protect those two storey buildings

http://www.cbc.ca/news/canada/toronto/midtown-heritage-protection-1.4261609

Kyle

at 2:55 pm

I’ve said it before and i’ll say it again. This whole argument that David is a Real Estate Agent therefore he is obviously cheerleading/pumping the market is just so stupid, and it reveals far more about the accuser’s ignorance of the real world than anything else.

A successful Agent’s biggest assets are his/her reputation and market knowledge. There is nothing but downside to putting his/her name on the line and pumping the market unjustifiably. One would have to be a real dumbass to think that pumping the market would be worthwhile for an Agent like David.

Condodweller

at 4:11 pm

@Kramer You should google concepts before you post them as facts. I am very familiar with trend chasing when it comes to investments. Just to be sure I googled it to make sure my understanding was correct. The key word in trend-chasing is trend. Trend chasing bias is when people are more likely to invest in something after it has gained value i.e. trended up and it is, in fact, more likely it will lose value, and more likely to sell an investment after it has been losing value i.e. trending down when it is in fact more likely it will gain value. It’s also known as the greater fool theory. People keep piling into an investment that has been gaining value exactly at the wrong time, i.e. just before the trend reverses. You can also lookup the emotional curve of investing that I have linked here in the past. It can greatly enhance your wealth if you learn it and apply it.

The chart I was referencing shows the cyclicality of real estate market which tends to be correlated to the business/economic cycle. If you believe that the real estate market will decouple and will continue its current trend line up I suggest you find out what cognitive disorder you have and take action to mitigate it. Others in this forum would probably call it delusional.

Condodweller

at 4:13 pm

This was meant as a reply to Kramer’s first response to me. I did hit reply on it to comment….

Kramer

at 5:10 pm

Hahahaha… “Google it”!!!!!!! GOLD!!!!!!!

Trend Chasing Bias 100% applies to your brutal posts below. The key point is that you assume that because something happened before it will happen again in the future and you let that impact your decision.

Whether it’s a weekly gain in a particular stock or a “real estate cycle”… whatever your system, timeframe and the asset is, it’s taking a position (long OR short) because of what has happened in the past.

If your stubbornness in sticking to your Google-found definition is bothering you too much to receive my point, then call it the “believing the past as a predictor of the future” bias. Whatever you call it, you have it!!!

BUT…

I have worse news for you… your Google-based education is not even the problem for you on this board going forward… because you just blew all your credibility by saying the following:

“If you look at the inflation-adjusted home price chart in the link I posted in my other comment you will see that house prices in 2010 were about fully valued which means you paid a fair price. You can tell by the average price line crossing the trend line in 2010.”

Translation: You said that the trend line determines if something is over or under-valued at any given time.

That is without question the WORST thing I have ever read on this board.

If this were true, then your valuation at any moment in time would not consider any new information and would only consider the past.

You might want to think that one through and grasp it before you go investing… in anything… at all.

Condodweller

at 8:00 pm

It’s somewhat comical to see you back paddle by attacking me. Trust me you don’t need to worry about me. I have no need to change your mind. Just go buy your next property because you know it will appreciate 50% the next 10 years.

Kramer

at 8:16 pm

I never said it WOULD. I said it was possible. Just like the market declining 50% is possible. When you’re biased, as you are, your mind is closed, you have made your decision and no new information will change your mind.

I’m done with you Condodweller. I feel like I just debated with a bag of hammers.

sevyn

at 1:58 pm

Kramer why are you so hyped up on this blog? are you a home owner or are you someone who missed out? Why are you blasting Christ for having his outlook? YOU ARE NOT CORRECT EITHER – so relax!! Look with all your comments – this is a fact – people need to get it through their brains – it isn’t about speculation, rules, supply vs demand, bubbles, interest rates etc – ABSOLUTELY NO ONE can predict the future of real estate. — NOT EVEN AN ECONOMIST. Everyone just needs to sit and wait. The government is and will do anything to stop further price increases. Stop looking at stats or even comparing Toronto to other cities. Obviously it had to stop one day – prices cant keep going up. The fact still remains and will always remain that you cannot go wrong buying real estate – you’d hope one day to either pay it off or make some money on it. So stop going back and forth trying to prove theories. There isn’t one. I don’t think there is anyway.

sevyn

at 1:59 pm

sorry I meant Chris!

Alexander

at 8:48 pm

UBS report basically is reactive because the market deflated already. Pretty much from January 2018 and up to at least May y-o-y everything in Toronto real estate will be in negative territory. This is just simple math and common sense, We are not going to see spring 2017 prices for a long period – courtesy to Fair Plan, interest rates, tightening, new policies, etc. I would not be surprised to see 20% -30% decrease in prices y-o-y in February and March. There is nothing to argue about – whether you call it bubble or not – prices are not going to be the same because of those policies. UBS did the same thing as David for Sept/Oct prices increase prediction – using data and some calculation it was clear that prices will go up after August.

Appraiser

at 8:11 am

I agree, there’s not much to argue about – except that (a) you made a prediction (sorry, nobody knows the future), and (b) most people apparently can’t differentiate between a bubble and a boom.

Meanwhile, TREB released it’s third quarter condominium report yesterday:

“The average selling price was $510,206 in Q3 2017 – up by 22.7 per cent compared to the average of $415,894 reported in Q3 2016.”

Chris

at 10:19 am

David, your main counter to the UBS conclusion is that “Toronto is a different animal”. I would simply point out that this is a very common sentiment of those caught up in a bubble.

“Throughout history, rich and poor countries alike have been lending, borrowing, crashing–and recovering–their way through an extraordinary range of financial crises. Each time, the experts have chimed, “this time is different”–claiming that the old rules of valuation no longer apply and that the new situation bears little similarity to past disasters. With this breakthrough study, leading economists Carmen Reinhart and Kenneth Rogoff definitively prove them wrong.”

https://www.amazon.ca/This-Time-Different-Centuries-Financial/dp/0691152640

Kyle

at 10:27 am

“My theory about Toronto has always been a very simple one, and it’s something that this UBS report, and every other like it for the last decade, has ignored: Toronto was drastically undervalued for so long, that only after an unparalleled period of appreciation, have current values caught up.”

Actually his argument reads to me that Toronto is NOT different, hence it’s values caught up to other large cities.

Chris

at 10:34 am

I mean even that argument is saying that Toronto is different, in that other cities were fairly valued and Toronto was unique in being undervalued. Because of that the old rules of valuation no longer apply.

Do you see the parallels in that train of thought to the quote I posted above?

Kramer

at 11:08 am

Chris, you were the one talking about assigning a proper valuation to Toronto’s Real Estate market… and you believe the market is overvalued now.

In your opinion, has there been a time in the past (5-10 years) where it was undervalued?

Or can real estate only be fairly valued or overvalued?

Chris

at 11:31 am

Of course real estate, just like any asset, can be undervalued, Kramer. That should be a given.

Personally, I think the market has been overvalued for awhile. I don’t have the data or memory to say exactly when, in my opinion, it moved from under to fair to overvalued. However, roughly, I would say it was undervalued from the mid-90’s onwards (after the last crash), and as prices moved up, probably swayed into fair valuation around the mid-2000’s and into overvaluation around the early to mid 2010’s. Again I’m going off my memory here, so take it with a grain of salt!

Kramer

at 11:37 am

OK… then I don’t see your issue then with David thinking Toronto was undervalued… and why you think it implodes old rules of valuation… or why it’s saying “this time it’s different” in the idiotic sense of it.

Chris

at 11:42 am

I disagree with it, in the timeframe he seems to be suggesting it applies to.

Were we undervalued in 1997? Probably. Were we undervalued in 2014? Probably not. Are we at fair value today? I don’t think so, and it seems neither does UBS, or the other organizations who have recently warned on our real estate market.

Kramer

at 11:56 am

OK so you disagree with his valuation… big deal, I disagree with you and the metrics you use as well. You can’t say that higher valuation party is always saying “this time it’s different” in that negative context just because you disagree with their valuation.

Chris

at 12:25 pm

Kramer, David literally says in his post “Toronto is a different animal”, compared to the other cities. It’s hard not to interpret that as saying “this time it’s different”.

Kramer

at 12:56 pm

He is not saying that in the same context of your book. I’m the context of your book, people say “yes! It’s overvaluated! It’s batshi+ crazy! BUT this time is different!!!!!”

He’s saying “I don’t think there is madness. I don’t think Toronto is in a bubble.” You’re allowed to take that stance without being an idiot because of your book.

Maybe you should, for fun, try writing a post addressed to all the people who were crying bubble/pop/crash 3-5 years ago. What would you say to them? I’m curious.

Chris

at 2:37 pm

Kramer, the quote and the book directly discusses those who believe that the asset in question is not overvalued because this time is different.

Kramer

at 4:02 pm

Here’s what I’m trying to say… Both your shot at David and your book are predicated on the FACT that the market is INDEED FACTUALLY ACTUALLY overvalued/in a bubble.

The book is written in hindsight, so it can easily pin point (forgive the pun) when a bubble TRULY existed and when it popped, and thus who is a donkey.

Your shot at David is also predicated on the FACT that we are INDEED FACTUALLY ACTUALLY in a bubble. But we are not in hindsight, we are in real time… so I want to know who decides we’re in a bubble today, thus allowing any bull you come across to automatically be a delusional idiot.

Is it UBS? Because I’ve seen these reports come out before… every year.

Is it you and your fundamentals? Because if the market is overvalued against them today then the market would have also been overvalued against them 3 years ago. Maybe YOUR fundamentals aren’t THE fundamentals.

Is it the Bank of Canada? Because they just purposely tranquilized the shi+ out of the market.

Maybe we are in a bubble, maybe we aren’t in a bubble… but I say that until it’s in the rear view mirror you can’t accuse anyone of being a “this time is different” person.

It’s kind of like someone who has consistently been wrong is imposing a ‘presumption of incorrectness’ on people who have consistently been right. It’s fascinating. Not ballsy… because you don’t have any skin in the game… but fascinating.

Chris

at 5:19 pm

David literally said “Toronto is a different animal”…I don’t know how else to interpret that other than as an iteration of “this time its different”?

Kramer

at 5:31 pm

Weak, Chris. Challenge yourself.

Chris

at 6:21 pm

You can call it weak if you like. That’s your prerogative. I disagree.

Kyle

at 11:17 am

Correction it is saying Toronto was different. Is that not the whole premise of the argument that things that are different eventually become like? To me it’s just like you saying Toronto is different than it’s historic ratios, therefore it will revert.

Why is it OK for Toronto to start off different in your example, but not in David’s?

Kyle

at 11:25 am

Also just to be clear i don’t subscribe to this idea that things can’t be different. IN act i think the whole notion is pure bunk and is all too often used as a dismissive overly simplistic (to the point of being meaningless) type of argument. IMO it is always different, each and everytime.

Chris

at 11:35 am

Cities can absolutely be different in their compositions. But economic cycles are rarely different. That’s the point. While Pheonix and Hong Kong and Toronto are all different places to live, the entire premise of that book is that they are subject to very similar economic forces and cycles; anyone who says “it’s different this time, therefore the old cycle does not apply” has historically not had a good record of being correct.

The details can be different. The outcomes are usually the same.

I’d highly recommend reading the book, as it’s quite interesting (if a bit dry at times when discussing methodology)!

Kramer

at 11:41 am

Yah, but Chris…

4 years ago people were saying “THIS IS A BUBBLE.”

and 4 years ago people were saying “THIS IS DIFFERENT”…

So where is the line? … when is it actually different? … what is it relative to?

Break out some Einstein.

Chris

at 11:44 am

Again, remember that real estate cycles can move very slowly. An average of 18 years in the United States. And you need to consider who was saying it 4 years ago; was it fringe economist or traders shorting our banks? Who is saying it today; big Canadian banks and credible international organizations? There’s a big difference in the weight one should apply those voices.

Kyle

at 12:01 pm

I think just about all bulls and all bears understand and appreciate the existence of economic cycles. My point is every cycle is different with respect to what drives them.

Without reading the book i will say history can provide some clues to how things in the future may play out, however IMO the bears over play this and have strong tendency to misinterpret history.

Basically i understand the bear’s interpretation of history to be that certain ratios they call “fundamentals” can’t diverge too far from some historic level or the cycle will end. Though they admit they have no idea as to when but just that it will – could be 5, 10, 18, even 50 years. To me this exhibits all the hallmarks of poor analysis, confirmation bias and belief perseverance. In good analysis, you don’t just come up with hypothesis you actually seek to quantify the correlation and sensitivity. If the market can take 50 years before responding to your “fundamentals” then your fundamentals have low correlation and sensitivity therefore you reject it. Instead you guys assume that your hypothesis is right, and that the market just hasn’t responded yet. In my view this is more akin to faith-based research than fact-based.

My interpretation of history is different, and dare i say far more plausible. It correlates very well with the market and requires no faith whatsoever. My view is that every now and then some unpredictable random (hence why it could be 5, 10, 18 or 50 years) exogenous event may occur that ends the business cycle. At which point values fall and yes those ratios will fall too, as a result of the cycle ending, not as the casue

Kramer

at 12:16 pm

I agree.

Chris

at 12:31 pm

What you’re talking about isn’t analysis but rather forecasting. The latter is much harder than the former.

Anyways, as I’ve said, we can have different opinions on where the market is going, but I would caution against placing too much weight on the assessment of “Toronto being a different animal” and thus discarding the assessments of these economists.

Kyle

at 12:53 pm

“What you’re talking about isn’t analysis but rather forecasting. The latter is much harder than the former.”

I’m not following to me they are very similar if not the same. In order to be good forecaster, you have to be a good analyst. What is the point (other than to perpetuate a false narrative), of analysis that would lead to bad forecasts or ones that take so long to materialize that no one can say the forecast had any bearing on the outcome?

Kyle

at 12:57 pm

Mean to say…

What is the point (other than to perpetuate a false narrative), of analysis that would lead to bad forecasts or forecasts that take so long to materialize that no one can say whether the analysis had any bearing on the outcome?

Chris

at 2:38 pm

I don’t really follow your question. Economists make forecasts frequently. But trying to time any market is usually not something they advocate.

An economist may tell you they think Tesla stock is overvalued. They’re not going to tell you the date it will decline.

Kyle

at 2:55 pm

When good Economists make forecasts, they pretty much always provide some kind of time horizon (e.g. near term/long term. to the next meeting, the rest of this year, etc). To be completely honest it is only RE bears that seem to operate like it’s ok for a forecast to be indefinitely open ended. This is why you guys always get compared to a broken clock.

Kramer

at 4:18 pm

Actually, even UBS is not specifically saying Toronto and the other top “bubble index” cities will suffer a crash… it just says they have heightened probabilities. Which basically means depending on what happens in the future (i.e. recessions, big events, etc), these cities have greater chance of a correction.

Which aligns with reports like Goldman Sachs saying “30% chance of Canadian RE market crash”… essentially they are putting higher probabilities on certain cities or regions, but the probabilities are tied to other probabilities of certain events taking place that they have also worked out… they are not explicitly saying it WILL happen.

And I guess that’s the difference between Bears and economists… Bears simply say that no matter what happens in the future, the market is gonna crash, full stop… (but they won’t put a time stamp on it of course).

Chris

at 5:23 pm

Yes that’s how most economists I’ve read report on the housing market. Typically it’s related to risk of a downturn, rather than a prediction or timing. UBS is doing exactly that in this report. They’re warning potential buyers of the risk, rather then speculating on a date.

Kramer

at 5:43 pm

Tied to probabilities of other events happening first. In other words. other events cause the correction. The correction doesn’t just happen for no reason. Have you worked out all your probabilities of these other events taking place?

Chris

at 6:22 pm

I don’t recall reading any reports from economists saying that Toronto real estate will only decline if certain specific events take place?

Kramer

at 7:53 pm

Why do you think Goldman Sachs said 30% chance of a crash? Run that through your brain on what that could mean. Is there a wizard living on toronto island spinning a 10 section wheel where 3 of the sections say “crash”?

They run forecasting models with probability weighted outcomes for many different events (ie recession, employment levels dropping, interest rates rapidly rising), and based on the results of the models they determine there is a 30% chance that a event or combo of events will take place that will mean a crash in Canadian Real Estate.

You should take a course on financial analysis. You would dig it.

Chris

at 8:50 pm

Thank you for the suggestion but I don’t think I need to add anymore financial analysis courses to my resume.

Also that sounds more like you’re describing CMHC’s stress testing methodology (for their ability to withstand a crash). I don’t recall Goldman’s report mentioning these scenarios. Rather they claim their prediction is based on assessment of overbuilding, mortgage debt, price growth, etc.

http://www.cbc.ca/news/business/goldman-sachs-house-prices-1.4119982

Kramer

at 9:11 pm

Tell me where the 30% comes from. There’s a 30% chance we’re overbuilding? Does that make any sense?

Walk yourself through it man, for the love of god, you seem like a smart guy. Don’t just paste an article… explain it. Where does the 30% come from?

Chris

at 9:17 pm

They say in the article that their methodology considers mortgage debt, price changes and overbuilding. They are concerned about rising interest rates. They do not mention the events you talked about before. However the CMHC internal stress test does; are you sure this isn’t what you’re thinking of?

If you have access to the full report, please feel free to share it. Otherwise I will take the Goldman representative at his word from this article as to how they make their forecasts.

Kramer

at 9:30 pm

I listed those as hypothetical model inputs that should be included in such an analysis… and yeah, they are used in many models, because they are what drives market booms and busts. You mentioned interest rates as a model input, I’m sure they also factored in probability of a recession and other key events in their model. That would make sense wouldn’t it? It’s common. It’s not exclusively in the CMHC scenario stress test. Home Depot Canada runs the same scenario analysis when they’re building their strategic plans for god sake. IT IS COMMONPLACE.

You’re dancing around the main point here, which is that you are calling for a market crash as inevitable, regardless of what happens in the future. You haven’t run any models or factored in probabilities of potential events or scenarios in the future. You just cry out crash, and wait. That’s fine, people do that, but now you’re denying it and debating like a chump. So good luck Chris. You’re rid of me for good! Way to go champ.

Kramer

at 9:35 pm

And you still didn’t explain where the 30% comes from, or even how it can be a % if they are dealing in certainties like you think you are. I guess there’s a wizard with a magic wheel after all. I hope we get lucky!

Chris

at 10:38 pm

Kramer, you’ve now called me an idiot and a chump in our discussion. I’m not gong to debate with you while you’re being rude.

Have a good evening. Hope you’re in a more civil mood next time.

Condodweller

at 9:23 am

@Chris “You’re dancing around the main point here, which is that you are calling for a market crash as inevitable, regardless of what happens in the future. You haven’t run any models or factored in probabilities of potential events or scenarios in the future. You just cry out crash, and wait. That’s fine, people do that, but now you’re denying it and debating like a chump.”

I used to think that Kramer and Kyle were the same people because they both have the same tendencies when it comes to debate. I don’t think that anymore because they have different styles but they do operate the same way. They take on extreme views without being able to back them up with sound data and analysis. OTOH though when they are presented with the same they dismiss it out of hand and try to discredit what they have been presented with by accusing you of various biases they don’t even know what they mean. Finally, when they run out of arguments they resort to baseless name calling.

They have a set view that RE markets will continue to go straight up forever which they try to back up with cherry-picking data which they find in various reports that suits their standpoint. I think they maintain their point of view because they have never had a negative stimulus which might change their mind. The story has been the same ever since I started following this blog a few years ago. All the bears are wrong, and they are right mostly because the bears have been wrong for a long time and because they have been wrong for a long time they will never be right. They love to through around psychological terms they don’t seem to fully understand.

I wonder what their story will be once the inevitable happens.

It’s disappointing as I like a good debate where I learn something in the end but it’s not worth the eventual verbal assault in the end. In the real world, they are called bullies. I have put Kyle on mental ignore until the ignore feature is added to the blog, perhaps when likes are implemented, because in my eyes no matter how strong his arguments sound like, he totally discredits himself with his behaviour. I have just gone through the gauntlet with Kramer and he is very close to going on my ignore list as well.

Kramer

at 9:48 am

Condodweller suggests on TRB:

“Regarding why OSFI did this is neither reason listed above (ie. either an attempt to reign in borrowing among Canadians, or an attempt to cool the market). They want to protect CMHC from mass defaults.”

Ben says:

The new changes actually have nothing to do with CMHC.

These changes are directly aimed at the part of the market that CMHC does not really play in, the conventional mortgage market (80% loan to value or less).

It’s ok, I’m sure Ben the expert is wrong… if not, just put him on mental ignore.

Kramer

at 10:16 am

You know what both your problems have been lately, and why since I’ve been in a bad mood I have gotten so frustrated with both of you? It’s that when someone else is correct on anything, you don’t acknowledge it, you nitpick some tiny mundane detail that is inconsequential tobthe overall point being debated, and then you create a sub-debate on that tiny mundane detail in some attempt to save face.

And if someone has you completely subdued in an argument about something (ie how you valuate real estate, Condodweller), then you also do not acknowledge it an just pretend like it never existed.

You have both been obstructors of progress and seeking of the truth… so I’m not debating with you anymore, because it is pointless.

Kramer

at 10:47 am

And the thing that threw me off the most was Chris basically throwing his hands in the air saying (paraphrased):

“Nope, we cannot assume that Goldman Sachs includes their estimated probability of a recession into their estimated probabilities of a housing market crash. I don’t care if it’s the most rational thing EVER said on earth, I didn’t read it, and I won’t assume it, so you are wrong.”

WEAK, Chris… Obstruction of progress. Not worth any more time.

And even if Goldman didn’t (and that is a big IF) they SHOULD have, and that is a fact, and that is THE point.

You know what else they PROBABLY factored in? The likelihood of government intervention. And if they didn’t then their model was weak because that’s the only thing that has slowed things down so far. Or maybe they did include it as a positive thing for the market… maybe they assumed in the model that if the government intervenes in the next two years then the risk of a true crash will decline.

And Condodweller, your using of that adjusted price chart and trend line to tell another reader what their house is truly worth was BAD but you not even acknowledging it was worse. Also not worth any more time.

Neither of you are trying to learn, you’re both just exclusively trying to be right… you stink of it.

Best of luck.

Kramer

at 11:56 am

“I wonder what their story will be once the inevitable happens.”

I have always stated that a crash or correction or anything is possible. It will depend on what else happens. Will the economy remain strong (I predict yes), will the CDN dollar skyrocket (I predict no), will there be a recession (I predict no in the near term), will interest rates jump 3% in a year (I predict no), will North Korea shoot a nuke (I predict no), will the government continue to tinker with policy (from today onward, I predict no) etc.

These unknowns will determine what happens with the real estate market.

I honestly did not see the governing bodies interfering this much to date. I wouldn’t have predicted this much intervention. On that I have been wrong. But it hasn’t destroyed the market. And when the Vancouver market was regulated for foreign buyers, the market reached new peaks a year later, so I will certainly not say that is IMPOSSIBLE for Toronto as well.

You’re the one that says it’s inevitable (you just said it)… and that’s why you’re impossible to debate with.

Kramer

at 11:59 am

And good lord… you say you’re not biased… and you just said “when the inevitable happens”.

Please please please admit you have biases.

If you don’t after saying that, then there is no helping you.

Kramer

at 12:13 pm

And no Chris, that was not a complete or perfect list… nor is it from a CMHC stress test… it’s supporting a point… here’s some more…

Will GTA population continue to grow – I predict yes.

Will employment levels stay at healthy levels – I predict yes.

Will new supply construction still be an overall ‘issue’ – I predict yes.

Will rates stay near historic low range forcing investors into other asset classes including real assets and real estate – I predict yes.

Etc. Etc.

The point: This general line of thinking is where predictions / probabilities / forecasts come from. You assign probabilities to key inputs or drivers of the thing you want to forecast. It’s how you forecast in macroeconomics.

It’s not like in USA 2008 where there was indeed an INEVITABLE trigger which was in 2007 when adjustable interest rates were scheduled to jump across thousands and thousands of risky mortgages at once (this was the first domino to fall).

There is no inevitability or certainty in what will happen with the Toronto RE market. If there is, you certainly haven’t identified it.

Adele Stanidis

at 4:15 pm

I think that the real problem with real estate prices are the buyers that continue to buy into it day after day. If the buyers would just stop then those listings would have no place to go but down . Is it really that important to have a mortgage that high that you can’t just say no way am I paying that . The more people who do that then the prices will have no place to go but down. You have the power to dictate the prices . If the listing sits there without any interest then the seller will have to reduce the price that’s if they really want to sell. Warning as well to not trust the realtor, come on folks they are loving this market!! They don’t even have to work at it anymore and they are getting paid so they will tell you that everything is really great out there. I was in the real estate industry when the interest rates were really high and houses were priced really low and there was a lot to try to complete a deal. I look at what most buyers have now as mortgages and I cringe at the thought that most people pray to win millions in lotteries but can have a debt of close to that without even worrying. Stop buying then it will stop

Max

at 4:43 pm

Toronto is the best city in Canada to live, work and play. Every time I travel I appreciate T.dot a bit more. It’s not the best in many ways, and not perfect, but it is decent in most of them and for things like climate, schools, jobs, public transit, shopping, health care, multiculturalism, crime,… i would say there are many people from other countries that if they had the means, would immigrate here by choice. China, South Asia, Europe, states,… they have some major issues going on that won’t disappear soon (gun control) that make Toronto a good, cheap alternative place to live.

JCM

at 5:57 pm

The statement that “Toronto was drastically undervalued for so long” implies that there’s an objective value of real estate. There is not. There is only the price that buyers are willing to pay and sellers are willing to accept, i.e., fair market value. The expectations of market participants is all that matters.

Market participants’ expectations shifted in the last 3 years, leading to rapid price appreciation up until April 2017. People bought on the assumption that prices would keep going up. Guess what? Prices don’t always go up (as shocking as that may be to hear on this blog). Market participants’ expectations have changed accordingly.

JCM

at 9:18 pm

Sorry, incomes and affordability also matter as well as market participants’ expectations.

JP

at 10:43 pm

While I lived in Hong Kong for the past 20 years, I also lived in Toronto for a great length of time before that. TO is a great city to live indeed. The recent run up of property prices has caused TO to become the worse bubble city per the UBS Report is unfortunate. Regardless of our sentiment to this great city, we all know “Things go up must come down”. The property prices of TO are no different. A few factors will be played out in the next couple of years: 1) foremost, the interest rate which has been kept at artificially low level will increase at least by One full percentage point; 2) unemployment rate will go up instead of coming down as we are entering into the last phase of the current economic expansion cycle; and 3) both the Ontario and Toronto governments are being pressured to legislate against this bubble phenomenon. With these factors come into play in full force, we will see a dramatic shift in the buyer/seller sentiments. I have seen the shift of sentiments in both Toronto during 1990-1996 and Hong Kong during 2000-2004. And both of the results were quite damaging ie. negative equities, bank foreclosures and personal bankruptcies. It will be interesting to see how it will play out. Hopefully, there will be a soft landing and not too many households will be hurt.