Remember that infamous list of the three things you don’t talk about at a proverbial dinner party?

Politics, religion, and money.

Wow, that’s, like, soooooo 1988.

If we had more time, maybe we could add to the list, or at the very least update it for 2018. Mind you, that list could be depressing, as I really, truly think it would comprise every single topic on the planet, one of which is sure to offend somebody.

So long as we’re banning clapping in university, to avoid causing students anxiety, I think we’re going the way of bubble-wrapping ourselves, and plugging our ears every morning.

But your average TRB reader doesn’t offend so easily, right?

So we can still talk politics on this forum?

As you all know, I’m a die-hard NDP supporter.

Wait, sorry, that was incorrect.

I’m a supporter of Die Hard.

But only Part 1 and Part 2. I give Die Hard With A Vengeance a pass, but the ones thereafter were just awful.

I’m also a die-hard breaker of the rules when it comes to talking politics, and since your average TRB reader is equally likely to support Liberal, Conservative, or NDP, I’m always bound to have a few detractors.

I have mentioned on multiple occasions that I thought the 2018 Ontario Provincial election was simply a contest to see who could promise to give away the most stuff, for free, between the Liberals and the NDP. The NDP used to be the “leftist” party, but when the Liberals began to give away free stuff like they didn’t have a $15 Billion deficit hidden by creative accounting practices, the NDP said, “Oh you think that is how you give stuff away? Just watch…”

A few readers politely pointed out that the Conservatives made many promises of their own, and whether you’re spending, or making cuts, it’s going to cost the taxpayer in one way or another. Totally fair, and totally true. All three parties focused more on giving people stuff and things, rather than explaining how they would lead the population forward.

Oh, voting! What’s the point? It’s only one vote. Show me a single election that’s ever been decided by one vote. And don’t mention the movie, “Election” where Tracey Flick beats Paul Metzler by one vote, because that’s a movie. And because the guy who played Ferris Bueller rigged the election so Reese Witherspoon would lose, but we can discuss this later…

The 2019 Federal election is bound to be one for the ages, and there are reasons a plenty for this.

For starters, Justin Trudeau has had his ups and downs over the last three years, and has been, at times, the most popular Prime Minister in decades, but also the most laughed-at. He could win in a landslide, or fall on his face as his opponents look to exploit his gaffes during his tenure.

Maxime Bernier killed all the momentum that Conservatives had built up, when he decided to start his own, and soon to fail party, which will take precious votes away from the Conservatives, and simply dump them in the Ottawa River.

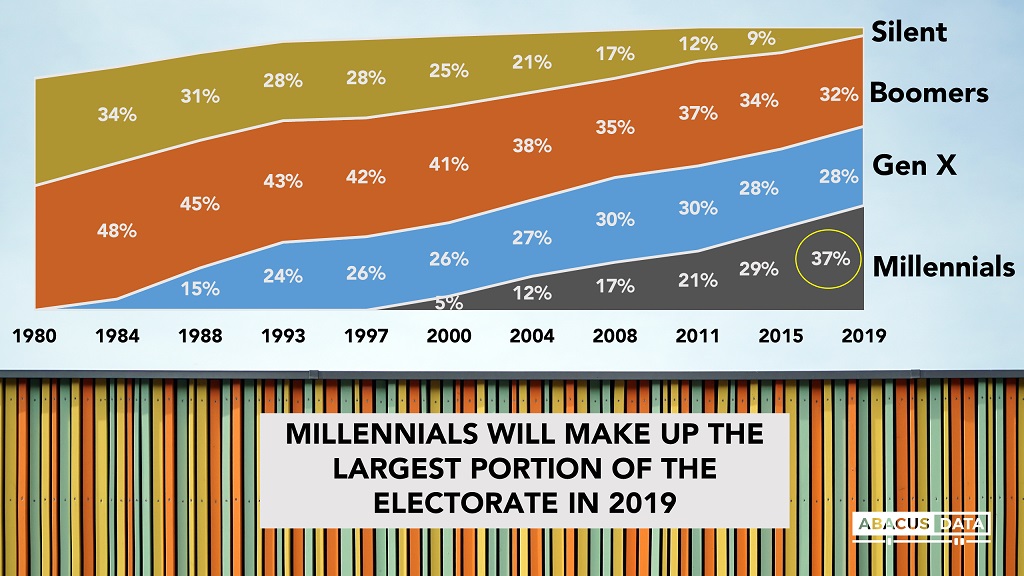

And oh yeah – for the first time EVER, millennials will represent the highest proportion of voters.

All of a sudden, the first two reasons don’t even seem to matter.

Millennials will decide this election, isn’t that something?

You senior citizens must be shaking your canes in an angry fashion right now, ready to throw your VHS collections of M*A*S*H through the pigeon-proofing on the window, and out into your extremely well-manicured lawns.

The thought of millennials riding their Segways into voting booths while live-streaming their “pick” on InstaFaceChat, stopping periodically to look at photos of their friends’ lunches on social media, is hard to stomach for many of us, whose stomachs aren’t filled with Avacado Toast.

But like it or not, millennials will decide the next election, statistically-speaking.

And what, aside from donating money to Kylie Jenner to ensure she can join the billionaire club, are millennials primarily concerned with in 2018?

Housing.

Housing, Housing, Housing. I really do expect this to be a major theme in the upcoming election, and if it’s not one that voters want to raise, I still see politicians using it as a springboard.

Crime is a boring story, and even those who read about it, don’t feel “affected” by it.

The economy sounds interesting in theory, but again, you have to give a you-know-what to really dig deep enough to see how it matters to you.

Jobs? Meh. Let’s just typecast and say that those people who don’t have one, don’t vote.

Climate change? Let’s get real. Canada is responsible for, what, like 2% of world greenhouse emissions? Psssh!

Electoral reform? What is that, anyways?

I could go on, and on, and be equally as sarcastic.

But on a truly serious note, I believe, with all my heart, that the election issues that voters really take seriously are the ones that affect them the most. Election promises that voters will benefit from, legislation that will help them, and any and all words coming out of a politician’s mouth that will have a tangible affect on one’s livelihood, will win votes in 2019.

During the early-going in this year’s Provincial election, I saw a comment on Facebook that said something to the extent of: “Free daycare? OMG! I mean, I don’t like the Liberals, hate them, in fact, but if this is really true, they’ve got my vote! ‘You do you,’ ya know?”

That was the moment, folks. One stupid comment on Facebook, from a person I don’t even know, brought me to a realization that I should have already come to sooner: people will always do what’s best for them.

As much as we should care about electoral reform, as concerned and involved as we should be regarding climate change, as passionate as we should be with immigration, or violent crime in poor neighbourhoods, we’re still going to look long and hard at election platforms that directly affect and benefit us.

The Canadian Real Estate Association recently hired Abacus Data to conduct a nation-wide survey of 2,500 people, all millennials, with respect to their feelings on all things related to housing.

The results were published on Monday, and you can read the whole article HERE.

The study is eye-opening, and I say that both as a voter, and as a real estate agent.

Take a look if you have time. It’s a fast read, and you’ll thank me.

But if I could borrow a couple of their graphics (and I’m letting myself do so because of all the money I pay to CREA which goes to waste…), I think the points really drive themselves home.

First, consider what I said above – that the millennials will be the largest set of voters in the 2019 election:

Take that, Boomers!

God. My poor mother, what must she be thinking?

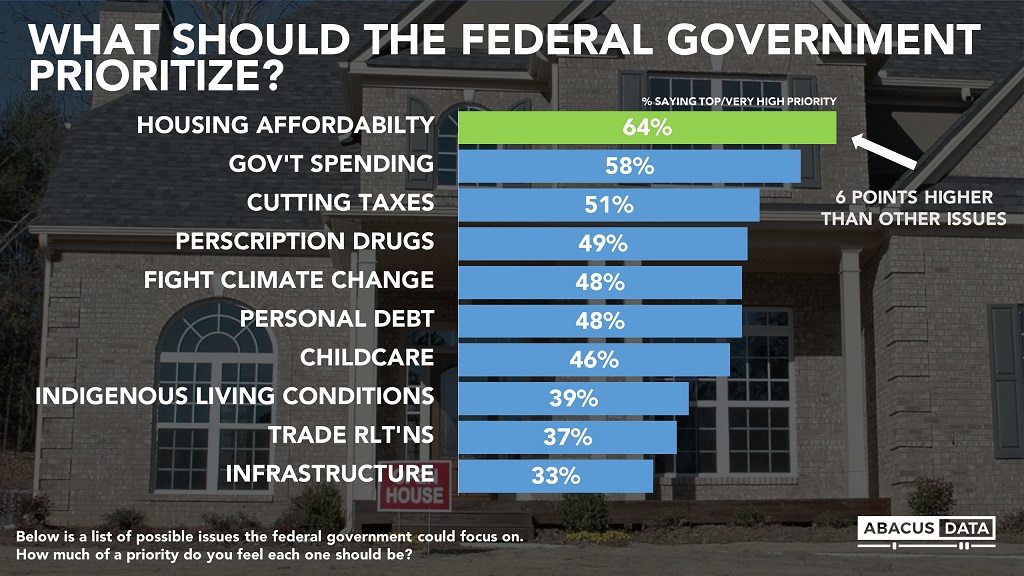

The study goes on to look at just how much housing is an issue for millennials:

Now if I could be humble for a moment, let me be honest: there are several things on that list that I can’t imagine millennials calling a “top or very high priority.” And not just millennials, to be fair, because this list is about millennials, but do 37% of people really care about trade relations? Or are they just trying to sound smart?

But if 64% of millennials believe the federal government should prioritize housing affordability, as the top, or very high priority, what does that say about our three major political parties’ focus in the coming election?

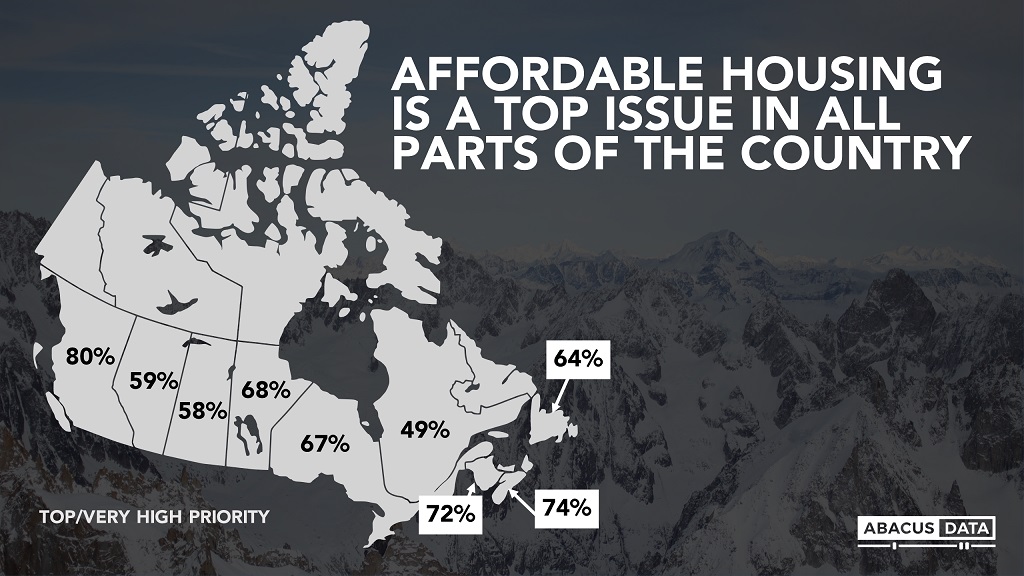

Amazingly, affordable housing was the top result in all nine provinces that were part of the survey:

Just look at B.C. wow!

A whopping 80% of millennials would put housing at the top of the list? I’d have suggested that the 67% in Ontario was a big number, but it’s absolutely dwarfed by B.C.

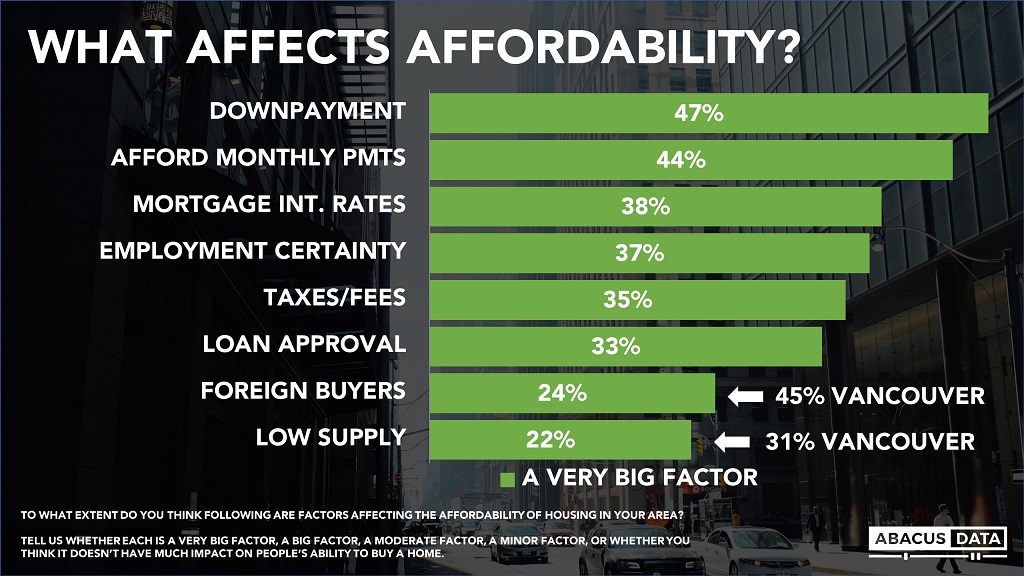

There are a slew of other graphics in the article, but the only other one worth exploring is this:

Note the fine print at the bottom – respondents were given options as to whether the factor was big, moderate, minor, or had no impact on affordability.

Interesting that downpayment was at the top of the list, since there’s a prevailing sentiment among the public that millennials are all rich kids getting money from their Baby Boomer parents to buy their first home.

Also interesting that 41% of Vancouver millennials still think “foreign buyers” are a very big factor. I’d love to see what that percentage was in Toronto.

The idea that 33% of millennials believe “loan approval” is a very big factor shows me that a third of all millennials haven’t done their homework! Pre-approvals are the easiest part of the home-buying process, and I rarely, if ever, come across a potential buyer that can’t get a mortgage.

I’m also not sure I understand “taxes/fees.” Yes, the $4,000 in property taxes you pay per year sucks, but it’s not really a factor on its own, especially if “afford monthly payments” is another factor.

I could blame Abacus Data for these silly options, or blame the respondents for not really knowing what’s what. Either way, I think the fact that “downpayments” and “affordable monthly payments” are at the top of the list are the major take-aways here.

Now as luck would have it, after I started writing this blog, yet another article with the same major theme hit the newswire:

“Poll: 94% of GTA Millennials Concerned They Won’t Be Able To Buy A Home”

This poll was conducted by Ipsos Reid, and commissioned by the Building Industry & Land Development Association, and the good ‘ole Toronto Real Estate Board.

Geez, what’s with organized real estate and polling millennials, eh?

Further 86% agreed with the statement that “it is important that young families can afford to live and work in the GTA without having to commute for more than an hour to get to their place of employment.”

And how about this great quote from the President of TREB, Garry Bhaura:

“The best public policy is proactive, not reactive. We hope these poll results demonstrate that the time for municipal decision-makers to start thinking about housing choice and supply for all GTA residents who want to own a home is now,”

Conspiracy theorists, put on your tinfoil hats! CREA and TREB are lobbying government!

As for the millennials, relax, you got this.

Or should I say we got this?

I was born in 1980, after all…

A Grant

at 8:08 am

Maybe I’m an outlier, but when I vote, I don’t “always do what’s best for” me. I want my neighbours to have access to free/subsidized childcare, quality public transportation, and affordable housing. Even though I don’t have kids, never use public transportation, and own my own home.

daniel b

at 10:14 am

On the contrary Grant, i’d say the research suggests most people vote like you. Why do high income earning downtown liberals elect leftish governments that tax them a lot? Why do poor rural voters elect right wing governments that pass tax cuts that almost exclusively benefit the downtown liberals? People vote based on an idea of what is fair and right for the country, whether it benefits them or not. David, unfortunately, suffers from the same issue as most of the conservatives i know, which is that he has very strong opinions on issues, such as voter motivation, but no inclination to actually learn anything about them by reading. In lieu of baseless prejudices, the world is awash in research and data for those interested to avail themselves of it.

Joel

at 10:35 am

I think the confusion here is that this reads as financially in their best interest, which is how many conservatives look at and justify their vote.

Socially and perhaps morally you don’t think voting conservative is in your best interest and that outweighs the financial incentive for you.

To me that is how I look at voting. What is best for me is a country that helps those in need and provides infrastructure, rather than a tax rebate for me.

Batalha

at 1:59 pm

Exactly. Because your tax rebate won’t fix the potholes on your street or build a school or hospital in your area or help provide clean water from your tap or ensure no ebola in your food or …

Well, you get my point.

Andy K

at 10:11 am

You are most definitely an outlier. A greater person than most and an outlier as a result.

Real estate millennial

at 10:35 am

The government fixing housing affordability further more any issue is laughable. Land is not infinite so there’s only so much housing you can build in one area. In the society we live in, the person who gets that home when the supply is limited is usually the highest bidder. I find it funny that the best solution is highly overlooked “transportation” when we can move people quickly and efficiently it doesn’t matter where you live. Like most adults my generation has no idea about the concept of economic constraints and how it plays a vital role in the life we live and the actions of politicians “not their verbal promises”.

Housing Bear

at 11:04 am

Well look at the quality of the people taking these polls. Interest rates the single most important factor for affordability only ranked third. Lower rates can buy you more house with the same down payment, lower rates reduce monthly mortgage payments. Lower rates make loan approval easier.

And yes modern public transportation could help out big time, but unfortunately we ranked infrastructure as the least important category in the first poll David shared

daniel b

at 11:14 am

lower interest rates improve affordability, provided you build enough housing. If you have a chronic housing shortage then lower rates only serve to bid up the prices of the stock.

Joel

at 11:19 am

With the current government regulations lower rates wont make a huge difference as the stress test applies and has a minimum. (Currently 5.34)

If the rules around that changed which I could see some governments changing affordability would improve, but prices would go up.

Housing Bear

at 3:35 pm

B20 is a soft 2% rate hike. Still holds true that RE and interest rates have a negative correlation. B-20 was set up to protect the banks, individuals can still go to private lenders where they wont face any stress test. Owners do not actually have to make payments based on their total debt level at a rate which is 2% higher. An actually 2% hike would hit ALL would-be buyers and eventually HIT all owners carrying debt. This would tank the market over night. Rates are trending higher for the short to mid term so B20 is actually a very wise measure to have implemented. I agree that b-20 will be dropped at some point, but this will be when it is clear that rates are on their way down again.

Affordability in the housing sense refers to your monthly payments vs your monthly income. People dont buy a house, the buy a mortgage payment.

Lower rates mean you can have the same monthly payments with a higher total debt level. A supply shortage along with expectations of further capital appreciation (under the assumption that supply shortage is a permanent thing) gets everyone to max out their total debt carrying capacity at a giving level of interest rates. We allowed this happen in an environment where rates were basically zero and have no where to go but up. Big mistake, and a lot of pain on its way for people who did max out when we had record level pricing.

Permanent supply shortage? – Could make this argument for SFH, we do not really have space to build more houses in Toronto proper.

Permanent supply shortage for condos? This is an absolutely insane claim. Look down streets like Danforth, Queen, Bloor, ETC. How many 100 year old 2 story brick building do you see? All of this can one day be converted to condos.

We also have record condo supply under construction right now.

daniel b

at 4:55 pm

Your particular examples of streets with the capacity to accommodate substantial growth are probably ill advised. Queen st has heritage conservation overlays on most of it now. Danforth has resisted development along most of its length because the politics of it are brutal and the existing density supports pretty high land values, which makes assembling for redev very difficult. Bloor has segment studies underway on most it which will cap heights pretty low. The new downtown plan means highrises can only be approved on sites with a very particular set of conditions, of which there are almost none left.

Remember ‘forest of cranes’ you’re used to was approved when the OMB was there. Without you can expect a much smaller supply channel. Further, note that in spite of all the construction, vacancy is effectively zero. We’ll get a couple good years of completions in 2020 and 2021, that may get a little relief, but overall i think we’re structurally into undersupply for the foreseeable future.

Also, at the risk of the word count on this response getting me into ‘chat board crank’ territory, i’ll add that most people’s impression of the supply is driven by cranes, while the dissappearance of low rise starts never registers. Much of the high rise is merely replacing low rise starts that don’t happen anymore…

Lastly, for whatever it’s worth, a hard recession or crazy spike in rates (which i think would cause a recession) would definitely clip values – i’m not a perma bull by any means. That said, unless our immigration and interprovincial migration trends change dramatically we’re going to be sub 2% vacancy for the next generation. You heard it here first!

Appraiser

at 4:58 pm

TREB data for September out today. Sales up and average prices up for the fourth month in a row, year over year. Could be a trend?

Questor

at 5:05 pm

To say/imply that a two percentage point rise in interest rates (from right now, presumably) would “tank the market overnight” is simply ridiculous, since a hike of this magnitude will occur over the space of two years, at least. Certainly higher rates will cool the RE market, but “overnight”? Skip the hyperbole, please.

Housing Bear

at 10:01 am

I did not imply for a second that it would be a 2% hike overnight. I was explaining the difference between b-20′ impact (a soft overnight hike of 2%) vs the impact actual interest rates increasing. Its funny that’s the only thing you could come up with to try and challenge me on. Have a nice day.

@Appraiser – I don’t know how you can find anything positive from the September numbers at all. Sales down from August! One of the weakest Septembers overall in the last decade. Expectations for further rate hikes are up now that trade with the US is resolved. I’ll call a mediocre fall, panic by spring. Our July bet is looking better and better to me.

Housing Bear

at 10:18 am

@daniel b

My point was to challenge the assertion that “there is no where left to build”. True for SFH, not for condos. I live in leslieville, you walk east or west on Queen and every other block has a recently completed or under development building. Not high rise mind you, but still provides much more accommodation than the traditional old brick buildings. The same is true for Queen street in the beaches areas. Danforth is seeing a lot of development starting east of Woodbine.

In regards to politics and NIMBYs – that can all change at any time. Just like b-20 will be dropped once rates stop going up.

If we hit a recession, expect immigration to level off.

Joel

at 1:47 pm

Individuals can not go to private lenders to avoid this at similar rates. Credit Unions are offering this service, but with rates about 1.5% higher, which is not doing much in terms of affordability.

Of course lower rates can lower your payment, but with the stress test set at a minimum of 5.34% rates lower than 3.34% won’t make a difference.

Parkhurst.bessborough

at 11:02 am

I am clapping loudly for this blog, David. No jazz hands here.

Numberco Owner of Real Estate

at 12:24 pm

I would offer the proposition that younger voters vote based on what is best for them. Older folks, who are arguably less dependent on government assistance/support, have more flexibility and thus are more open to vote based on what is best for the greater good.

Carl

at 12:57 pm

If housing is an election issue, it is an issue for municipal and provincial elections. There is very little that the federal government can or should do about it, with one exception: dealing with real estate being used for tax evasion and money laundering.

Jennifer

at 1:31 pm

Agree with this. Property law is a provincial matter. And it didnt factor much into that election. The millennials should have shown up there and made their concern known at that time. Oh but wait, we had Ford who won on zero platform. THAT’s how much people disliked the liberals.

What could the feds do? Change the home buyers plan? Give some tax breaks? Play around with CMHC? Would they have the power to ban foreign ownership, like some other countries did, for example? Any constitutional law experts out there?

Kate

at 4:04 pm

The federal government could pull back a little on the immigration levels. That would be a big help. They could also put the kai-bosh on foreign students purchasing property. They can rent like the rest of us.

QMJHL

at 1:52 pm

“legislation that will help them”…?

What planet are you on? Apparently, one where people (well, lifeforms, anyway) pay attention to proposed legislation. My, how quaint a notion.

Appraiser

at 6:09 pm

Moody’s Analytics:

“Overall, the report projects a fairly stable Canadian housing market with no major short-term correction over the next five years. In markets where there are house price increases, those are expected to continue to moderate, and could be offset by higher income.”

https://business.financialpost.com/personal-finance/mortgages-real-estate/housing-market-not-headed-for-a-major-correction-moodys-analytics-says

Carl

at 7:29 am

Their June report stated “Toronto and Vancouver will go through short but

significant house price corrections that will bring their prices more in line with long-term

trend values”. What changed in four months?

Housing Bear

at 10:03 am

Rates have gone up along with expectations for further hikes?

But I mean it is Moody’s – weren’t they the ones who called the US housing bubble ten years ago…………….. Oh wait, no they were the ones who rated packages of subprime loans as AAA

Housing Bear

at 10:24 am

Past 2020, “it’s really going to hit the fan,” Caranci said. “At that point you have high level of indebtedness combined with income stress happening simultaneously. So we are definitely not out of the woods.”

The next recession for Canada will be different than the previous because it will be “a household led recession,” Caranci said.

– Beata Caranci, chief economist at Toronto-Dominion Bank

Whoa, so now even our big banks are calling it for what it is?

Fun fact for you; Household led recessions are the worst because over 2/3rds of our economy is based on consumption.

Questor

at 10:47 am

I quote: “An actually (sic) 2% hike would hit ALL would-be buyers and eventually HIT all owners carrying debt. This would tank the market over night.“

“Eventually” hit all indebted households, absolutely. My only point of contention was the leap from “eventually” to “overnight.” I strongly agree that the market will slump/tank/cool/crash/dip as rates rise, but over a reasonably long period of time. Although I suppose one person’s “reasonably long” can be another’s “reasonably short.”

Housing Bear

at 11:15 am

No you implied that I was stating that rates could/would jump 2% overnight.

Quote – “Certainly higher rates will cool the RE market, but “overnight”? Skip the hyperbole, please.”

Because I’m in a good mood today I will still address your new angle.

A 2% hike in one shot would remove the vast majority of new buyers from the market. If you can’t sell your 500k condo and take out your equity how do you move up to the 1.2 million dollar property? This effects the whole move up ladder- Huge reduction in demand

HELOCs, CCs, a lot of variable rate mortgages would adjust higher on the spot and would force many to have to sell – Huge increase in supply, where demand has already been gutted.

The above all happens overnight.

Discounting the fear of catching a falling knife, prices would have to adjust to a point where normal buyers can afford to buy at the new interest rate level. Plus we would certainly be in a recession at this point (or headed for one very quickly) because even those that could afford their debts will be squeezed from spending money elsewhere in the economy. Our economy is 2/3rds consumption driven.

Eventual problems;

The problem would be prolonged as fixed rate mortgages renew over the next few years, many of which would be doing so with negative equity. – More forced sales and supply?

If banks are watching the value of THEIR assets (Your home) fall in value and defaults are increasing, guess what they do? They stop making new loans to shore up their reserves – Further hit to demand.

These eventual problems add to job loss and overall strain on the economy.

Its a good thing that we WON”T get a 2% hike in one shot, the rises will be gradual. 25bps at a time, 50bps max. For those with multiple years left on their mortgages gradual vs sudden may not even make that much of a difference (other than from a demand perspective) but I doubt rates will even get to 2% higher than they are today. The economy and housing market will break before then.

Questor

at 1:19 pm

Sorry, my lack of clarity. When I wrote “Certainly higher rates will cool the RE market, but ‘overnight’?” the word “overnight” was meant to refer to the cooling of the market, which is how I interpreted your original statement that “This (interest rates increasing by two points over time) will tank the market overnight.”

In essence, both rising rates and a cooling RE market figure to play out over a couple of years, unless, as you surmise (and as is quite likely), the economy and housing market(s) have broken/collapsed/weakened before Governor Poloz has a chance to move rates two points higher.

Izzy Bedibida

at 3:01 pm

Exactly. The last thing we need to for most of the GTA residents to become ENDIE’s like many London residents. This will put a strain on consumer spending.

An older, but interesting artical:

https://tvo.org/article/current-affairs/are-londons-endies-a-warning-for-canadas-housing-market